Poor Countries and Tax Pressure (Part 1)

The determinants of tax burden in low-income countries

Summary:

· Domestic resources are now a major factor in the economic development of low-income countries (LICs) and will play an increasingly important role in the coming years, particularly in financing the ambitious Sustainable Development Goals (SDGs) recently defined by the international community.

· These resources appear all the more important as donor countries’ development aid budgets are being tightened in a context of « public finance crisis » and increased funding for the defense sector (particularly in countries recently affected by terrorist attacks).

· As a result, numerous initiatives aimed at improving the tax burden in LICs have recently been launched. Drawing on a wealth of literature, they aim to create an environment conducive to tax mobilization.

· The degree of trade openness, the level of development, the sectoral composition of the economy, and the quality of the institutional framework are the main factors explaining inter-country differences in taxation.

« The importance of public revenue tounderdeveloped countries can hardly be exaggerated if they are to achieve their hopes of accelerated economic progress » (Kaldor, 1962). For more than 50 years since this quote by Nicolas Kaldor, international donors and developing countries have repeatedly emphasized that taxation and the ability to collect domestic resources are one of the fundamental pillars of economic and social development. However, in debates on development financing, this important issue has often been overshadowed by others relating to aid effectiveness, the accumulation of external debt, and remittances from migrants in advanced economies.

Although the importance of domestic revenues was widely recognized in 2002 at the Monterrey Conference on Financing for Development, much of the action taken up to that point had focused on aid effectiveness in recipient countries and on measures to reduce the debt burden of heavily indebted poor countries. Nevertheless, over the years, the issue of domestic resource mobilization in developing countries has gained prominence, to the point of playing a leading role in the Addis Ababa Action Agenda (AAAA) defined following the conference on financing for development held in the Ethiopian capital last July.

However, before going into detail on proposals to improve the tax burden in low-income countries, particularly in sub-Saharan Africa (SSA), it is necessary to first identify the economic, social, and political determinants.

Level of development and sectoral composition

Although issues relating to domestic resource mobilization are currently receiving greater media coverage and renewed interest from policymakers, numerous studies published since the 1970s have sought to identify the determinants of these resources in LICs. This literature, which grew during the 1990s, has made it possible to define the main characteristics that explain the differences between countries in terms of taxation.

One of the first determinants of tax pressure put forward by studies by Lotz and Morss [1967], Bahl [1971], Chelliah et al. [1975], Tait et al. [1979], and Leuthold [1991] was the level of development, approximated in these studies by the value of GDP per capita. Most of these studies showed that the level of taxation was positively correlated with per capita income (see Figure 1 below), thus confirming Wagner’s law that demand for public services is elastic (reacts proportionally and significantly) to income, linking the need to finance these public services (and therefore additional domestic resources) to individual income levels.

Figure 1: Tax revenues and level of development

Note: All observations in the graphs in this article are averages calculated for each country over the period 1990-2012. The study sample includes countries defined as low-income countries (LICs) or lower-middle-income countries (LMICs) by the World Bank.

Sources: BSI Economics. IMF data, WDI. Author’s calculations.

In parallel with the level of development, other studies have shown that the degree of trade openness can also explain tax disparities within developing countries (Burgess and Stern [1993], Agbeyegbe et al. [2006], Khattry and Rao [2002], Baunsgaard and Keen [2010]). Historically, customs revenues have always represented a significant source of income for these countries due to the ease of identifying transactions at borders and levying taxes on them. However, although significant customs barriers generate revenue, they also represent an obstacle to trade that can potentially lead to a reduction in the total volume of transactions, ultimately reducing overall customs revenues. In fact, the Washington Consensus adopted in the late 1980s, which advocated lowering these tariff barriers, contributed to reducing the tax collected per unit traded. However, this trade liberalization also made it possible to intensify trade for developing countries (and therefore the number of taxable transactions), in some situations offsetting the loss of customs revenue per unit traded due to the lowering of customs duties. But in other cases, some studies have also shown that the decline in revenue from trade activities has forced countries dependent on this income to seek other sources of taxation, thereby increasing the level of taxes levied on income, wealth, corporate profits, and value added.

While the level of development and the degree of trade openness are two of the most important determinants of the tax burden in developing countries, other indicators also contribute to defining the tax frontier of these countries. Several empirical studies have shown that the sectoral composition of the economy can also explain changes in tax revenues. Gupta (2007) shows that countries that are still highly dependent on agriculture find it difficult to raise taxes. This can be explained by the significant VAT exemption on agricultural goods (Chambas 2005) and by the difficulty of identifying and subjecting agricultural taxpayers to taxation, particularly given the relatively informal nature of agriculture in low-income countries. On the other hand, a large industrial sector within the economy allows for higher tax revenues, as these activities are often large-scale, carried out by a limited number of companies that are therefore easily identifiable, making it possible to collect taxes without much difficulty.

