Abstract :

· Financial inclusion indicators in Africa are all below the global average: 35% of the population has a bank account, 15.4% saves with a financial institution, and 6.7% has credit with a financial institution.

· Mobile banking platforms offer great hope for improving financial inclusion on the continent, as exemplified by the Kenyan leader M-PESA;

· Education and income increase the likelihood of financial inclusion. Gender and age play a less important role.

· Financial exclusion is more related to factors experienced by the African population than to conscious choices. Legislators and prudential authorities therefore have a role to play.

Access to finance is a major challenge for economic development. It enables individuals to develop their projects and integrate into society, businesses to invest, innovate, and hire, and the economy as a whole to function. In order to address the major challenges they face, African countries are particularly confronted with the difficult task of raising funds to finance themselves. One of the continent’s major challenges is therefore financial inclusion.

An individual’s financial inclusion can be defined as their access to basic formal financial services. A person is said to be financially included when they have a bank account, the ability to open a savings account and take out a loan, and the possibility of using banking services such as obtaining a credit card or using a mobile phone for payments. Formal financial services must be available, accessible, and affordable. In this article, we will attempt to shed light on the issue of financial inclusion for individuals in Africa, a fundamental concept for inclusive and sustainable development on the continent.

What are the challenges of financial inclusion?

At the microeconomic level, financial inclusion makes it possible to finance projects, whether personal or professional. Individuals can thus invest in future projects such as education or the purchase of real estate, which ultimately benefits the economy as a whole. At the company level, financial inclusion facilitates activities and procedures such as paying salaries or suppliers. At the state level, financial inclusion allows for better control and regulation of economic activities and facilitates the payment of taxes or subsidies.

However, many individuals in Africa encounter difficulties when it comes to raising funds, particularly when it comes to formal fundraising. Indeed, the informal financial system in Africa is still significant and poses the problem of state control over the flows exchanged. Financial inclusion often clashes with informal finance, even though the two phenomena are not incompatible within the same economy. In this study, we will focus on the financial inclusion of individuals. The issue of access to formal financial services for businesses will not be addressed here.

Financial inclusion in Africa: some figures

Source: World Bank Global Findex Database 2014. BSI Economics

Let’s start by looking at the financial inclusion of individuals in Africa. Although they have increased since the first questionnaire conducted by the World Bank in 2012 (Global Findex Database 2012), financial inclusion indicators are all lower in Africa[1] than the global average (see chart above). Thirty-five percent of the African population has a bank account, compared to 61.5% worldwide. While 27.4% of the global population has formal savings, only 15.4% of Africans deposit funds in a financial institution. Finally, 6.7% of the African population has taken out a loan from a financial institution in the last 12 months, compared to 10.7% globally. Looking at these figures, one question arises: are the savings and credit figures linked to a cultural tendency to save less and borrow less on the continent? It would appear not. According to World Bank figures, 56.3% of the African population say they have saved money in the last 12 months, compared to 56.5% globally. The African continent is following the global trend in terms of savings. As for credit, the African continent seems even more inclined to borrow, with 51.4% of the African population admitting to having taken out a loan in the last 12 months, compared to 42.4% globally. Such figures further demonstrate the importance of the informal sector for savings and credit.

Mobile banking, a growing phenomenon on the continent, is an exception: only 2% of the global population has a mobile account, compared to 13% of the African population. Many African economies are developing mobile banking services, with Kenya leading the market with its M-PESA mobile payment system. Created in 2007, M-PESA is a mobile payment platform owned by the operator Safaricom. The service was initially created to enable individuals to send and receive money easily. Safaricom has gradually developed new services, such as M-Shwari, which allows individuals to deposit their savings to earn interest and take out microloans, and Lipa Na M-Pesa, a payment tool that allows individuals to pay their bills directly via their mobile phones. Since its creation, M-PESA has transformed the Kenyan financial system and enabled many individuals to become financially included thanks to its much greater geographical coverage than banks. Today, 18 million Kenyans use this service, representing 70% of the adult population. And its success does not stop at Kenya’s borders, as 30 million people worldwide are believed to use this service. In 2011, transactions between individuals accounted for 30% of Kenya’s GDP. Much less developed in the rest of the continent, mobile banking is generating great hope in the rest of Africa, where individuals still have very little access to banking services but where the proportion of people with mobile phones is growing steadily. Such a system increases financial inclusion by giving marginalized and poor people access to financial services.

