Summary:

– The Australian agricultural sector has historically faced a shortage of labor, leading to the development of huge, high-yield farms.

– The downward spiral of falling prices, declining yields, and ever-increasing investments is reducing the profitability of a sector that receives very little subsidy in Australia, unlike in France.

– The climate crisis in Australia is further weakening the sector, with over-indebted farms forced into bankruptcy.

– The farmer-peasant model is giving way to that of the multi-skilled farmer-entrepreneur faced with multiple risks.

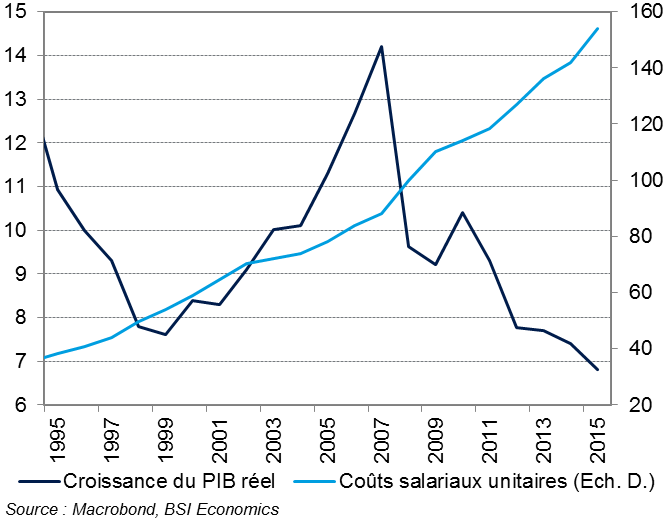

The agricultural sector in France is in crisis, caught between rising investment and falling profitability. This column provides an overview of the difficulties faced by another major agricultural nation, Australia, to highlight some of the challenges facing the agricultural sector. The traditional farmer model is giving way to that of the agricultural entrepreneur, who is both an agricultural engineer and a venture capitalist.

The added value of the Australian agricultural sector was €22 billion in 2013, compared with €32 billion in France, or 1% of global production.1 This is a great success for a productivity-focused, export-oriented agricultural sector.

The Food and Agriculture Organization of the United Nations (FAO) predicts that by2050, global food production will need to increase by 70% to meet the needs of nearly 10 billion people. This is the main challenge facing the agricultural world today. Agriculture should therefore be a booming sector. However, in Australia, the agricultural sector is under pressure and facing a triple crisis: employment, the productivist system, and climate change.

Employment crisis: farms are becoming gigantic

In 2011, the Australian agricultural sector employed nearly 320,000 people on 135,000 farms, or 1.7% of the total population, compared to 960,000 people in France spread across 515,000 farms. However, the Australian agricultural sector has had to contend with a labor shortage that has hampered its development.

-

On the one hand, Australia’s population density is historically very low, with an average of 3 people per square kilometer compared to 121 in France.

-

On the other hand, skilled workers are not attracted to agriculture and are more drawn to the mining sector, which offers better living conditions, despite the crisis currently affecting the mining industry.

-

Unskilled seasonal workers are mainly young people under the age of 31 who have obtained a « working holiday » visa (165,000 visas in 2013). In order to stay in Australia for more than a year on this visa, it is essential to work for at least three months as a seasonal worker, mainly in agricultural jobs.

Basic economic principles therefore suggest an increase in capital intensity, i.e., higher investment in infrastructure and production tools in order to substitute capital for skilled labor, which is too scarce and therefore too expensive.

As a result, the average size of an Australian farm is 2,950 hectares, all types of production combined, compared to 55 hectares in France. This has led to an inexorable decline in the number of farmers, which fell by 21% between 1996 and 2011.

