Usefulness of the article: Following the first default in its history on March 9, 2020, where does Lebanon stand today? This article reviews the main factors that led the country to the current crisis and lays the groundwork for reflection on the unfolding of future events.

Summary:

- Poor management of public finances in Lebanon and endemic corruption have led to a very significant increase in public debt (158% of GDP in 2019).

- The « financial engineering » system developed by the Banque du Liban, which consisted of attracting dollar deposits to finance the large twin deficits, ultimately failed to prevent the default that occurred in March 2020.

- The economic crisis in Lebanon is affecting all levels of the economy.

- With foreign exchange reserves depleted and the country heavily dependent on imports and remittances from abroad, Lebanon is now seeking to restructure its public debt by negotiating with its creditors.

- One way out of the current crisis for Lebanon could be to restructure the banking system by creating new public banks, public investment funds, cooperatives, and other institutions capable of stimulating economic development.

Lebanon is currently experiencing a multiple crisis: the first default in the country’s history, a shortage of dollars, severely limited bank withdrawals, higher cost of living, a drop in the value of the pound on the parallel market, high levels of corruption, etc.

Since October 2019, the Lebanese people have been protesting against deteriorating economic conditions, ineffective public policies, and corruption (Lebanon ranks 137th out of 180 countries in 2019 in terms of perceived corruption according to the Transparency International Index). This movement began after a week in which the authorities demonstrated their inability to manage major fires and following the introduction of a tax on the use of the WhatsApp phone application. These protests led to the resignation of the government.

The formation of a credible new government was the first step in enabling the country to take legitimate measures and potentially receive assistance from the International Monetary Fund (IMF) and/or financial aid from partner countries. However, this assistance would remain conditional on the rapid implementation of reforms by the authorities or at least a short-term plan.

However, at this stage, no such plan has been finalized, leaving Lebanon with very few options given the situation (depletion of dollar reserves, imminent major public debt repayments). Consequently, on March 7, 2019, the government’s lack of room for maneuver prompted it to announce, for the first time in its history, a default on a Eurobond[1]maturing on March 9 (worth USD 1.2 billion).

1. A crisis at all levels

Lebanon is suffering from an economic, banking, monetary, and sovereign crisis.

1.1 The banking system and financial engineering

For many years, the Lebanese economy has suffered from high twin deficits (budget and current), which are usually financed through bond issuance, remittances from the Lebanese diaspora (according to Goldman Sachs in December 2018), or other types of investment flows (foreign bank deposits, for example).

To finance these deficits, the government and the Central Bank of Lebanon (BDL) have chosen to rely heavily on the local banking system to finance the public deficit so as not to have to pay excessively high interest rates on the international capital market. This situation has been facilitated by « financial engineering » and a strategy of high deposit remuneration, so that:

- Banks have the financial resources necessary to acquire public debt securities;

- And attract dollar deposits in order to have USD available to carry out sterilized open market operations[2] to maintain the Lebanese pound (LBP) peg to the USD and thus limit inflationary pressures.

This is an expensive system, especially if the twin deficits widen and no reforms are implemented, with a significant crowding-out effect on access to credit and low price competitiveness. This system has been particularly costly, even unfair and controversial, especially since some studies estimate that 40% of Lebanese commercial banks’ assets belong to political figures, leading to conflicts of interest (see the study by economist J. Chaaban published by the Economic Research Forum in 2016, entitled « I’ve got the power »).

