Usefulness of the article: In order to assess the exposure of French and European industry to protectionist risk, this article draws on the latest edition of the OECD’s TiVA database, which records international trade in terms of value added.

Summary:

- France benefits primarily from the openness and stability of the European market.

- European countries as a whole benefit from the strong integration of the single market to counter the risk of protectionism.

- China, on the other hand, occupies a unique position in that it is rapidly refocusing on its domestic market while increasing its capacity to meet foreign demand. It is asserting itself as a leading industrial power.

The various announcements of tariff increases by the United States have brought the risk of protectionism back to the forefront. The latest report from the World Trade Organization (WTO) announces that global trade in goods is expected to grow by 1.2% in 2019 and 2.7% in 2020, whereas the April forecasts predicted growth of 2.6% and 3% respectively. Similarly, the International Monetary Fund has also warned that trade tensions are weighing on global growth.

These tensions affect countries differently. China, the United States, and Europe are not equally exposed to the risk of protectionism. It is therefore interesting to understand how countries are impacted through their integration into global value chains.

The apparent loosening of global value chains

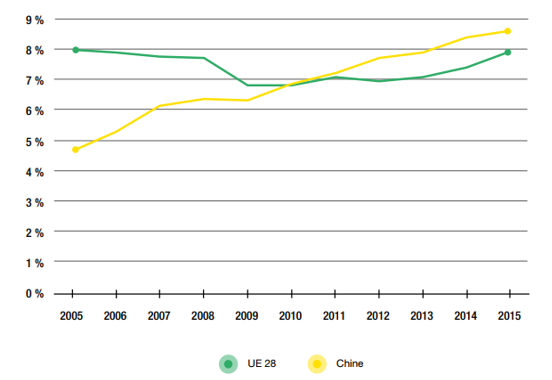

A country’s integration into global value chains can be assessed by measuring the share of foreign value added in its gross exports. In 2015, for example, value added imported from abroad accounted for 9% of US exports, 17% of Chinese exports, and 12% of the European Union’s extra-EU exports (after adjusting intra-EU flows to domestic trade). Of course, this indicator is partly linked to the size of the country in question: the larger the country, the more resources it has at its disposal and the less it depends on external sources. France and Germany, for example, have 21% foreign inputs in their exports and therefore appear to be more integrated into value chains than the two global superpowers.

Share of foreign value added in gross exports (2005-2015, in %)

Sources: Tiva, OECD

One striking phenomenon is the significant decline in the foreign content of exports since 2011 in the countries studied. At first glance, this could support the theory of a « slowdown » in globalization, or even raise questions about the initial effects of protectionist measures. In reality, in Europe as in the United States, this apparent disintegration of global value chains can be explained almost entirely by the decline in energy commodity prices. The situation is very different in China, where this phenomenon is coupled with a longer-standing trend[2]toward regionalization, as the country’s strategy is to prioritize its domestic market and reduce its dependence on foreign imports. Therefore , we cannot speak of a phenomenon of « deglobalization » on a global scale, but rather of a strong development of Chinese regionalism.

China is providing ever more added value to foreign markets while becoming more self-sufficient

The Chinese added value contained in French final manufacturing demand increased steadily between 2005 and 2015, rising from 2.5% to 6.9%. This phenomenon can be observed in all European countries, enabling China to overtake the United States at the turn of the 2010s as the leading supplier to European industries.

This increase is not specific to any particular sector but is common to all European import sectors and all Chinese export sectors. Conversely, European and French value added in Chinese final manufacturing demand has steadily declined over the same period. Similarly, China now provides more value added than the European Union to US manufacturing demand.

Share of European and Chinese value added in US final manufacturing demand (2005-2015, in %)

Sources: Tiva, OECD

Far from being limited to mass consumer products, China’s commercial dominance also extends to raw materials, capital goods, and intermediate products used in industrial value chains. Furthermore, the once popular idea that China’s own value added only came into play at the low-coststages ofassembly and manufacturing is no longer true. On the contrary, China is managing to increase its presence in foreign markets and become less and less dependent on the rest of the world to meet its own demand.

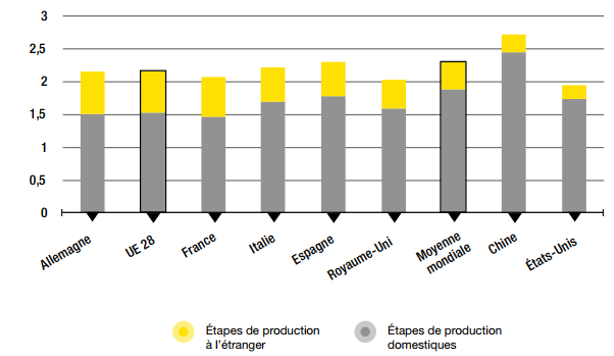

French and European industrial products go through more foreign production stages than those of Chinese and American producers

Since 2005, European industries (excluding the United Kingdom) have seen their international exposure increase, as measured by the average number of production stages remaining abroad before reaching the final consumer (from 0.52 in 2005 to 0.61 in 2015, based on an average of foreign stages starting with French producers). In contrast, this indicator has fallen sharply in China (from 0.40 in 2005 to 0.31 in 2015 foreign stages on average).

Distance to final demand in the manufacturing industry (2016)

Sources: OECD. Calculations and processing: La Fabrique de l’industrie

The metal products sector is an important explanatory variable for this phenomenon: these commodities are more likely than others to pass through foreign production stages before reaching their markets, but this number has been declining to varying degrees in all countries since 2008-2010. It is impossible to say whether tariff measures on steel and aluminum have played a significant role in this, particularly when compared with the effects of the crisis that hit the steel sector in 2008 and the huge overcapacity maintained by China in this sector. In any case, in the United States, this particular feature of the metallurgy sector is so pronounced that it is enough to bring down the overall outsourcing indicator for the entire manufacturing industry, whereas it fails to reverse the average trend in France and Germany. In China, the situation is different again: as all sectors have been refocusing on their domestic market since 2008, the general shift is all the more striking.

France’s strong integration into European value chains protects it from the risk of protectionism

European economies are highly integrated with each other within a stable, free-market zone. French and European industries are therefore benefiting from this integration, which protects them to a certain extent from protectionist tensions.

Compared to Europe, China has a special status. It is integrated into global value chains as a supplier to external markets, while rapidly increasing its capacity for self-sufficiency. In other words, China is asserting itself as a leading industrial power that the United States and the European Union must contend with.

Reference: Alsif AS., Charlet V., Lesniak C., 2019 « Is France exposed to the risk of protectionism? », La Fabrique de l’industrie – Presses des Mines, October.