Usefulness of the article: This article provides an update on the situation in Turkey, focusing on the latest economic developments, Turkish financial markets, currency risk, and refinancing risk.

Summary:

- After ten years of strong growth, fueled by credit and boosted by the massive influx of foreign capital seeking returns, the miracle is over and Turkey has sunk into a fourfold crisis: financial, economic, political, and geopolitical.

- Turkey is a victim of its dependence on external financing, making it vulnerable to foreign capital outflows.

- This crisis is reminiscent of the inflationary debt crises in Mexico (1994-1995), Thailand (1996-1998), South Korea (1997-1998), Colombia (2001-2001), Turkey (2000-2001), and Argentina (2001-2002).

- All indicators are flashing red: massive depreciation of the Turkish lira, high inflation, falling Turkish bond and stock markets (in real terms), worrying signals on CDS, falling consumer spending and soaring unemployment. The contraction in Turkish GDP could be greater than expected in 2019 (around -2.5% according to IMF forecasts);

- The Turkish central bank’s management of foreign exchange reserves and the low level of these reserves raise questions, to the extent that the central bank could allow the lira to find its true equilibrium level (leading to further depreciation).

- However, the refinancing risk, which was significant in the banking sector in Q4 2018 and Q1 2019, seems to have been averted for the time being. The government will face refinancing risk in Q1 2020, giving it time to implement the first structural reforms.

Turkey has been severely affected by a financial crisis, symbolized by the sharp depreciation of its currency, the Turkish lira (TRY) (-28.7% against the USD and -25.1% against the EUR in 2018), the fall in the share prices of the country’s main public companies (in foreign currencies), and, above all, the surge in Turkish bond yields and credit default swaps (CDS)[1]. Added to this are an economic crisis (Turkey entered recession inthe fourth quarter of 2018) and a crisis of confidence (private consumption and investment are in sharp decline). Furthermore, Turkey shares its borders with Syria and Iraq to the southeast, two countries that have been severely affected by wars in recent years and whose refugees now number in the millions in Turkey.

This crisis is reminiscent of the inflationary debt crises in Mexico (1994-1995), Thailand (1996-1998), South Korea (1997-1998), Colombia and Turkey (2000-2001), and Argentina (2001-2002), whose economies were also heavily dependent on external financing (between 25% and 60% of GDP) and which ultimately had to call on the International Monetary Fund (IMF) for help in restructuring and containing the crisis (Dalio, 2018).

The aim of this note is therefore to take stock of the situation in Turkey six months after the initial sharp depreciation of the Turkish lira, focusing on the latest economic and financial developments, as well as the exchange rate risk and refinancing risk for companies, banks, and the Turkish government.

1. Overview of the Turkish economic situation

The « Turkish economic miracle, » characterized by high real GDP growth and relatively stable inflation (although relatively high at 7.9% between 2010 and 2016), was made possible by the wave of liberalization that began in the early 2000s (following an initial wave of liberalization launched in the 1980s). After ten years of strong growth, fueled by credit and boosted by the massive influx of foreign capital seeking returns (notably due to the highly accommodative policies of central banks around the world following the 2008 financial crisis), Turkish growth appears to have come to a screeching halt. Expansion has turned into contraction, and there are signs that the storm may not be over yet. This crisis takes us back to the crises of 1993-1994 (12% contraction in Turkish GDP) and 2000-2001 (10% contraction in Turkish GDP) (Dalio, 2018).

1.1 The Turkish lira is experiencing exponential depreciation

Between 2002 and 2013, the exchange rate of the Turkish lira (TRY) against the dollar (USD) and the euro (EUR) was relatively stable, with one dollar trading at an average of 1.5 Turkish lira and one euro trading at an average of 2 Turkish lira over the same period. From 2013 onwards, the depreciation of the Turkish lira became apparent (see chart below), losing more than 75% of its value against the dollar and the euro respectively in just five years, with the depreciation process accelerating sharply from July 2016 and the failed coup. The Turkish lira has thus experienced exponential depreciation since 2013, and there is no indication at this stage that the depreciation process is over.

This depreciation has effectively led to an increase in (1) the cost of imports (particularly raw materials, especially agricultural products) and (2) the foreign currency debt of Turkish companies and banks.

