Abstract:

- The US trade policy, which has been aggressive since Donald Trump’s election, is causing tensions between the major economic powers.

- Not all of the justifications for this trade policy are « far-fetched »: US manufacturing jobs have suffered from globalization, particularly since China’s arrival on the international markets.

- But there are many inconsistencies, and the United States’ « go-it-alone » policy is jeopardizing the global economic balance, of which the United States is the cornerstone.

Economic news in recent months has been dominated by the implementation of US President Donald Trump’s first protectionist measures and the reaction of partner economies, including additional tariffs, exemptions, and retaliatory measures. This article seeks to untangle the valid and invalid arguments that would justify the increase in US trade barriers, particularly against China, and highlights the economic stakes of this potential « trade war. »

Since the interwar period, economic crises have often been marked by an increase in trade barriers, and the crisis of 2007-2008 was no exception. However, to the surprise of many, the protectionist response was weaker than expected, highlighting the success of the World Trade Organization (WTO). The US presidential campaign and the recent election of Donald Trump as President of the United States have nevertheless kept economic protectionism at the forefront of international debates. With monetary policies on the verge of normalizing, Trump has embarked on a trade policy that is almost as aggressive as the one he announced during his campaign.

Three days after officially becoming president of the United States, he announced the withdrawal of the United States from the Trans-Pacific Partnership[1]. In January 2018, he also imposed additional tariffs on solar panels and washing machines. This protectionist momentum was reinforced in March 2018 with the imposition of additional tariffs on steel (25%) and aluminum (10%) imports.

A look back at five months of trade tensions

This protectionist drive came as a real shock. The United States’ two largest trading partners, Canada and Mexico, were temporarily exempted from these tariff increases while the North American Free Trade Agreement (NAFTA) was being renegotiated. The European Union responded by threatening to tax American products (bourbon and Harley-Davidson motorcycles), which also earned it a reprieve.

However, a real escalation took place with the People’s Republic of China, which declared that it could devalue its currency to protect itself from tariff increases on its products exported to the United States. At the beginning of April, the Chinese Minister of Commerce also imposed tariffs ranging from 15 to 25% on more than a hundred American products. The US Trade Representative responded by publishing a list of Chinese products « to be taxed. » China retaliated the next day by imposing a 25% tariff on around 100 products, including soybeans, which are the leading US agricultural export to China. After talks between Chinese and US delegations, a truce was signed on May 19, 2018, ending the first episode of trade war since the interwar period. However, it does not seem to end there, as on June1, 2018, tariff exemptions for Canada, Mexico, and the European Union came to an end.

Until the beginning of the year, most politicians and economists dismissed the possibility of implementing a trade policy as aggressive as the one announced by Donald Trump during his campaign. How can we explain this protectionist momentum on the part of the United States, at a time when the effects of the crisis seem to be disappearing?

Protectionism, a pillar of the « America first » policy (Donald Trump, 2016)

Trump’s rhetoric is based, among other things, on reducing the US trade deficit, which stands at over $500 billion, making it the largest in the world. By focusing much of his attention on this goal, many have claimed that Trump is a mercantilist, pursuing an aggressive economic policy aimed at accumulating the largest possible trade surplus. But the US desire to reduce the trade deficit is not based on this desire for accumulation. Trump’s protectionist policy stems from his belief that this deficit reflects the economic dysfunctions and injustices suffered by the United States in today’s globalized world. In his view, reducing the trade deficit means protecting the US economy from unfair trading partners.

Donald Trump’s campaign was based on this rhetoric of protecting the US economy, and more specifically protecting American jobs, as evidenced by slogans such as « Make America Great Again » and « America First. » Legally, these tariff increases are permitted under the Trade Expansion Act (Section 232) of 1962, which allows the US president to impose tariffs on a product if its importation jeopardizes national security.« National security » can be understood to mean the economic health of the country: Donald Trump has thus announced a law to end offshoring, in line with his contract with the American voter[4].

