Usefulness of the article: Private sector debt, the threat of a sharp rise in US interest rates, vulnerability to protectionist escalation, political risks… The risks associated with emerging economies are currently worrying the markets, undermining their GDP growth. However, in the early 2000s, emerging economies saw their GDP grow faster than that of developed countries, with a differential of 4% to 5%. These countries alternate between periods of prosperity, during which they inspire optimism, and periods, such as the current one, during which they cause concern.

Summary:

- Some countries find themselves stuck in a phase of development: their GDP per capita is stagnating and is therefore not converging with that of developed countries.

- This phenomenon, known as the « middle-income trap, » affects two regions in particular: Latin America and the MENA region (Middle East and North Africa). Conversely, some countries in East and Southeast Asia, such as South Korea, Japan, and Singapore, have experienced significant growth over a long period of time, becoming developed countries.

- To overcome this trap, the countries concerned must adopt a new economic model that emphasizes domestic consumption and, above all, productivity growth: policies that encourage education and innovation are therefore becoming essential for these economies.

Since the 2008 crisis, the global economy has been growing at a slower pace than in the years preceding the shock (around 2%). This could suggest that a period of long-term slowdown is possible. Empirically, per capita GDP data show that not all countries are converging in terms of growth. There are three types of trends: countries that are converging towards the per capita income level of the United States (around $60,000 in 2017)[1], which serves as a benchmark; those that are growing at a level equivalent to that of the United States; and finally, there is a group of countries for which there is a divergence: the wealth gap tends to increase with that of the benchmark.

Research has led to the idea that, in order to move from one income bracket to another, structural reforms are necessary to maintain high per capita income growth. Empirically, however, many countries seem to fail in this convergence process. This result implies the existence of what is known as the « middle-income trap. » The concept of the middle-income trap refers to a threshold level of per capita income above which countries that have reached it are stuck in a trap that prevents them from growing further. Are emerging countries therefore doomed to remain countries of the future for a long time to come, as Georges Clemenceau said in his day about Brazil? Not necessarily: a coherent long-term policy can remedy this.

The concept of the middle-income trap

The term « middle-income trap » was first used by Homi Kharas and Harinder Kohli in 2007. There is no consensus on the definition of this phenomenon: two views can be discerned. The first defines the middle-income trap in absolute terms: according to this definition, a country is in this trap if it remains at the GDP per capita levels of middle-income countries for a sufficiently long period of time[2]. Felipe et al. (2012) define two subcategories within middle-income countries. Countries that remain in these subcategories for more than 42 years in total are considered to be trapped. The middle-income trap is seen as a duration; a country that takes « too » long to move into the high-income category is thus trapped.

Another view, used in particular by Justin Yifu Lin and David Rosenblatt (2012), defines the middle-income trap in relative terms. A country is said to be trapped if its per capita GDP growth stagnates for a long period of time compared to that of a reference country (most often the United States).

The mechanisms at play

Initially, most low-income countries that have successfully transitioned to middle-income status have done so by changing their economic model. They have been able to move from a model based primarily on agriculture (a sector that generates low value added) to a more diversified model based on industrialization, which is more productive. A significant portion of the gains are thus based on exports of goods. These countries enjoy a relative advantage over other economies in terms of labor costs, which are much lower than in developed countries.

However, this model is not viable in the long term (i.e., at least 15 years and up to several decades, depending on the study). As these countries become wealthier, upward wage pressures make the price competitiveness advantage less favorable, as labor costs rise. Without a change in the economic model, or without moving upmarket in terms of exported products, exports are likely to decline. Trade no longer enables countries to maintain high growth rates. After experiencing a period of strong growth that enabled them to move from low-income to middle-income status, countries must now adopt a new model that places greater emphasis on improving their price and non-price competitiveness and strengthening domestic demand. This will enable them to return to growth through the development of higher value-added sectors and the emergence of a middle class with an increasingly high marginal propensity to consume. This significant change in the growth model requires consistency in economic policies over time.