1.2 Turkey is losing control of inflation

Between 2004 and 2018, Turkey managed to keep the annual inflation rate below 12% (although the inflation target is 5% with a fluctuation band of +/- 2%). This relative stability in inflation (compared to the long period of disinflation that Turkey experienced in the 1990s and a peak inflation rate of 130% in 1994) was one of the key factors in Turkey’s economic expansion over the last decade. However, the loss of control over inflation in 2018 (exit from the green rectangle on the chart below) and the delayed reaction of the Turkish Central Bank (TCB), which finally raised its key rate to 24% in September 2018, despite numerous attempts by the government to influence this decision, are weighing on the Turkish economy.

The Turkish central bank was slow to react, allowing inflation to reach a level that is difficult to reconcile with a soft landing for the Turkish economy. The central bank is now obliged to maintain a high key rate, above the inflation rate, in order to regain control of inflation, at the risk of further stifling the country’s economy. Otherwise, inflation could continue to soar, prompting Turks themselves to continue exchanging their lira for foreign currencies and further damaging the Turkish lira.

For the time being, the central bank seems to be managing, as best it can, to maintain its independence from the state, and only by sticking to this orthodox policy can inflation be brought down (≤ 12% if we look at the inflation history of the last fifteen years; ≤5% if we refer to the target announced by the Turkish central bank).

For its part, at the end of December the government announced measures aimed at restoring some purchasing power to the Turkish population, such as a 10% discount on households’ electricity bills, a 10% discount for households and businesses on their natural gas bills, VAT exemption on the purchase of equipment and materials for businesses, and a 26% increase in the minimum wage. Other tax cuts on consumer products (particularly food products), voted in 2018, have been maintained.

1.3 Consumer spending is in free fall

Private consumption accounts for around 60% of Turkey’s GDP, but consumer confidence appears to be particularly low and consumer spending is in free fall. Never in the last 20 years has consumer spending contracted so sharply in Turkey, which is likely to have a significant impact on Turkish GDP in the coming quarters, with the contraction likely to be much greater than expected. For the moment, the median forecast of 43 economists surveyed by Reuters predicts a contraction in Turkish GDP of only 0.3% in 2019 (while the Erdogan government still anticipates GDP growth of 2.3%). The IMF, for its part, anticipates a contraction in Turkish GDP of 2.5% in 2019. By way of comparison, Turkish GDP contracted by 6% and 4.7% respectively during the previous crises of 2001 (banking crisis) and 2009 (financial crisis).

1.4 Unemployment rate at an all-time high

The unemployment rate jumped sharply in February 2019, rising from 13.5% to 14.7% of the working population, representing an additional 366,000 unemployed (the unemployment rate was still only 9.6% in April 2018). More worryingly, the unemployment rate for 15-24 year olds has now reached 26.7%, the highest unemployment rate ever recorded for this age group. In total, the number of unemployed people has increased by around one million in just one year. Unemployment now affects 4.7 million people in Turkey, the highest since 2009.

2. Update on Turkish financial markets

Given the many uncertainties surrounding Turkey, foreign capital is flowing out of the country, with international investors preferring to reinvest their capital in emerging countries considered more stable or repatriate it to the United States, which has been experiencing stock market euphoria since the US Federal Reserve (Fed) changed course and its chairman, Jerome Powell, made new ultra-accommodative comments.

2.1 Bond market, CDS and sovereign risk

The Turkish 10-year sovereign bond moved in line with German and French bonds until 2013 due to low public debt (29% of GDP in 2018) and effective management of public accounts. From 2013 onwards, however, the spread between Turkish bond yields on the one hand and German and French bond yields on the other began to widen, and has continued to increase ever since, signaling a loss of investor confidence in Turkey. This surge in Turkish sovereign rates (the 10-year rate stood at 19% in May 2019, compared with 12% a year earlier) is likely to automatically lead to an increase in government debt servicing costs, a widening of the public deficit, and an increase in public debt. It should also be noted that of the three major rating agencies, which currently classify Turkish sovereign debt as « speculative, » two have recently maintained their negative outlook on Turkey, leaving open the possibility of a further downgrade of Turkish debt in the future.