In theory, increasing tariffs allows a country to protect its companies from foreign competition: by raising the price of imported products, tariffs are supposed to divert domestic consumption towards domestic goods, thereby boosting the production of local companies. The resulting economic recovery should benefit domestic employment, as domestic companies, which are making more profits, no longer need to resort to layoffs and offshoring.

Very early on, Donald Trump made it very clear that he intended to target economies that were gaining « unfair » trade advantages and which, in his view, were threatening the US economy. This terminology comes from articles of the World Trade Organization (WTO) and the International Monetary Fund (IMF), according to which one country can defend itself against another if the latter uses unconventional policies to gain a trade advantage. Among these policies, currency manipulation was targeted: by intervening in the foreign exchange market, a central bank can depreciate its currency (sometimes to the point of undervaluing it), which improves its price competitiveness. Indeed, depreciation lowers the price of exported products in foreign currency, thereby increasing the volume of exports.

The issue of currency overvaluation or undervaluation had already been addressed during Barack Obama’s presidency: twenty-three senators wrote to the President asking for a currency clause to be included in the Trans-Pacific Partnership, whereby evidence of currency manipulation would allow signatory countries to increase their customs duties. Under the guise of this clause, it was China that was targeted, and still is today. But why this American obsession with China?

The « China shock »

For several decades, China has been accused of manipulating its currency, i.e., maintaining an artificially low exchange rate through intervention in the foreign exchange market. Its detractors explained that this was why China was gaining so much market share, thanks to its low-priced products, whose export was facilitated by a weak currency.

Then China joined the WTO (2001) and began a phase of economic liberalization. Starting in 2005, it indexed the value of its currency to a basket of five other currencies (the US dollar, the euro, the pound sterling, the yen, and the Hong Kong dollar). The renminbi gradually appreciated, silencing criticism of its exchange rate, even though the exchange rate regime remains administered. This explains why the US Congress, which is responsible for determining which countries could be classified as manipulators, has never designated anyone.

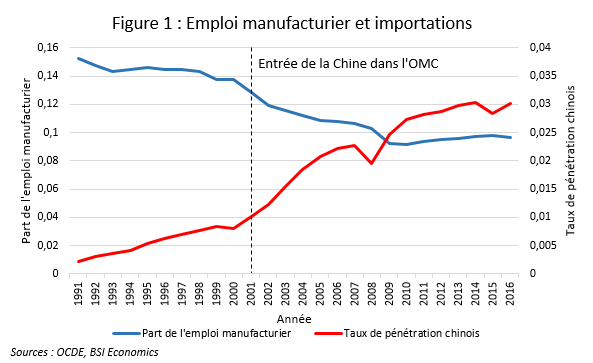

However, while the first pillar of Donald Trump’s protectionist rhetoric has fallen by the wayside, the second remains intact. China’s sudden economic development and transition to a market economy have not been without repercussions for developed economies. This is what economists have called the « China shock »[6]: China’s entry into economic globalization in 2001 profoundly affected advanced economies. From the US perspective, the sudden increase in the share of Chinese products in US imports (known as the penetration rate) coincided with a decline in the share of manufacturing employment in the US, as shown in Figure 1. Several economists have shown that the massive influx of Chinese products onto the market has led to increased unemployment, a decline in employment rates, and lower wages in sectors competing with these same products in the United States: consumers have substituted Chinese products for American products, thereby depressing the manufacturing sector.

It was with this in mind that an agreement was reached between the United States and China: the latter committed to increasing its imports of American energy and agricultural products in exchange for a reduction in American customs duties. This declaration of intent makes perfect sense when we consider that the trade deficit between the two countries stands at nearly $375 billion. Similarly, Brazil, Argentina, Australia, and South Korea have had their exemptions renewed after agreeing to reduce their exports of steel and aluminum to the United States. These latest developments once again underscore Trump’s determination to reduce the US trade deficit at any cost, brandishing the threat of protectionism without necessarily following through on it.