What microeconomic factors influence financial inclusion?

Are individuals equal in terms of access to formal finance in Africa, or are there disparities? To answer this question, we refer to the article » The determinants of financial inclusion in Africa » (Zins & Weill, Review of Development Finance, 2016). The microeconomic characteristics that most influence a person’s financial inclusion are education and income. With regard to education, the probability that a person who has completed tertiary education will have a bank account increases by 44%, that they will have formal savings by 31.9%, and that they will have a bank loan by 10.1%.

On the other hand, when an individual is in the poorest quintile of the population, the probability of having a bank account decreases by 21%, the probability of having formal savings by 10.6%, and the probability of taking out a formal loan by 3.70%. Gender and age also play a role, but to a lesser extent. Being a woman reduces the probability of having a bank account by 3.1% and the probability of having formal savings by 1.3%. The use of mobile banking services is impacted by the same microeconomic factors.

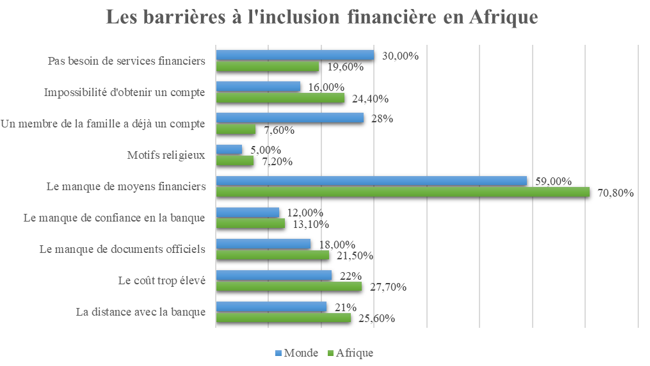

Barriers to financial inclusion in Africa

Another fundamental question to ask is: how can financial inclusion in Africa be improved? To answer this question, we need to understand the barriers and difficulties that the African population faces when it comes to formal finance. When talking about barriers to financial inclusion, it is important to distinguish between « voluntary » and « involuntary » exclusion.

Source: World Bank Global Findex Database 2014. BSI Economics

« Voluntary » exclusion is linked to microeconomic choices not to use formal financial services; exclusion occurs on the demand side of financial services. Religious reasons and the fact that a family member already has an account are examples of « voluntary » barriers. We will look at Islam to illustrate the religious barrier. Sharia (Islamic law) defines a number of principles in financial matters. Interest rates, riba, uncertainty, gharar, and speculation, maysir, are prohibited. It is forbidden to finance certain sectors of activity, such as alcohol production, as these are considered haram; they are illegal under Sharia law. Finally, the projects financed must be rooted in the real economy and subject to profit and loss sharing between the financier and the financed. Islamic finance offers individuals financial services that comply with the Sharia principles outlined above. However, this form of finance is still very underdeveloped on the African continent, which may explain the financial exclusion of individuals who wish to have access to financial services that respect their religious values. Indeed, 30% of the population of Sub-Saharan Africa is Muslim, representing 248,420,000 individuals.

« Unintentional » barriers arise from factors that exclude a population; exclusion occurs more on the financial services supply side. For example, distance from the bank, excessive costs, and lack of official documents are « unintentional » barriers. We will focus on this last barrier to illustrate our point. African banks have excess liquidity on their balance sheets. This phenomenon is problematic because it is responsible for low intermediation by banks. Nketcha and Samson attempt to explain this excess liquidity of African banks in their article (Review of Development Finance, 2014). The authors conclude that this is a precautionary strategy: banks on the continent adopt this behavior to protect themselves against the risk of a liquidity shortage. To insure themselves against this risk, they require significant guarantees from their customers. However, the latter do not always have the necessary collateral or official documents.

