Purpose of the article: The aim of this article is to lay the essential theoretical foundations for understanding the banking issues addressed in public debate. What is money creation? What is a bank run? What role can the government play in rescuing a bank? How does the central bank influence the behavior of commercial banks? What is liquidity (or central bank money), which is so often mentioned in the financial press?

Summary:

- Seventeenth-century London goldsmiths became the ancestors of modern banks by discovering money creation as we know it today: to grant credit, all you have to do is create a deposit.

- Banks are constrained in their power to create deposits. If they abuse this power, they risk insolvency. Furthermore, the central bank has the ability to influence the lending behavior of banks. This is how it implements monetary policy.

- There are two types of bank insolvency: a bank may lack capital (on the liabilities side) or liquidity (on the assets side). Liquidity crises can be the result of self-fulfilling phenomena; if all the customers of the same bank withdraw their money, suspecting, rightly or wrongly, that it may go bankrupt, the bank quickly risks running out of liquidity.

- To limit liquidity crises, the government guarantees customer deposits, while the central bank acts as a lender of last resort.

1. Money creation by banks

1.A History of modern banking – London goldsmiths in the 17th century

To understand how modern banks operate, let’s take a look at how they came into being. It is generally accepted that money creation in its current form originated in England inthe 17th century, when certificates of deposit issued by goldsmiths became a means of payment that gradually replaced gold and silver coins.

Since goldsmiths had safes to protect the metals they worked with and offered certain banking services (e.g., currency exchange), wealthy merchants and individuals naturally entrusted their gold and silver coins to goldsmiths. In exchange, the goldsmiths gave each depositor a deposit certificate that allowed them to withdraw their money at any time. Goldsmiths then noticed that depositors rarely asked to convert their certificates of deposit into coins, and when they did, they did not do so at the same time. This was because:

- Not all depositors carried out large transactions at the same time and therefore did not have the same need for coins at any given moment.

- Certificates of deposit were increasingly used as a means of payment in commercial transactions and were gradually replacing gold and silver coins. It was therefore no longer necessary to systematically request the conversion of the certificate of deposit into coins before making a transaction.

Furthermore, coins are perfectly substitutable for one another. Goldsmiths do not need to return to depositors the coins that were entrusted to them by that same depositor at the time of deposit, but can return other coins for an equivalent amount.

Based on these observations, goldsmiths realized that it was not necessary to mobilize all the coins they held to meet daily withdrawal requests. Goldsmiths could estimate the maximum amount of coins their customers would request in a day and lend the rest to earn interest. This is how money creation as practiced by modern deposit banks came into being.

To lend, the goldsmith simply had to create a new deposit certificate and give it to the borrower. The total amount of deposit certificates in the economy increased instantly by a simple bookkeeping entry, without any change in the total amount of coins in circulation. The borrower, holder of the new deposit certificate, has the same rights as any other depositor. They can decide to withdraw coins from the goldsmith or use the deposit certificate as a means of payment in a transaction. As long as the goldsmith has more gold than is necessary to meet the daily withdrawal requests of depositors, they can repeat the operation and create new deposit certificates.

The borrower had to repay the loan when it matured, thereby destroying the certificate of deposit that had been created when the loan was granted. The interest received by the goldsmith in return for the loan enabled him to pay interest (at a lower rate, as the goldsmith obviously retained a margin) to his customer-depositors in order to attract new ones, thereby increasing his stock of coins and thus his lending capacity.

1.B Money creation and the balance sheet of a deposit bank

In this section, we will reconstruct the simplified balance sheet of a modern deposit bank based on various transactions since its inception, drawing on the parallel that can be drawn with17th-century London goldsmiths.

First, we should remember that a balance sheet’s liabilities show the company’s sources of financing, while its assets show the company’s possessions (i.e., how the financing has been used).

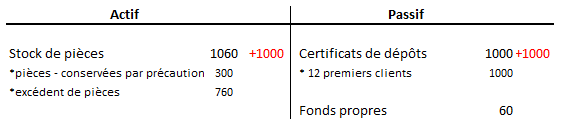

1. Let’s imagine that a London goldsmith’s apprentice decides to set up his own business, aware of the potential offered by the deposit/loan activity he can develop. He has recently inherited and has a starting sum of 60 gold coins, which he intends to use to develop his business. Let’s analyze the impact on the goldsmith’s apprentice’s balance sheet:

2. Twelve customers deposit a total of 1,000 coins, and the goldsmith issues the corresponding certificates of deposit. He decides to require himself to keep at least 30% of the amount of the certificates of deposit issued in the form of coins to cover any withdrawals.