Latin America and MENA versus East and Southeast Asia

Over the last century, the global economy has been largely dominated by a small number of industrialized countries (the United States, the United Kingdom, France, Germany, Italy, and Japan). The share of global GDP accounted for by the seven most developed economies fluctuated between 45% and 50% during the20th century (Figure 1). However, from the middle of the century onwards, this share gradually declined.

Figure 1: Share of G7 GDP in global GDP, in percent

Source: Lin and Rosenblatt, 2012

But it was mainly during the first decade of the21st century that the share of emerging economies in global GDP grew rapidly, narrowing the gap with developed countries. This rapid decline in the dominance of the most industrialized countries can be explained mainly by the strong growth of the BRIC countries (Brazil, Russia, India, and China), which alone accounted for around 40% of the world’s population in 2011. All these factors point to a global catch-up effect towards the income levels of the most developed countries.

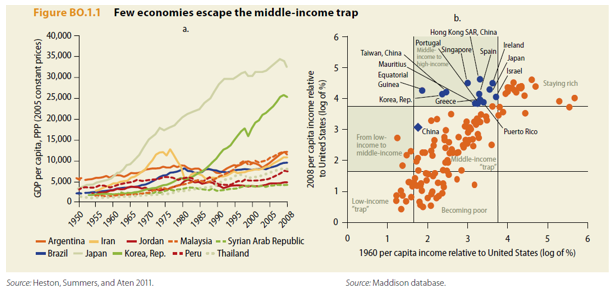

However, between 1960 and 2008, only 13 countries moved from middle to high income (Figure 2) out of the 101 countries in this income bracket.

Figure 2: Countries that have escaped the middle-income trap

Source: China 2030 Building a Modern, Harmonious, and Creative Society, The World Bank.

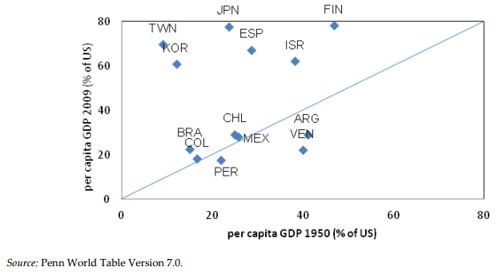

Regional dynamics emerge from this general observation. Among the few countries that have succeeded in becoming high-income countries and remaining so, six are located in East and Southeast Asia[4], suggesting that a regional factor may have benefited all of these economies. Conversely, Latin America and the M ENA region are two regions where GDP per capita has stagnated (Figure 3).

Figure 3: GDP per capita in 1950 and 2009 (as a percentage of US GDP per capita)

Source : A . Jankowska, A. Nagengast, and J. R. Perea, 2012

How can we escape the middle-income trap?

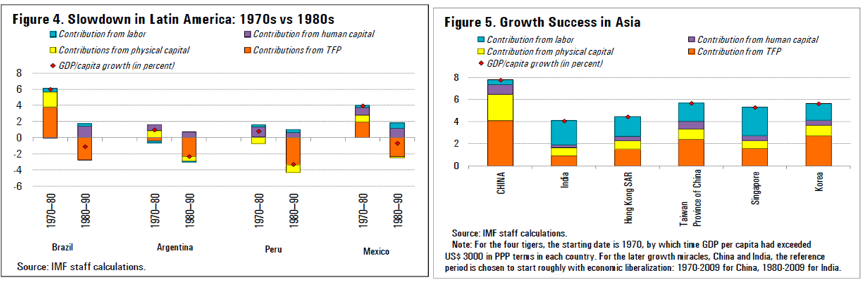

How can we explain such different growth trajectories for countries starting from roughly equivalent income levels? Economic literature on the middle-income trap agrees that productivity[7] plays a major role in whether or not this trap occurs. In addition to the necessary refocusing on domestic consumption mentioned above, it is indeed the productivity component that explains most of the success of the « escapers » (Figure 4). Conversely, it has contributed negatively to growth in Latin American countries. Barry Eichengreen et al. (2013) show that 85% of the reduction in GDP per capita growth is linked to the decline in productivity. This is because, once the middle-income threshold has been reached, it is not a lack of investment stock that countries suffer from (many of them, notably Brazil and Malaysia, have already achieved a high degree of industrialization), but rather a lack of productivity.

