This brief note aims to decipher a striking chart related to current economic events. At a time when gold is rapidly increasing in importance in global reserves, this Killer Chart examines this phenomenon and the increasingly widespread misconception that links this surge in gold to a loss of confidence in the US dollar (USD).

Download the PDF:

Why is this interesting?

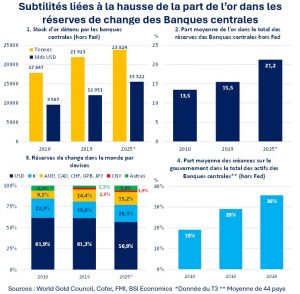

Since the health crisis, central banks’ foreign exchange reserves have risen sharply, particularly in connection with the acceleration of gold purchases. The volume of gold held by CBs rose from 21,923 tons in 2019 to 23,824 tons in the third quarter of 2025[1] (see yellow bars in Chart 1 of the Killer Chart). Four countries stand out among those with the largest increases in volume, exceeding 200 tons: China, Poland, India, and Turkey.

The volume effect was accompanied by a significant price effect, linked to the sharp rise in the price of gold (+184% between the end of 2019 and the end of 2025), which automatically increased the value of central banks’ gold holdings[2]. As a result, the value of gold reserves expressed in billions of USD grew faster (blue bars in Figure 1) than volumes. Mechanically, the share of gold in total central bank foreign exchange reserves has increased by +6 ppts since 2019 to reach 21.2% at the end of 2025. This trend appears to be global and independent of the level of development: Austria, Egypt, Ecuador, Uzbekistan, Poland, Qatar, Russia, and Turkey are among the countries with the largest increase in the share of gold in their reserves.

It would be tempting to conclude that central banks have recently changed their strategy, with gold becoming a substitute for US Treasury bonds and the US dollar (USD) in a context where countries are seeking to move away from the dollar. However, this conclusion is incorrect, or at least largely incomplete.

What are we to make of this?

The geopolitical dimension is certainly a factor in the transformation of the composition of some central banks’ foreign exchange reserves, but these are actually quite specific cases. This is particularly true of Russia, which is subject to US sanctions and is seeking to avoid exposure to the USD, finding an alternative in local gold storage.

However, this is not necessarily the case for China. While China has reduced its dollar holdings[3] at the same time as increasing its gold purchases, it is important to remember the underlying macroeconomic context. From 2014 to 2024, the Chinese banking system, supported by the central bank, intervened massively in the foreign exchange market to support the yuan. To do so, banks resorted to systematic net sales of foreign exchange reserves (except in 2020-2021). Since 2025, this trend has reversed and net purchases of foreign currencies, including the dollar, have become the norm in order to prevent the yuan from appreciating too sharply. Furthermore, since 2021, Hong Kong, China’s offshore financial center, has been rebuilding its stock of US Treasury bonds, which reached an all-time high of USD 268 billion at the end of 2025. Contrary to popular belief, China’s arbitrage decisions are not solely motivated by geopolitical considerations, and the country is not really following the path of a country disengaging from the dollar. Geopolitics may accelerate the process of gold acquisition, but it remains a secondary factor.

The main reason stems from the diversification of foreign exchange reserves, a strategy that central banks have been pursuing for many years. This strategy can be seen in the composition of foreign exchange reserves by currency (see Chart 3), where the share of the USD is gradually declining in favor of other currencies, mainly the euro in recent years, but also the Canadian and Australian dollars and even the Korean won. There are various reasons for this strategy: smoothing the impact of USD fluctuations, seeking higher returns, increased accessibility of other currencies and currency risk hedging tools, etc. (for more information, read this Killer Chart). Gold acquisitions follow a similar logic. However, this diversification into gold may seem surprising, given that gold is by nature less liquid than other reserves, does not provide any return (unlike bonds), and even has a storage cost. Thus, the opportunity cost of holding gold appears to be significant for central banks.

Beyond the diversification challenges that gold can address, CBs find another advantage in increasing the share of gold reserves. These reserves have a stabilizing effect on their balance sheets. As the value of gold has risen sharply in recent years, this offers opportunities for capital gains on gold sales. These capital gains can partly feed into the CBs’ equity capital, which is valuable in helping them absorb potential losses.