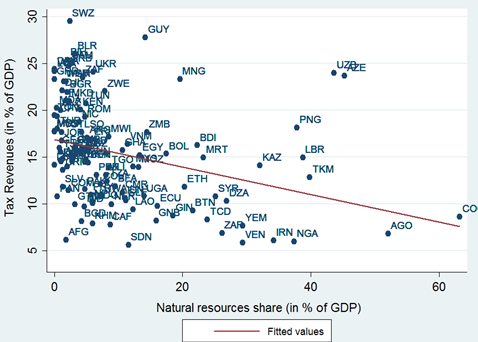

Furthermore, in developing countries, particularly those in sub-Saharan Africa, the industrial sector includes a few large companies operating in the natural resources sector (where the country in question has such resources). In this case, the financial windfall is all the greater as these natural resources are generally exported. Furthermore, the resulting profits are obvious, and when these resources are not exploited by a private company, they are exploited by a state-owned company whose profits go directly to the government’s budget. However, excessive dependence on revenues from the exploitation of natural resources can also lead to a disengagement of the state from other forms of taxation, ultimately exposing public revenues to fluctuations in commodity prices and thus the state budget to potentially highly unpredictable external shocks. Figure 2 below corroborates the findings of studies by Bornhorst et al. [2009], Thomas and Trevino [2013], and Crivelli and Gupta [2014], showing that countries with abundant natural resources also have the lowest tax rates (excluding revenues from the exploitation of these resources) among developing countries.

Figure 2: Tax revenues and the importance of the natural resource sector

Sources: BSI Economics. IMF data, WDI. Author’s calculations.

The importance of the informal sector and the institutional framework

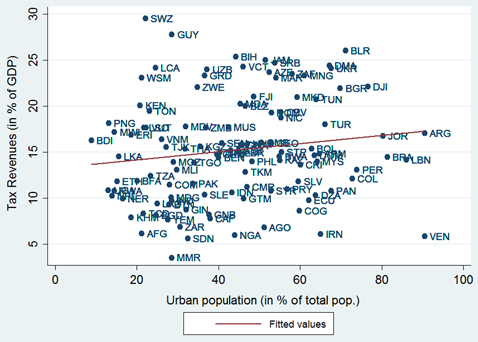

Subsequently, other studies have highlighted the importance of demographic factors in explaining the level of taxation in these economies. Although first studied by Bolnick in 1978, a number of relatively recent articles (Madhavi [2008], Mkandawire [2010]) have added population density, urbanization rate, and dependency ratio to the list of determinants of tax pressure in developing countries. Intuitively, it is quite logical to observe lower tax revenues in countries where the population is extremely dispersed and where tax collection is costly and inefficient. However, a high concentration of population in developing countries can also lead to an increase in the informal sector, which most often escapes taxation (at least direct taxation) and contributes to the erosion of the tax base. However, according to studies by Khattry and Rao [2002] and Thomas and Trevino [2013], it would appear that increased urbanization, while promoting the development of informal activities, nevertheless tends to have a positive impact on tax revenues in developing countries (see Figure 3 below).

Figure 3: Tax revenues and urbanization

Sources: BSI Economics. IMF data, WDI. Author’s calculations.

On the political and institutional side, a large number of studies have ultimately highlighted the key role played by the quality of institutions, and therefore governance, in the mobilization of domestic resources (Tanzi and Davoodi (1998), Ghura (1998), Teera and Hudson (2004), Gupta (2007), Madhavi (2008), Bird et al. (2008), Bornhorst et al. (2009), Thomas and Trevino (2013)). Intuitively, an effective and benevolent government is able to collect more domestic resources than a state that is highly corrupt and poorly involved in enforcing its tax laws. Graphically, we see a positive relationship between the level of taxes collected and the CPIA index, which focuses on the degree of transparency, accountability, and control of corruption within the public sector (see Figure 4 below).

Figure 4: Tax revenues and prevalence of corruption

Sources: BSI Economics. IMF data, WDI. Author’s calculations.

Conclusion

All these studies, as well as others not cited here, have provided a better understanding of how taxation works in developing countries, particularly in sub-Saharan Africa. Furthermore, identifying the specific determinants of domestic resource mobilization in these countries has also enabled policymakers to tailor their tax reforms to the particular context of their country. But what is the real picture of tax performance in developing countries and those in sub-Saharan Africa? Has there been a significant increase in domestic resources in these countries? A brief overview of the evolution of these revenues in SSA countries over the last decade is provided in the second part of this article to better understand where these countries stand and measure how far they still have to go.