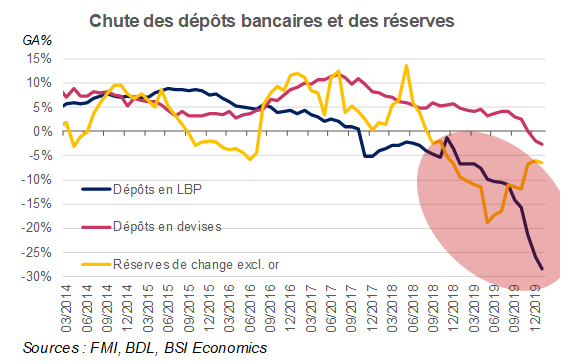

In an interview on CNBC, economist N. Zouk of Oxford Economics likened this modus operandi to a Ponzi scheme: the banking system collects deposits (in return for remuneration) and uses them to finance the public deficit, relying in particular on « new deposits » to continue to remunerate « old » depositors. Such a scheme is sustainable as long as deposits continue to flow in, but as soon as deposit growth slows or contracts, this is no longer the case. In the second half of 2019, bank deposits in Lebanon contracted by 3.6% (year-on-year), with a particularly sharp fall in deposits denominated in Lebanese pounds (-16.5% year-on-year, see chart below). In addition, many Lebanese depositors were able to transfer their money abroad, despite the exchange controls applied by banks.

Dollars and deposits are guaranteed by the Central Bank (BdL), while dollar liquidity in the system depends on the growth of USD deposits, attracted by the high returns on this type of deposit, in line with the monetary policy pursued by the BdL. However, since the last quarter of 2019, dollar deposits have been leaving the country and the BdL does not seem to be able to reverse the trend. This downward trend is unlikely to be reversed in the short term and only financial assistance (via donors or, for example, within the framework of CEDRE[4] ) could alleviate the dollar liquidity stress.

In addition, other flows have tended to dry up at the same time. In the case of expatriate remittances, this could potentially be explained by lower fuel prices, affecting producer countries and the employment and income dynamics of expatriates working in these countries (bearing in mind that the largest share of remittances comes from the Gulf countries). These flows tend to slow down and then contract, particularly foreign bank deposits, in line with the gradual deterioration of international confidence in the country.

1.2 BDL reserves

At the beginning of March 2020, the BdL claimed to have $29 billion in gross foreign currency reserves. However, a report published in February by Fitch estimated that its foreign currency liabilities exceeded its assets, giving the Bank of Lebanon a net negative foreign currency position of nearly $40 billion, excluding gold. N. Saidi, former deputy governor of the central bank, estimates that usable reserves have fallen to around $3-4 billion (FT) due to deductions from commercial bank deposits that the BdL cannot access because of reserve requirements, as well as BdL loans to local institutions ($6-7 billion) to help them cover their commitments to correspondent banks.

1.3 The US dollar against the Lebanese pound

An economy that is 72% dollarized is facing a shortage of dollars and is therefore unable to repay its debt (Eurobonds, more than 50% of which were now held by non-residents). In other words, this means a simultaneous decrease in the supply of USD/LBP in the Lebanese economy, an increase in demand for USD/LBP by Eurobond holders, and growing speculation about Lebanon’s ability to repay and its overall situation. Such a situation has the effect of causing a depreciation of the Lebanese pound against the dollar on the black market.

In February 2020, the Lebanese pound is still officially pegged to the dollar at 1,507, but has lost more than 60% of its value (according to Reuters), as local banks ration the dollars needed to import food, medicine, and other essential goods.

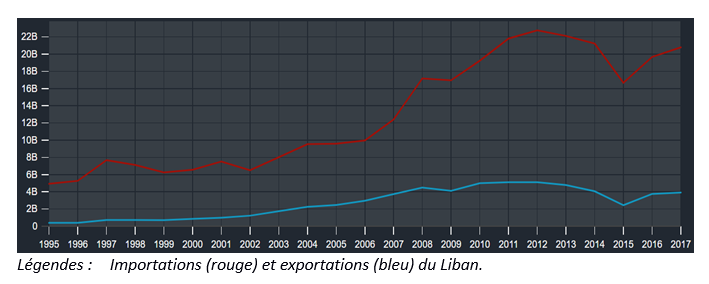

This internal depreciation is hurting imports, on which Lebanon depends mainly for consumption (see chart below), thereby fueling inflation for these products. Prices in supermarkets are now doubling, reducing the real income of consumers who are already under severe pressure (according to Infopro). Fuel and bread (subsidized by the government) are roughly the same price. At the same time, the government is considering a potential fuel price increase of 5,000 Lebanese pounds in an attempt to boost tax revenues.

