Disclaimer: The information contained in this article does not constitute investment advice or a solicitation to buy or sell financial products.

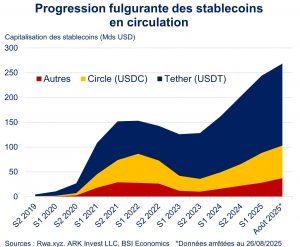

This note aims to decipher a significant graph related to current economic events. On July 18, 2025, the Genius Act was passed in the United States, establishing a regulatory framework for the integration of stablecoins into the financial system. This law would reinforce the rapid growth of stablecoins (see Killer Chart below), with potential opportunities for the United States but also some gray areas.

Download the PDF:killer-chart-stablecoins-real-opportunity-or-source-of-instability

Why is this interesting?

A stablecoin is a digital asset that is indexed to the value of a reference financial asset, mainly currencies (68% of stablecoins in circulation are pegged to the US dollar and their capitalization represents 99% of the total stablecoins issued, according to ARK IM[1]). Unlike bitcoin and other highly volatile cryptocurrencies, the value of a stablecoin (SC) remains stable over time relative to the currency to which it is pegged.

SC can be purchased on cryptocurrency exchange platforms and are seen as a low-cost alternative means of payment[2] or as an asset serving as a store of value[3]. Since 2020, SCs, whose market capitalization has increased nearly tenfold in five years to reach USD 268.4 billion at the end of August 2025, have been experiencing a surge in popularity.

Stablecoins are issued by private investment companies, which ensure their stability through reserves that they hold elsewhere and manage as collateral. For example, for each dollar-indexed stablecoin issued, the issuer must hold a dollar-denominated asset with a value equivalent to the amount of the stablecoin in question. The stability of SCs therefore depends heavily on the sound management of these reserves by their issuers. However, the details of this management remained unclear at this stage, and one of the objectives of the Genius law is to ensure better control and greater transparency.

This change in the regulatory framework would, in principle, strengthen the liquidity of SCs. By reassuring potential buyers of the credibility and solidity of issuers, it would increase demand for a market whose capitalization could reach $2 trillion by 2028, according to U.S. Treasury Secretary S. Bessent. This phenomenon could prove favorable to the ambitions of the US government.

What to make of it?

The significant fiscal stimulus sought by the new Trump administration in the United States will lead to colossal financing needs. However, public debt financing conditions have tended to deteriorate in recent quarters (see this Killer Chart from BSI Economics for more information). An increase in USD-indexed stablecoins would present a real opportunity by fueling increased demand for US Treasury securities, which would be used as collateral. Indeed, the need for stablecoin issuers to have USD-denominated cash reserves (see ndbp 4) is pushing them to acquire more and more US securities, mainly Treasury bills. Tether and Circle, the main issuers, which account for 86% of the stablecoin market, held USD 182.1 billion[6] in US Treasury bonds in June 2025, nearly double the level of two years ago (USD 96.3 billion), making them among the largest purchasers of these securities in the world[7].

Their weight is expected to increase in the coming quarters and their demand for US sovereign debt securities would, at least partially, replace the lower demand from other traditional investors, which would also have the likely beneficial effect of generating downward pressure on T-Bill yields (see BIS report). However, there are several risks to note. Beyond the challenges of tracing illicit funds and combating money laundering and terrorist financing that the Genius Act must address, other aspects could be sources of financial instability.

The sensitivity of SC issuers to changes in the market prices of their collateral, and in particular to an increase in interest rates that would reduce the value of the securities, is particularly questionable, as this sensitivity is likely to differ significantly from that of traditional institutional investors. Indeed, the composition of SC issuers’ balance sheets is currently less diversified than that of Money Market Funds, for example.

In the event of pressure on short-term interest rates, SC issuers need to be more agile in restructuring their assets and reserves (whose market value falls in response to rising interest rates). They would probably be unable to do so if, at the same time, SC holders wanted to withdraw or exchange their SCs. This scenario would require MMF issuers to sell their most liquid reserves (T-bills) in order to free up the funds needed to ensure that MMF holders can cash out… at the risk of triggering a crisis of confidence, or even a vicious circle that could lead to the depletion of reserves and/or a bank run. This scenario would lead to a sharp contraction in issuers’ assets and significant disposals of their T-bills, which could generate, at the very least, high volatility in the bond markets (see the bankruptcy of Silicon Valley Bank in 2023).

The risk is all the greater given the growing weight of SC issuers in US sovereign bond holdings (see figuresfrom ARK IM and the BIS) and the systemic risk associated with the current high concentration of issuers in the market (Tether, Circle, Stably, Binance, to name but a few). This risk appears to be significant, given the continuing uncertainty surrounding the trajectory of inflation in the United States and its counterpart (a potential rise in key interest rates by the Federal Reserve).

The issue of loss of monetary sovereignty linked to the issuance of SCs is also often cited as a risk factor. However, this risk seems to pose more of a threat to other countries in the event of strong demand for USD-indexed SCs (this point will be the subject of a future Killer Chart).

The rapid emergence of dollar-indexed SCs would represent a real opportunity for the United States, given the current context of sharply rising public debt. This can only be successful if the Genius Act effectively establishes a solid regulatory framework. This framework must go hand in hand with an increase in the number of issuers and a more robust reserve management model, otherwise there is a risk of encouraging the creation of new systemic players that pose a real threat to financial stability.

V.L, article written on 08/26/2025

[1] Two stablecoins indexed to the US dollar, Tether (USDT, blue area on the Killer Chart) and Circle (USDC, yellow area on the Killer Chart), account for 86% of the market share of stablecoins in circulation.

[2] This cost is particularly advantageous for international fund transfers.

[3] They can also serve as solid collateral in decentralized financial transactions (or « DeFI protocol »; for more information, see this article by Victor Warhem on BSI Economics). However, unlike fiat currency, they do not generate a direct return, except through investment.

[4] In principle, the issuer holds adequate reserves to ensure the stability of the stablecoin, in particular by responding to potential demand for the sale or conversion of the SC by its holders. In principle, an SC holder should be able to sell their SC at any time without incurring any exchange rate risk. To do this, the SC issuer must therefore have sufficient reserves that it can quickly sell (usually US Treasury bonds) to free up the funds needed to meet this type of demand. Otherwise, the stability of the SC is not assured and exposes the entire ecosystem to significant liquidity risk.

[5] See these forecasts for the Big Beautiful Bill or these forecasts for the House Reconciliation Bill.

[6] These figures take into account direct holdings of US Treasury bills and indirect holdings via shares in money market funds or reverse repo transactions collateralized by Treasury bonds.

[7] According to the Bank for International Settlements, SC issuers purchased USD 40 billion worth of T-Bills in 2024, more than Fidelity Government Money Market Funds (USD 27 billion) or Japan (USD 23 billion).

[8] These are investment funds specializing in the purchase of short-term financial instruments issued by the government or government entities. Their model is also designed to take advantage of rising short-term interest rates, which is not the case for SC issuers.

[9] This basic financial mechanism is linked to the fact that, for bonds, yields move in the opposite direction to their prices.

[10] Although the 1-year inflation expectations in the University of Michigan survey fell recently during the summer of 2025 (4.9% in August compared with a peak of 6.6% in May), they remain above the current level and the Federal Reserve’s inflation target.