The most significant barrier in Africa is the same as at the global level: lack of financial resources (70.8%). We can then see that the main obstacles are « involuntary » obstacles: excessive cost (27.7%), excessive distance from the bank (25.6%), and lack of official documents (21.5%). « Voluntary » barriers, such as religious reasons and the fact that a family member already has an account, are the least significant factors (7.2% and 7.6% respectively).

It is therefore important to note that barriers to financial inclusion are most often experienced by African populations. Reducing costs, improving the geographical coverage of branches, and improving access to administrative documents can be effective ways to increase financial inclusion. Effective banking regulation also plays an important role in ensuring proper monitoring of banks and increasing intermediation. The problem of excess liquidity in African banks could be reduced, for example, by establishing a deposit guarantee fund.

Conclusion

Despite an increase in financial inclusion in Africa, the continent still scores below the global average on indicators. The financial exclusion of the African population is mainly linked to « involuntary » factors. People suffer from the high cost of financial services, the excessive geographical distance from banks, and the lack of official documents.

In terms of microeconomic determinants, being a wealthy, educated, and older man increases the likelihood of financial inclusion, with education and income being the most influential factors. Access to formal financing is a major challenge for the continent’s development, but it must correspond to a certain economic reality. Indeed, financial inclusion raises the issue of the dangers of excessive debt, a phenomenon observed particularly in the context of microfinance.

To initiate virtuous financial inclusion, African economies must develop robust financial systems. Governments can contribute to this phenomenon through public policies aimed, for example, at improving access to official documents, developing communication channels with remote geographical areas, and regulating the emerging banking system.

Sources:

Demirgüç-Kunt, A., Klapper, L., 2012. Measuring Financial Inclusion. The Global Findex Database (Policy Research Working Paper No. 6025). The World Bank, Washington, DC. http://www-wds.worldbank.org/external/default/WDSContentServer/WDSP/IB/2012/04/19/000158349_20120419083611/Rendered/PDF/WPS6025.pdf

Demombynes, Gabriel and Thegeya, Aaron, Kenya’s Mobile Revolution and the Promise of Mobile Savings (March 1, 2012). World Bank Policy Research Working Paper No. 5988. Available at SSRN: https://ssrn.com/abstract=2017401

Nketcha Nana, P.V., Samson, L., 2014. Why are banks in Africa hoarding reserves? An empirical investigation of the precautionary motive. Review of Development Finance 4, 29–37.

Zins, A., Weil, L., 2016. The determinants of financial inclusion in Africa. Review of Development Finance 6, pp. 46-57.

http://www.jeuneafrique.com/mag/421063/economie/mobile-banking-success-story-nommee-m-pesa/

Definitions:

Formal account: holding an account with a financial institution (e.g., a bank, cooperative bank, or microfinance institution).

Formal savings: depositing funds in a bank account or any financial institution such as a cooperative bank or microfinance institution. Conversely, informal savings refers to depositing funds with a tontine or with a person outside the family.

Formal borrowing: borrowing from a bank or financial institution such as a cooperative bank or microfinance institution.

[1]The World Bank’s Global Findex Database covers 37 African countries: Algeria, Angola, Benin, Botswana, Burkina Faso, Burundi, Cameroon, Congo, Côte d’Ivoire, Egypt, Ethiopia, Gabon, Ghana, Guinea, Kenya, Madagascar, Malawi, Mali, Mauritania, Mauritius, Namibia, Niger, Nigeria, Democratic Republic of Congo, Rwanda, Senegal, Sierra Leone, Somalia, Sudan, Tanzania, Chad, Togo, Tunisia, Uganda, Zambia, and Zimbabwe.