Decline in emerging market reserves: Sovereign rates in advanced economies are unlikely to rise (2/2)

Summary:

· The decline in emerging market reserves is expected to have a major upward or downward impact on sovereign rates in advanced economies through two channels: global liquidity and portfolio rebalancing.

· The effect of portfolio rebalancing is not limited to a simple rise in long-term rates. It could take the form of either a curve distortion or an increase in purchases of equities or real estate assets in advanced economies by private investors in emerging markets, with an increase in sovereign debt holdings by domestic banks.

· In addition to the two channels usually considered, the decline in emerging economies’ foreign exchange reserves is significant in that it reflects the slowdown in their growth and the transformation of their economic models. This is likely to have major repercussions on the financial markets of advanced economies.

After reaching nearly USD 8.2 trillion in June 2014, emerging countries’ foreign exchange reserves are currently on a downward trajectory that is likely to be sustained. This trend could have an impact on asset valuations in the financial markets of advanced economies through two channels: the level of global liquidity and portfolio rebalancing.

In a previous article, we presented the determinants of changes in emerging economies’ reserves. We also attempted to show that their decline does not reduce the level of global liquidity as long as emerging market central banks carry out sterilization operations.

In this article, we will examine the impact of the decline in emerging market reserves on asset prices in advanced economies through two channels: (i) portfolio rebalancing and (ii) macroeconomic spillovers.

1- The complex effects of the portfolio rebalancing channel:

At the national level of each advanced economy considered individually, the sale of foreign exchange reserves by emerging market central banks has no impact on the amount of money in circulation but simply leads to a portfolio rebalancing.

Consider the example of the PBOC selling a US Treasury bond. The operation consists of the Chinese central bank selling a foreign currency asset — a T-Bond— to obtain liquidity denominated in that currency—dollars—in order to sell it on the market in exchange for its own currency—the yuan. In our example, the dollars on the PBOC’s balance sheet change hands: they are now held by a Chinese individual or legal entity wishing to invest their assets abroad, or by a non-resident investor who has liquidated their assets in China and would like to invest them in another economy. The total amount of dollars does not change. Moreover, if the private investor who obtained the dollars from the PBOC immediately reinvests them in a T-Bond with the same maturity as the one held by the PBOC, the transaction would be neutral for US rates.

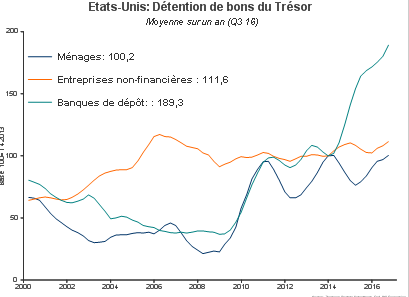

However, the reality is more complex and the composition effect is unlikely to be neutral. Portfolios are likely to be readjusted. In terms of duration, the investment strategies of private agents could differ significantly from those of central banks in emerging countries. For example, the latter have a preference for the short and intermediate segments of the US yield curve, with more than half of their US securities holdings maturing in less than three years and 72% in five years, while 67% of total US debt has a maturity of less than five years. If private agents have a preference for longer maturities, currency sales by central banks could flatten the US curve rather than increase its slope.

In general, private agents may prefer to use dollars to purchase assets other than US Treasury bills. For example, they could deposit their newly acquired dollars with a US bank. The bank would then be likely to reinvest them in T-Bonds. They could also use them to purchase real estate in the United States from a seller who, in turn, would deposit the dollars with the bank, which would then do the same, and so on (Charts 4). Consequently, in all these cases, the decline in emerging countries’ foreign exchange reserves should, through the sale of sovereign securities held by their central banks and ceteris paribus, cause a distortion of sovereign debt curves and not necessarily an increase in long-term rates.

Chart 1

Sources: National Association of Realtors, BSI Economics

Chart 2

Furthermore, private agents are likely to have a greater appetite for equities than central banks. Through this channel, the redistribution of official foreign exchange reserves to the private sector should have two effects:

1) It should support stock prices in advanced economies.

2) On the other hand, by increasing the supply of financing for private companies, the rise in mergers and acquisitions financed by emerging market reserves could reduce the required return on capital—at the risk of creating a bubble if investors no longer exercise their role of oversight and discipline—and, by extension, the natural interest rate in advanced economies.

In fact, the share of emerging economies in cross-border equity investments rose from 5% in 2000 to 11% in 2011, and the share of US equities held by emerging economies rose from 2% in 2002 to 9% in 2014 (Karolyi, et. al 2015). Furthermore, according to UNCTAD data, emerging markets accounted for more than a third of outward FDI in 2010-2015, more than double their share in the first decade of the millennium.

In summary, the decline in emerging market reserves is likely to have an impact on asset prices in advanced economies. However, these effects, which are channeled through portfolio rebalancing, are unlikely to be limited to a simple rise in long-term interest rates. In reality, they are likely to be much more complex, leading in particular to a distortion of yield curves and a possible rise in the prices of risky assets.