Figure 4: Contribution to growth, Latin American and Asian regions

Source: Shekhar Aiyar, Romain Duval, Damien Puy, Yiqun Wu, and Longmei Zhang (2013)

What are the levers to remedy this? In addition to technical progress, there are three determinants of productivity growth according to Pierre-Richard Agénor and Otaviano Canuto (2012): human capital, access to public infrastructure (transportation, telecommunications), and positive externalities from the knowledge network already present within the economy.

Anchoring these determinants in an economy requires structural reforms. The country must have an effective education system that is accessible to as many people as possible, including in higher education. To encourage innovation, massive investment is needed to develop new sectors with higher added value: policies that encourage entrepreneurship, guarantees of property rights, etc. Similarly, the establishment of efficient infrastructure on a national scale requires heavy investment. But this infrastructure is essential because it reduces transportation-related transaction costs and facilitates the flow of information and, therefore, knowledge. Labor market reforms are also crucial: rigidities in this market can discourage hiring in the most innovative sectors. Finally, improving governance is a major factor in this productivity issue. In countries where corruption is endemic, resources are allocated in a particularly inefficient manner. This creates wage distortions and discourages individuals from giving their best, since their wages are completely disconnected from their level of productivity.

Conclusion

The middle-income trap is not simply a slowdown in growth: it is a long-term phenomenon that requires a transition to a new economic model. It highlights the need for good governance to ensure the consistency of economic policies over time. This is a major challenge for countries whose institutions are often riddled with corruption, and it adds to the other challenges they face: increasing automation of work, the resurgence of protectionist policies, the fight against climate change, etc. The middle-income trap will continue to be a hot topic for some time to come.

Bibliography

Felipe, Jesus and Abdon, Arnelyn and Kumar, Utsav, Tracking The Middle-Income Trap: What Is It, Who Is In It, And Why? (April 2012). Levy Economics Institute Working Paper.

Justin Yifu Lin & David Rosenblatt, 2012. « Shifting patterns of economic growth and rethinking development, » Journal of Economic Policy Reform, Taylor & Francis Journals, vol. 15(3), pages 171-194, September.

Kharas, H., & Kohli, H. (2011). What Is the Middle Income Trap, Why do Countries Fall into It, and How Can It Be Avoided? Global Journal of Emerging Market Economies, 3(3), 281–289.

Eichengreen, Barry and Park, Donghyun and Shin, Kwanho, Growth Slowdowns Redux: New Evidence on the Middle-Income Trap (January 2013). NBER Working Paper No. w18673.

Raj Nallari, Shahid Yusuf, Breda Griffith, and Rwitwika Bhattacharya, Frontiers in Development Policy (2011). The World Bank.

Agenor, Pierre-Richard and Canuto, Otaviano, Middle-Income Growth Traps (September 1, 2012). World Bank Policy Research Working Paper No. 6210.

[1] Source: World Bank

[2] The World Bank classifies the world’s economies according to their per capita income level. It distinguishes between two subcategories of middle-income countries: a lower bracket for countries with per capita income between USD 996 and USD 3,895; and an upper bracket for countries with per capita income between USD 3,896 and USD 12,055.

[3]These are the following countries: Equatorial Guinea, Greece, Hong Kong, Taiwan, Ireland, Israel, Japan, Mauritius, Portugal, Puerto Rico, South Korea, Singapore, Spain, and China (China’s inclusion in this list is still debated, with many observers considering it to still be in transition).

[4] These countries are: South Korea, Japan, China, Singapore, Taiwan, and Hong Kong.

[5] Middle East and North Africa.

[6] Productivity is the ratio between output and the resources (labor and capital) used to produce it. An increase in productivity means that more can be produced with the same factors of production, or that the same amount can be produced using fewer of these factors.