« Trade wars are good, and easy to win » (Donald Trump, March 2018)

However, Donald Trump’s trade policy suffers from several inconsistencies when compared with his rhetoric. While the impact of the « China shock » is evident, US employment appears to be doing well: in December 2017, the US unemployment rate was 4.1%, and only 3.3% in the manufacturing sector. The argument of protecting the US economy is therefore far from sufficient to justify this trade policy. In addition, to limit its economy’s exposure to international competition, the US administration is resorting to « safeguard » tariffs, which are applied to all of the United States’ trading partners, unless they are subsequently exempted. However, if we take the example of steel and aluminum, the US has taxed products that come mainly from its economic allies. According to recent figures, Chinese products account for only 2% of the steel and aluminum imported by the US.

Furthermore, while customs barriers can protect industries competing with foreign countries, this does not come without collateral damage. Every protectionist measure has adverse effects on other economic agents: higher consumer prices lead to a decline in the purchasing power of local consumers; higher prices for imported goods also increase production costs for other industries, which may see their profits decline.

This aggressive trade policy also increases economic tensions between the major economic powers. Following the announcement of the tariffs, the reaction of the United States’ trading partners has been very violent. Canada and Mexico, as well as the European Union, have just seen their exemptions come to an end and have warned the US that they will take swift action, even going so far as to refer the matter to the WTO and take legal action against the US. This exchange of threats has reignited fears of a new trade war. The last such war took place between the two world wars, when the crisis of the 1930s and the weakness of the Gold Standard pushed economies to raise tariffs against each other in the hope of protecting their industries from the slump. In addition, some economists are highlighting the possibility of a « currency war »: China’s threat to de-index its currency and devalue it in response to protectionist measures would have a considerable impact on the global economic order. This scenario is certainly unlikely at this stage, as it would run counter to China’s desire and efforts to make the renminbi an international currency.

Finally, the United States recently vetoed the appointment of a new judge to settle disputes at the WTO, raising fears of a deadlock in international economic institutions. This go-it-alone policy is worrying given the role of the United States in the global economy: it is the world’s second-largest exporter and largest importer of all products combined. The impact on the international trade balance is therefore not insignificant. Furthermore, these decisions have an impact on the US currency: the dollar reacts to every protectionist statement made by the US president, which tends to cause it to appreciate. However, this currency is the cornerstone of the international monetary system, which means that Donald Trump’s choices have an impact, to a certain extent, on other economies.

Conclusion

The aggressiveness of US trade policy since the beginning of 2018 has come as a big surprise and has generated new tensions between the major international powers. The argument of « national security » is justified if we take into account the impact of globalization and China’s entry into the global market on the US economy. However, it loses its meaning when the economies affected by additional tariffs are the United States’ main trading partners, and therefore allies. The inconsistencies in Trump’s trade policy make it impossible to rule out the possibility of a new « trade war, » but the threat is very real, and in every negotiation it serves the current US objective: reducing the trade deficit.

[1] The Trans-Pacific Partnership is a multilateral free trade agreement signed in February 2016 by twelve economies in the Americas and Asia.

[2] These exemptions were lifted on June1, 2018.

[3] This section has never been invoked since the creation of the WTO in 1995.

[4] See “End of the Offshoring Act” and “Contract with the American voter.”

[5] See Article XV of the WTO and Article IV of the IMF.

[6] See Autor, Dorn, and Hanson (2013): « The China Syndrome: Local Labor Market Effects of Import Competition in the United States. » For more information, see also http://chinashock.info/

[7] Share of US steel imports: Canada 16%, Brazil 13%, South Korea 10%, Mexico 9%, China 2%. Source: https://atlas.media.mit.edu/en/

[8] For more details, see Sébastien Jean & Ariell Reshef, « Why Trade, and What Would Be the Consequences of Protectionism? », CEPII Policy Brief 2017-18.