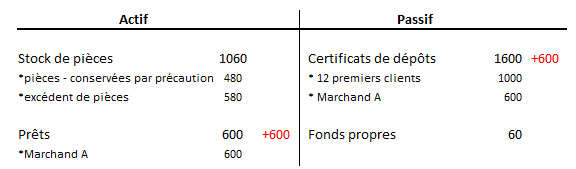

3. Merchant A wishes to borrow 600 coins, and the goldsmith grants him credit by creating a new certificate of deposit. Each time a loan is granted, the total amount of deposits increases, and money (i.e., deposits) is therefore created.

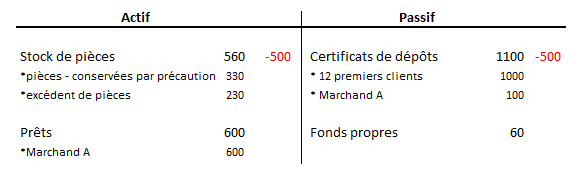

4. Merchant A withdraws 500 coins for whatever purpose.

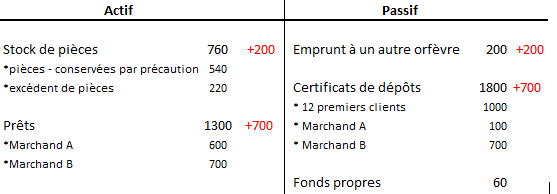

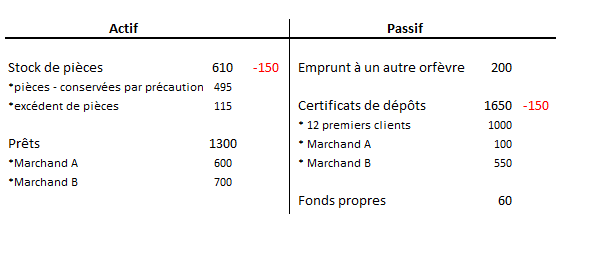

5. Merchant B wants to borrow 700 coins for a short period. The goldsmith is in a difficult situation: he knows that B is a good borrower (the risk of non-repayment is low), but he has committed to keeping 30% of his deposits in his vaults in the form of coins, a rule he will no longer be able to comply with if he grants this loan. He decides to borrow 200 coins from another goldsmith and then grants the loan.

6. Merchant B converts part of his deposit into coins (150 coins) to spend.

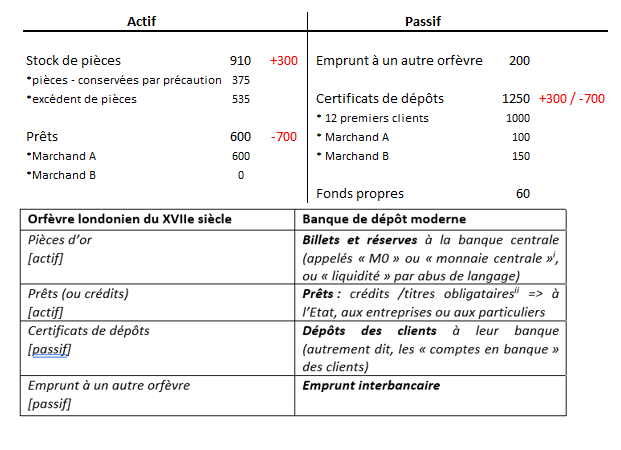

7. Merchant B is paid 300 coins by one of his customers and deposits them with the goldsmith. At the same time, he repays his loan (700).

Before reconstructing the balance sheet of a modern deposit bank, let’s match certain components of the goldsmith’s balance sheet with their equivalents in modern banks.