2- Emerging countries, a source of growing macroeconomic contagion:

Beyond the channels of global liquidity and portfolio rebalancing, the decline in emerging market reserves deserves particular attention, not only in itself but above all because it is a symptom of a profound transformation of the global economy and its financing methods. This trend is, first and foremost, a sign of less undervaluation of emerging market currencies and, conversely and all other things being equal, less overvaluation of advanced economy currencies. This should benefit growth and inflation in the latter and facilitate the recovery of long-term rates.

Secondly, the decline in reserves also reflects the slowdown in emerging market growth, which is likely to have two effects:

1-This deceleration is contributing to a sustained decline in commodity prices: until very recently, with its rapid growth, China consumed more than half of global iron production and half of global aluminum and copper production (IMF 2015). The moderation in commodity prices should contribute to moderating inflation in advanced economies and therefore weigh on long-term rates.

2-The slowdown in growth in emerging economies is likely to have a greater impact than in the past on advanced economies due to their greater integration into the global economy and financial system. For example, a one percentage point slowdown in Chinese growth had no significant impact on US growth in the early 2000s. In 2015, the impact is estimated at around 0.2 percentage points (Chuik and Hinojosa 2016). Similarly, a decline in growth in the BRICS countries is likely to reduce global growth by 0.4 percentage points over two years (Huidrom et al. 2016). The deterioration in growth prospects in emerging markets is therefore likely to weigh on long-term rates in advanced economies, especially as emerging markets are exerting a growing influence on global asset prices. Indeed, shocks to asset prices in emerging countries now account for one-third of the variance in stock prices and exchange rates in advanced economies due to their increased financial integration (IMF 2016). Emerging economies could therefore be a source of significant volatility in the event of major economic difficulties or market mistrust, for example with regard to countries suffering from a deep current account deficit or insufficient reserves relative to short-term external debt.

Conclusion

The decline in emerging market reserves is likely to lead to portfolio rebalancing effects that are much more complex and nuanced than a simple rise in long-term rates on the sovereign debt markets of advanced economies. It is also symptomatic of a profound transformation in emerging economies, which is likely to generate significant and potentially contradictory spillovers on financial markets in advanced economies. As a result, central bankers in these economies are likely to give greater weight than in the past to developments in emerging countries in their response.

Bibliography

Aerzki, Rabah and Matsumoto, Akito, A “New Normal” for the Oil Market, IMF, October 2016

Bernanke, Ben S., The Global Saving Glut and the U.S. Current Account Deficit, speech given at the Federal Reserve Bank of Saint Louis, Homer Jones Lecture, Board of Governors of the Federal Reserve System, April 2005

Brainard, Lael, What Happened to the Great Divergence?, speech given at the U.S. Monetary Policy Forum, Board of Governors of the Federal Reserve System, September 2016

Brainard, Lael, The « New Normal » and What It Means for Monetary Policy, speech given at the Chicago Council on Global Affairs, Board of Governors of the Federal Reserve System, September 2016

Caballero, Ricardo J., Farhi, Emmanuel, and Grouinchas, Pierre-Oliver, Safe Asset Scarcity and Aggregate Demand, American Economic Review: Papers and Proceedings 2016, 106(5): 513–518

Chuik, Alexander, and Hinojosa, Arthur, Impact of Chinese Slowdown on U.S. No Longer Negligible, Economic Letter, Federal Reserve Board of Dallas, vol. 11, no. 5, May 2016

Clark, John, Converse, Nathan Coulibaly, Brahima and Kamin, Steve, Emerging Market Capital Flows and US Monetary Policy, International Finance Discussion Paper Note, Federal Reserve Board, October 2016

Ferrucci, Gianluidi and Miralles, Cesar, Saving Behaviour and Global Imbalances: The Role of Emerging Market Economies, ECB Working Paper Series No. 842, December 2007

Gelos, Gaston and Surti, Jay,The Growing Importance of Financial Spillovers from Emerging Market Economies, Global Financial Stability Report, IMF, April 2016

Greenspan, Allan, Federal Reserve Board’s semiannual Monetary Policy Report to the Congress, Board of Governors of the Federal Reserve System, February 2005

Huidrom, Raju, Kose, M Ayhan and Ohnsorge Franziska, Painful spillovers from slowing BRICS growth, Vox EU, February 2016

Karolyi, George Ng, David, and Prasad, Eswar The coming wave: Where emerging market investors will put their money, NBER Working Paper No. 21661, October 2015

Ma, Guonan and Yi, Wang, China’s High Saving Rate: Myth and Reality, BIS Working Papers, June 2010

Pescatori, Andrea and Furceri David, Perspectives on Global Real Interest Rates, World Economic Outlook, IMF, April 2014

Prasad, Eswar S., Rebalancing Growth In Asia, NBER Working Paper 15169, July 2009

Yellen, Janet, The Outlook, Uncertainty and Monetary Policy, speech given at the Economic Club of New York, Board of Governors of the Federal Reserve System, March 2016