Crisis of the productivist model, between falling yields and rising investment

In 2013, Australian agricultural exports accounted for nearly 60% of its total production, with a value of €27 billion, or 2.3% of GDP. In France, agricultural exports represent €60 billion, or 2.1% of GDP. Markets and prices are therefore largely international, with China being Australia’s largest partner, accounting for 22% of agricultural exports. The majority of Australian farms are livestock farms (48%), but there are also cereal farms (24%) and farms combining both (20%).3

Diversification of Australian and French agricultural crops

In the wake of falling commodity prices against the backdrop of the Chinese growth crisis, market opportunities have become uncertain with volatile agricultural prices. The DJCI indices for wheat andlivestock prices4 have fallen by 50% and 25% respectively since the end of 2005.

Changes in the Dow Jones Commodity indices for wheat and livestock

Direct aid: 2% of Australian farmers’ gross income compared with 18% in Europe

Faced with uncertain yields, Australian farmers receive very little subsidy. Direct aid to farmers represents on average only 2% of Australian farmers’ gross income, compared with 18% in Europe. Total agricultural aid represents 0.1% of GDP in Australia, compared with 0.7% in Europe. The future of Australian agriculture therefore depends on increasing productivity to generate sufficient margins.

Support for agricultural producers in Australia and the European Union

To be profitable, these large farms must be at the cutting edge of technology, which requires significant investment and therefore rationalization of production. However, the agricultural sector is directly affected by the law of diminishing returns. For example, the use of fertilizers only increases the production of a field for a limited time, and increasingly powerful and expensive fertilizers are needed to prevent excessive erosion of yields after a few years. This makes it necessary to invest in high-precision tools to control and adjust fertilizer quantities in order to limit costs. But in order to compile statistics cross-referencing production and the amount of fertilizer required per square meter, skilled workers are needed who are capable of mastering complex tools… including statistics!

As a result, the spiral of increasing farm size, rising investment, and declining yields is forcing Australian farmers into ever-greater debt and putting pressure on profits. While this is an inexorable trend, it is turning farmers into venture capitalists.

Climate change further weakens the economic equation

While climatic hazards have always existed in a country with a predominantly hot and dry climate, climate change, which reduces the intensity and duration of rainfall, is undermining the economic equation for some farms. Small unforeseen events can now more easily lead to situations of excessive debt: the amount of debt incurred for new investments may exceed the value of the farm. This has led to an increase in the number of farms being seized over the past year, as farmers are no longer able to repay their loans with reduced incomes due to drought.

Conclusion

The farmer-peasant model we know is gradually disappearing, in Australia as in France, for various reasons, but with one thing in common: the physical work of the farmer is giving way to the office work of the farm manager, a true entrepreneur with multiple skills. The increase in demand for agricultural products tends to make this transformation inevitable.

But can this headlong rush continue? It seems that in Australia, without direct subsidies, only farmers who prove to be shrewd investors will be able to stay in the market.

But if the market proves to be more fragmented than anticipated, with some end consumers demanding higher quality, less productivity-focused production models (organic farming, short supply chains, etc.) may develop without necessarily competing directly with large farms. The problem facing the agricultural world may therefore be this: choosing between investing to grow or investing to downsize. One option positions itself on global markets, the other on more upmarket markets. But, in the end, 10 billion human beings will need to be fed.

Appendix: Key statistics on agriculture in France versus Australia

1Value added corresponds to agricultural sector production minus the value of intermediate inputs used in production. Figures from the United Nations Statistics Division include the value added from forestry, hunting, fishing, crops, and animal production.

2 Agricultural production projections must meet « the food needs of all people by ensuring that everyone has physical, social, and economic access to sufficient, safe, and nutritious food of their choice, enabling them to lead an active and healthy life » (United Nations, FAO, World Summit on Food Security Declaration, 2009).

3 Source: Australian Bureau of Statistics (2011).

4 The Dow Jones Commodity Index All Cattle Total Return reflects the price of cattle and feeder cattle via futures contracts. The Dow Jones Commodity Index All Wheat Total Return reflects the price of different types of wheat on the Chicago and Kansas markets via futures contracts.