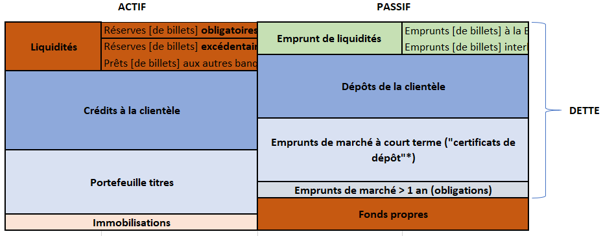

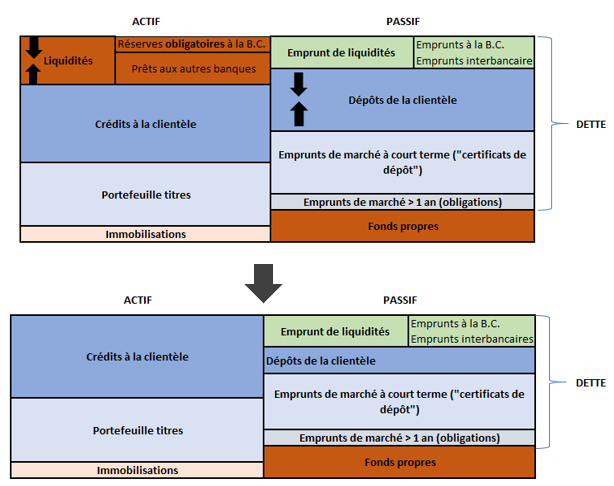

Let’s slightly complicate our goldsmith’s balance sheet to obtain that of modern deposit banks. In addition to customer deposits, another source of financing must be added: funds borrowed on the financial markets (mainly from institutional players). On the asset side, modern deposit banks lend to the economy (businesses, households, the government, etc.) either by granting loans or by purchasing bonds on the financial markets. The balance sheet of a deposit bank can be simplified as follows:

NB: It should be noted that when a customer of a modern bank makes a transfer/payment to a recipient who is a customer of a second bank, the impact of the transaction on the balance sheet of the initial bank is comparable to that of a withdrawal by one of the depositors (concomitant decrease in reserves (assets) and deposits (liabilities)).

1.C Commercial banks create money (bank deposits), but the central bank has the power to influence the behavior of banks

Although commercial banks create money (i.e., by granting loans, banks create new bank deposits), the central bank has the ability to influence the behavior of banks in order to encourage them to increase or restrict the supply of loans (and therefore the creation of deposits) to the economy: this is known as monetary policy.

As we have seen, a bank’s ability to lend depends on its ability to obtain central bank money (banknotes and bank reserves at the central bank). Unlike in the days of London goldsmiths, when gold and silver coins were in limited supply in a country, central bank money is now a variable mass controlled by the central bank (the central bank can print banknotes or create reserves). To implement its monetary policy, the main tools available to the central bank are to facilitate or restrict central bank money in the banking system and to manipulate the cost of obtaining ( the « refinancing rate » at which commercial banks can borrow central bank money from the central bank) and holding (the rate of return on reserves) central bank money by banks, i.e., the key interest rates. When the economy is overheating, the central bank raises key interest rates, which has the effect of slowing down bank lending activity and, therefore, economic activity. Conversely, when the economy is growing below its potential, the central bank lowers key interest rates, which has the effect of stimulating lending activity and, therefore, economic activity.

2. The natural limits of money creation: risk management by banks

2.A What is insolvency?

Banks cannot create money indefinitely or lend to borrowers without analyzing their ability to repay. Like all businesses, banks can become insolvent and risk bankruptcy. Insolvency is the situation of a company that cannot pay its debts. There are two types of insolvency:

- For various reasons, the total value of assets becomes less than the total amount of debt. The net value of the company is then said to be negative. The company would not be able to repay all of its debts if it sold all of its assets at market value.

- The company does not have sufficient liquidity (in the broad sense: central bank money and assets that can be easily converted into central bank money) to meet its immediate obligations. The company is insolvent due to illiquidity. This situation can occur even though the company has more assets than debts.

The unique nature of banking makes effective management of these risks essential. Deposit banks collect deposits and other forms of short-term financing and lend on a long-term basis ( mortgage loans, long-term loans to businesses to finance their investments, etc.). They are said to « transform maturities. » As a result, more than other companies, banks’ balance sheets have specific characteristics:

- The significant maturity mismatch between their assets (long-term) and liabilities (short-term) is the source of liquidity risk.

- Their debt is very high relative to their equity (this is referred to as significant « leverage »). Banks must be careful not to lend too much or to borrowers who are too risky.

2.B Examples of bank insolvency?

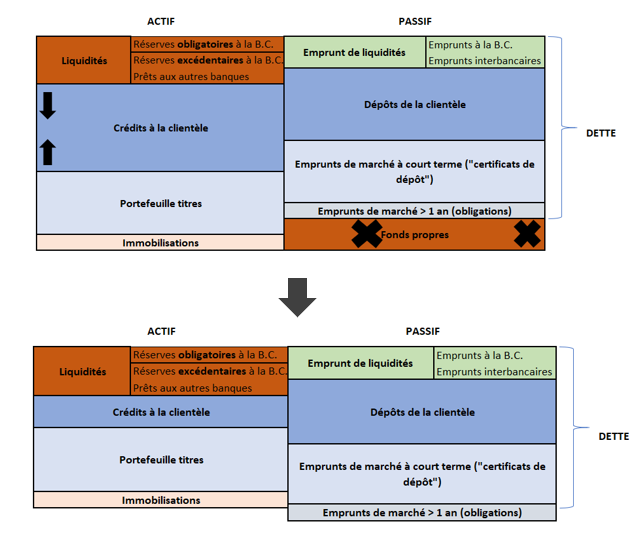

Let’s imagine a bank in a healthy position with a simplified balance sheet similar to the one shown above. The bank’s net value is positive because the value of its assets exceeds that of its debts, which reflects the presence of equity. This equity serves as a safety cushion when the bank incurs losses.