Trade in Lebanon (USD million)

2. Focus on debt

Lebanon’s debt level stood at 158% of GDP at the end of 2019, the fifth highest in the world after Japan, Venezuela, Sudan, and Greece (World Population Review). Even during periods of acute crisis, the Lebanese government had never defaulted on a single payment. However, it was unable to make the most recent payment on March 9 on the $1.2 billion Eurobond[2]. This automatically further undermines the confidence of international markets in the Lebanese sovereign issuer.

A default was supported, in particular, by economists and financial experts who argue that Lebanon should use its reserves to finance the purchase of essential imports to meet the needs of the population instead of paying its creditors on time. Local banks, on the other hand, which held some of the Eurobonds maturing on March 9, opposed default, arguing that it would put pressure on the sector and jeopardize Lebanon’s ties with foreign creditors. However, as Lebanese officials said, paying the debt in March would have been « suicidal » given the state of reserves and the urgency of importing essential goods.

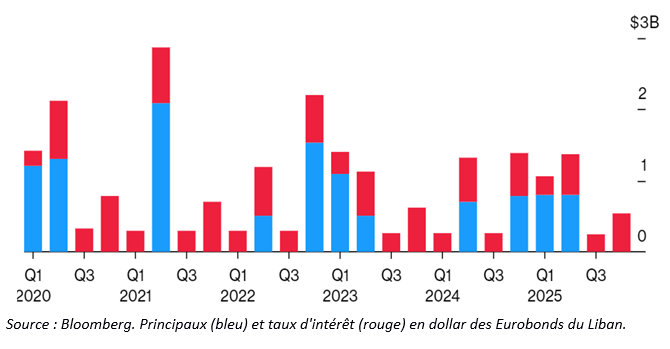

The government is currently preparing negotiations with its creditors for debt restructuring, with Lazard Ltd. and Cleary Gottlieb Steen & Hamilton acting as legal and financial advisors. For 2020, US$700 million is due in April and US$600 million in June (see figure below).

[1] A Eurobond is a bond denominated in a currency other than that of the issuing country. In the case of Lebanon, these are mainly bonds denominated in US dollars.

[2]Monetary operations consisting of intervening in the foreign exchange market on a daily basis to sell/buy currencies in order to maintain the parity of the central currency against the reference currency (the US dollar in the case of Lebanon). In some cases, these operations may involve significant injections of liquidity, which can lead to upward pressure on the general price level without sterilization. The sterilization of open market operations then consists of using other monetary policy tools, such as the issuance of certificates of deposit in the case of Lebanon, aimed at withdrawing a portion of this liquidity to avoid the emergence of inflationary pressures.

[3]The crowding-out effect stems from the fact that local banks are heavily solicited to purchase public debt securities when the public deficit is structural, devoting a large part of their activity to this mechanism, to the detriment of credit distribution to the private sector, whose access to bank liquidity is then reduced.

[4] CEDRE is the international conference on financial support for Lebanon, which resulted in a commitment of around €9 billion in loans to modernize Lebanon’s economy. However, at this stage, the country still does not meet the conditions to benefit from the aid.

[5]As recently as November 2019, Lebanon made a payment of more than $1.5 billion in Eurobonds, sending a positive signal that the government was ready to meet its commitments.

[6]As the March 9 maturity date for the $1.2 billion Eurobond approached, the price fell from 90 cents on the dollar in early February to a record low of 53 cents, with an interest rate exceeding 1,000%.

[7]Growth bonds are bonds that stipulate that the capital must be locked in for an agreed period, usually 3 to 5 years, in order to provide the country with a certain level of growth.