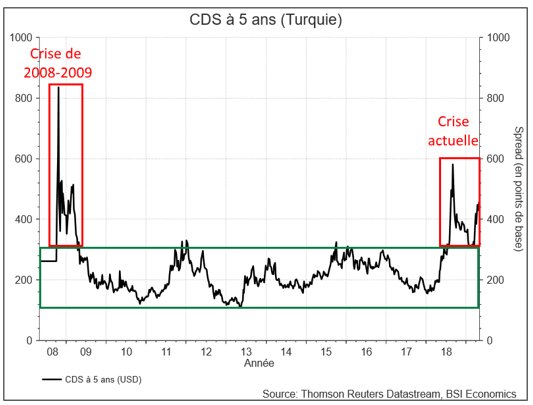

The five-year Turkish CDS, meanwhile, has emerged from a long period of hibernation (2009-2018), returning to levels not seen since 2008-2009 (see chart below). Despite a decline in the CDS premium between Q4 2018 and Q1 2019, raising hopes of a return to normal and a re-entry into the green rectangle (spread ≤320 bps), CDS rose sharply again at the end of March 2019, casting doubt on the markets’ perception of sovereign risk.

2.2 Equity market

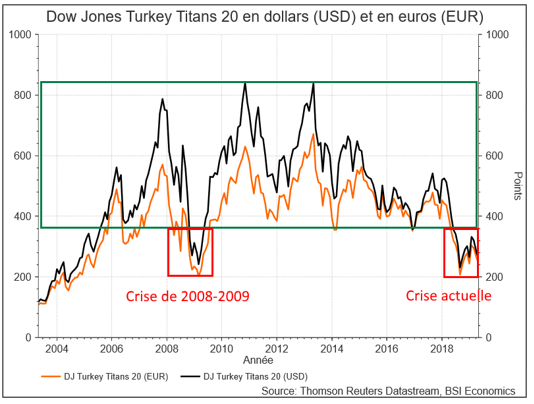

The Turkish equity market (in real terms) is also under pressure. The international benchmark index, the Dow Jones Turkey Titans 20, which includes the 20 most liquid stocks on the Istanbul Stock Exchange, has lost more than 75% of its market capitalization (in both euros and dollars) since its highs in 2013. As we can see in the chart below, the index has fallen back to both its 2004 levels (roughly corresponding to the start of the last phase of expansion in the Turkish economy) and its 2008-2009 levels (corresponding to the last major financial crisis). As with the spectacular rise in interest rates on the Turkish bond market, this fall in the stock index symbolizes investor (particularly foreign investor) mistrust of Turkey. Here again, the Turkish stock market’s decline of more than 20% in the last quarter, despite a rebound of more than 50% that began in Q4 2018, also casts doubt on Turkey’s ability to recover this year.

The question is therefore whether the low point reached in August 2018 (around 200 points) can be maintained in the coming months. If not, a return to square one (the Dow Jones Turkey Titans 20 index was launched in 2004 with a base value of 100 points) is conceivable.

3. The currency crisis could worsen, but the risk of refinancing seems to have been averted

The more the Turkish lira depreciates, the more difficult it becomes for Turkish banks and companies to repay their foreign currency debts, which could lead to bankruptcies. As a result, all eyes are on the central bank, which is working to preserve the value of the national currency on the foreign exchange market, even if it means resorting to unorthodox practices.

3.1 Currency risk

Currency risk refers to the uncertainty of the exchange rate of one currency (in this case, the lira) against another (the dollar or the euro, for example). This currency risk is perceived negatively, both by investors (who will demand a higher risk premium in order to be compensated for the risk incurred, which automatically lowers the price of Turkish assets: stocks, bonds, real estate) and by businesses and households (who will exchange their lira mainly for dollars, but also for euros or any other reserve currency).

In order to slow down the conversion of Turkish lira into foreign currencies, both within the Turkish banking system and on the foreign exchange market, the central bank has activated the two levers generally used during currency crises, namely:

- The use of the key interest rate (an increase in this rate increases the remuneration of Turkish lira holders and makes it more difficult to take speculative positions against the lira);

- The use of foreign exchange reserves (to offset excess supply by artificially increasing demand for lira on the foreign exchange market and thus maintain the value of the Turkish lira).