Case 1: Several customers announce that they will not be able to repay the loan granted to them by the bank.

The losses reduce the bank’s capital, which acts as a buffer. Once the capital is exhausted, further losses reduce the value of the assets to below the value of the debts. Even if the bank sold all its assets, it would not be able to repay all its creditors.

Case 2: The bank’s customers begin to fear for its solvency and withdraw their money en masse

At this point, the bank is still technically solvent (assets exceed liabilities), but it urgently needs cash (banknotes or reserves) to meet its customers’ withdrawal and transfer requests. If the bank is unable to borrow cash immediately, the only solution will be to sell its less liquid assets (securities, loans, etc.). However, in order to sell them quickly, the bank risks selling them off at a price below their market value. The bank will then incur losses, which will reduce its equity capital to the point where it may become insolvent (see case 1).

2. C Overview of tools to limit the risk of banking crises

The failure of a bank can threaten the entire banking system. First, the interconnections between banks pose a risk of a chain of failures, as the creditors of the insolvent bank may not be repaid. Furthermore, liquidity crises can arise from simple fears (whether justified or not) and become self-fulfilling. If one bank fails, everyone will tend to worry about the solvency of their own bank. Customers’ fear of not being able to recover their money may prompt them to withdraw or transfer their deposits (hoping to get there before other customers), thus creating liquidity pressures. If several banks experience this phenomenon, general anxiety increases, further exacerbating liquidity problems.

Banking crises are harmful to the entire economy. It is therefore logical for public authorities to question their role in containing banking crises. However, public intervention is criticized, in particular because it creates what is known as moral hazard: banks take more risks because they believe they are protected by the state in the event of difficulties.

In addition to prudential regulation, public institutions have several tools at their disposal to preserve the stability of the banking system. In particular, they can:

- Recapitalize banks that no longer have sufficient capitalwith public funds when they are considered « systemic. » This lever, known as a « bailout, « was used in several countries following the 2008 crisis.

- Guarantee bank deposits to reassure depositors and prevent bank runs. The introduction of this public guarantee in the United States in 1934, following the Great Depression of 1929, instantly reduced the number of bank failures.

- Acting as lender of last resort. During bank runs, the central bank must lend as much liquidity as requested by banks that are able to provide it with high-quality (illiquid) assets as collateral. In other words, the central bank temporarily buys back illiquid assets that commercial banks would be unable to sell in an emergency to obtain liquidity. This role, conceived in the19th century by Walter Bagehot, has helped to prevent the spread of numerous liquidity crises. The European Central Bank made particular use of it during the 2008 crisis.

Conclusion

Seventeenth-century London goldsmiths invented money creation as practiced by modern banks. To grant a loan, the bank creates a deposit. In other words, it credits the borrower’s bank account with a simple book entry. However, if banks abuse money creation (by lending too much or to defaulting borrowers), they risk becoming insolvent. The failure of one bank can easily spread to other banks given the interconnections between them and the self-fulfilling nature of liquidity crises.

Since banking crises have a severe impact on a country’s economy, public authorities put mechanisms in place to limit them. In the eurozone, control of the money supply (i.e., monetary policy) is a prerogative that member states have entrusted to the European Central Bank (ECB) and which is exercised through commercial banks. However, until recently, the stability of the banking system was a mission largely shared between national authorities and the ECB. The financial crisis of 2008 and then the eurozone crisis of 2011 highlighted this inconsistency, prompting eurozone member states to take action. It was to fill this gap that the Banking Union project was launched in 2012 (see BSI article » The Banking Union put to the test » ). Still incomplete in 2019, it is based on three pillars: 1) a single resolution system for bank failures in the eurozone, 2) a single supervisory mechanism for banks, and 3) a common deposit guarantee fund.

Disclaimer: the mechanisms explained in this article are often simplified for ease of understanding.

Sources:

https://www.academia.edu/5097471/Money_Creation_Genesis_2_Goldsmith-Bankers_and_Bank_Notes

https://positivemoney.org/how-money-works/advanced/how-do-banks-become-insolvent/

http://www.bsi-economics.org/804-union-bancaire-a-l-epreuve-ga

https://www.linkedin.com/pulse/why-banks-fail-definitive-guide-solvency-liquidity-ratios-rochford/

http://www.cadtm.org/Banques-Le-bail-in-est-il-une-solution

http://www.bsi-economics.org/804-union-bancaire-a-l-epreuve-ga