This point is all the more important given that the share of domestic government debt has risen sharply on average since 2020 ( see Chart 4). As these debts generally take the form of bonds, this situation exposes central banks to unrealized capital losses when interest rates rise. However, since the energy crisis of 2022, bond yields have tightened. Although they have fallen since 2025, they remain higher on average than during the pre-health crisis period, posing a risk of real losses for CBs when these bonds mature or need to be sold. CBs could now draw on their gold reserves to absorb potential losses on their bond portfolios.

The revaluation account mechanism could also provide additional leverage to absorb losses. When a CB holds gold that it values at market value, in a context of rising gold prices, the resulting increase in assets translates into an equivalent increase in liabilities via this mechanism. However, this increase in liabilities does not mean an increase in the CB’s equity (as the capital gains are unrealized and therefore cannot be included in the income statement). Furthermore, the gold revaluation account is not transferable (i.e., it cannot be used to cover capital losses recorded on other asset classes[9]), which suggests that it cannot be used to absorb losses. However, there is a recent precedent: South Africa.

In 2024, South Africa circumvented these obstacles, facilitating a transfer of the gold revaluation account (for more information, see this Fed note). Although to date there is no legislation specifically providing for this possibility in most countries (and it is even prohibited in the eurozone), a scenario similar to that in South Africa[10] cannot be ruled out as a last resort[11]. In a context of renewed volatility (in currencies, bonds, etc.), this alternative use of gold could therefore complement the arsenal of central banks.

The strategy of gold holdings by central banks is therefore part of a much broader macroeconomic context than the perception of geopolitical risk or mistrust of the dollar. The process of diversifying foreign exchange reserves thus helps to stabilize their balance sheets and facilitate the conduct of monetary policy. This is a key point, given their decisive role in many areas: inflation management, financial stability, exchange rate stability, economic growth, etc. (depending on their mandate). On the other hand, central banks are now becoming more sensitive to the volatility of gold prices, and the status of gold in global reserves may well change in the coming years.

V.L, article written on February 22, 2026

[1] Author’s calculations, based on World Gold Council data for 90 countries.

[2] It should be noted here that not all central banks value their gold assets in the same way. While the US Federal Reserve values gold at the 1973 price (in accordance with US law), most other central banks use market value. Some central banks value gold at a « historical » price, allowing for occasional revaluations (South Africa and Lebanon, for example).

[3] The amount of US Treasury bonds held by China has been divided by almost two since 2014 (with USD 683.5 billion at the end of 2025, China nevertheless remainsthe third largest holderin the world outside the US). Furthermore, this decline does not necessarily correspond to sales of US bonds, but rather to China’s failure to renew its demand when US bonds reach maturity.

[4] Between May 2025 and January 2026, net currency purchases by Chinese banks reached USD 338.4 billion.

[5] Despite ambitions to internationalize the yuan, see chapter 6 of the BSI Economics book « 12 Economic Keys to Approach 2030 » (V. Lequillerier and E. Banh).

[6] The financing needs associated with the massive increase in public deficits during the health crisis were mainly covered by the domestic banking system, with central banks playing an important role. As a result, their stock of government bonds and their share of total assets increased significantly.

[7] Due to the inverse relationship between bond prices and yields.

[8] According to the European Central Bank report at the hyperlink: « The euro equivalent of the ECB’s gold holdings increased by €10.5 billion […] mainly due to the rise in the market price of gold, expressed in euros. This increase also led to a corresponding increase in the ECB’s gold revaluation accounts (see Section 1.3.2 « Net equity »). »

[9] Although this happened in Italy in 2002, it is no longer possible in the euro area, see Articles 16 and 18 of Chapter III of the following texts. There are similar points in the texts governing the scope of action of other central banks around the world.

[10] Given that this operation did not cause mistrust in the country: there were no negative repercussions on capital flows, the rand, or bond yields.

[11] For example, in the event of losses that would pose a lasting threat to the solvency of the monetary institution, preventing it from carrying out its tasks.

[12] For more on this aspect, read this Killer Chart or refer to this article by C. Weiss (2025).