Bibliography

Lotz, J. R. and Morss, E. R. (1967). Measuring « tax effort » in developing countries. Staff Papers, International Monetary Fund, pages 478-499.

http://www.jstor.org/stable/3866266?origin=pubexport

Bahl, R. W. (1971). A regression approach to tax effort and tax ratio analysis. Staff Papers, International Monetary Fund, pages 570-612.

http://www.jstor.org/stable/3866315?origin=pubexport

Chelliah, R. J., Baas, H. J., and Kelly, M. R. (1975). Tax ratios and tax effort in developing countries, 1969-71. Staff Papers, International Monetary Fund, pages 187-205.

http://www.jstor.org/stable/3866592?origin=pubexport

Tait, A. A., Grätz, W. L., and Eichengreen, B. J. (1979). International comparisons of taxation for selected developing countries, 1972-76. Staff Papers, International Monetary Fund, pages 123-156.

http://www.jstor.org/stable/3866567?origin=pubexport

Leuthold, J. H. (1991). Tax shares in developing economies a panel study. Journal of development economics,

35(1):173-185.

http://www.sciencedirect.com/science/article/pii/0304-3878 (91) 90072-4

Burgess, R. and Stern, N. (1993). Taxation and development. Journal of Economic Literature, pages 762-830.

Agbeyegbe, T. D., Stotsky, J., and WoldeMariam, A. (2006). Trade liberalization, exchange rate changes, and tax revenue in Sub-Saharan Africa. Journal of Asian Economics, 17(2):261-284.

http://www.sciencedirect.com/science/article/pii/S1049-0078(06)00015-7

Khattry, B. and Rao, M. J. (2002). Fiscal faux pas? An analysis of the revenue implications of trade liberalization. World Development, 30(8):1431-1444.

http://www.sciencedirect.com/science/article/pii/S0305-750X (02)00043-8

Baunsgaard, T. and Keen, M. (2010). Tax revenue and (or?) trade liberalization. Journal of Public Economics, 94(9):563-577.

http://www.imf.org/external/pubs/cat/longres.aspx?sk=18252

Gupta, A. S. (2007). Determinants of tax revenue efforts in developing countries. International Monetary Fund.

http://www.imf.org/external/pubs/cat/longres.aspx?sk=21040

Bornhorst, F., Gupta, S., and Thornton, J. (2009). Natural resource endowments and the domestic revenue

effort. European Journal of Political Economy, 25(4):439-446.

http://www.imf.org/external/pubs/cat/longres.aspx?sk=22115

Thomas, M. A. H. and Trevino, M. J. P. (2013). Resource Dependence and Fiscal Effort in Sub-Saharan Africa. Number 13-188. International Monetary Fund.

Crivelli, E. and Gupta, S. (2014). Resource blessing, revenue curse? Domestic revenue effort in resource-rich countries. European Journal of Political Economy, 35:88-101.

http://www.imf.org/external/pubs/cat/longres.aspx?sk=41205

Bolnick, B. R. (1978). Demographic effects on tax ratios in developing countries. Journal of Development Economics, 5(3):283-306.

http://www.sciencedirect.com/science/article/pii/0304-3878(78)90032-9

Mahdavi, S. (2008). The level and composition of tax revenue in developing countries: Evidence from unbalanced panel data. International Review of Economics & Finance, 17(4):607-617.

http://www.sciencedirect.com/science/article/pii/S1059-0560(08)00002-6

Mkandawire, T. (2010). On tax efforts and colonial heritage in Africa. The Journal of Development Studies, 46(10):1647-1669.

http://www.framtidsstudier.se/wp-content/uploads/2011/01/20100909124338filLOoq1WlW53k34oag3KWn.pdf

Tanzi, V. and Davoodi, H. (1998). Corruption, public investment, and growth. Springer.

http://www.imf.org/external/pubs/cat/longres.aspx?sk=2353

Ghura, M. D. (1998). Tax Revenue in Sub-Saharan Africa. Effects of Economic Policies and Corruption (EPub). Number 98-135. International Monetary Fund.

Teera, J. M. and Hudson, J. (2004). Tax performance: a comparative study. Journal of International Development, 16(6):785-802.

http://hdl.handle.net/10.1002/jid.1113

Bird, R. M., Martinez-Vazquez, J., and Torgler, B. (2008). Tax effort in developing countries and high income countries: The impact of corruption, voice and accountability. Economic Analysis and Policy, 38(1):55.