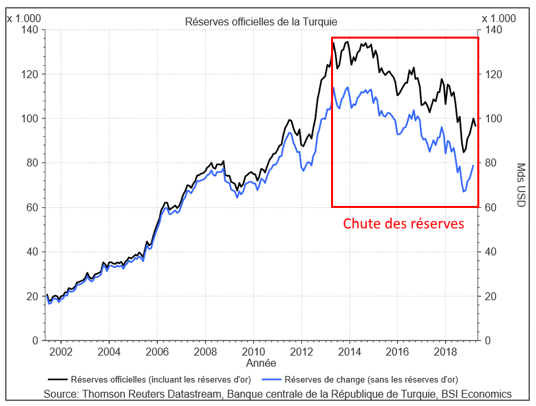

Despite the use of these two levers, the decline in foreign exchange reserves( both gross and net) is a cause for concern. Official foreign exchange reserves (as defined by the IMF) have fallen sharply in recent years, from USD 136 billion at the end of 2013 to USD 84 billion at the end of 2018, a drop of nearly 40%. Foreign exchange reserves (excluding gold reserves) fell from USD 107 billion to USD 73 billion over the same period, a drop of nearly 32% over five years. According to the Turkish central bank, which highlights the recent increase in the country’s foreign exchange reserves (+3.5% growth in foreign exchange reserves in Q1 2019, with the country generating a current account surplus for two quarters, which has helped to ease the pressure on its reserves), these reserves are still sufficient to defend the lira on the foreign exchange market.

However, on closer inspection, it appears that net foreign exchange reserves (which can actually be mobilized in the very short term) are extremely low (USD 28 billion at the beginning of April 2019 according to official figures from the Turkish central bank), so much so that the latter could quickly find itself trapped and forced to let the lira find its true equilibrium level, thus opening the door to further depreciation.

This is all the more likely given that Turkey’s foreign exchange reserves are actually overvalued by $12 billion (Pitel and Samson, 2019) due to the use of currency swaps (very short-term loans) (in dollars) with Turkish commercial banks. The aim of this maneuver, used by other emerging countries when their currency is under attack, is to inflate the country’s foreign exchange reserves in the very short term in order to (1) increase the central bank’s firepower on the foreign exchange market and (2) show a higher level of foreign exchange reserves than is actually the case.

As a result, Turkey’s foreign exchange reserves (in net terms) would be only $16 billion, or less than one month’s worth of imports, even though the critical threshold is usually three months’ worth of imports. Furthermore, these reserves would only be enough to last a few days at most in the event of another coordinated speculative attack (the first attack took place last summer). It should be remembered at this point that the central banks of Mexico (1994) and Thailand (1997) also exhausted 100% of their available reserves before allowing their respective currencies to float freely (Dalio, 2018). Similarly, during the Turkish crises of 1993-1994 and 2000-2001, the central bank also used its foreign exchange reserves to cushion the fall of the lira before allowing it to find its true equilibrium level. A return of political uncertainty (linked, for example, to the annulment of the Istanbul municipal election results) or economic uncertainty due to the lack of economic reforms deemed credible by the markets could serve as a catalyst and lead to a second speculative attack, despite the very likely absence of rate hikes in the United States this year.

The credibility of the Turkish central bank, which has already been undermined on several occasions (notably due to its slowness in raising rates and its lack of independence from the government), could suffer from its unorthodox policy, which is precisely what Turkey does not need at the moment.

3.2 Refinancing risk

The currency crisis, which is currently limited, could therefore worsen in the very short term. However, a (re)financing crisis, which could lead Turkey (the state, companies, banks) to default on part of its debt, seems unlikely at this stage. The currency risk mainly affects small businesses, particularly in the construction, transport, and energy sectors. As these businesses do not necessarily have access to foreign currency income, it has been decided that they will no longer be able to borrow in foreign currencies until further notice. In addition, the capacity of the guarantee fund was increased in 2017 to support these companies, and debt restructuring is currently being prioritized in order to avoid bankruptcies.

Most of the private debt is held by Turkish companies that generate foreign currency revenues and/or have access to currency hedging tools, and have done so for many years, thus limiting the risks they face in the short term. As for the banks, which had lent heavily to Turkish households and companies (particularly in the real estate and energy sectors), while financing themselves in the short term in foreign currencies (85% of short-term debt is in foreign currencies), were able to cope with the refinancing risk in both Q4 2018 and Q1 2019, even though the markets were skeptical about this. However, their ability to borrow and refinance their external debt appears to be significantly reduced going forward.

In addition, Finance Minister B. Albayrak has just announced a USD 4.9 billion recapitalization plan for state-owned banks, while encouraging private banks to recapitalize if necessary. It remains to be seen whether investors will be motivated to recapitalize Turkish private banks. And if so, at what price? Finally, as far as the government is concerned, the refinancing risk does not appear to be significant this year, with the next repayment peak in January 2020, which gives it time to implement the first structural reforms.

Finally, it should be noted that the share of non-performing loans, currently at 4.2% (compared to 5.5% at the height of the 2008-2009 crisis), a figure that remains low but has risen sharply in recent months, will be the indicator to watch in order to assess the deterioration in the quality of bank credit in Turkey. This ratio, which exceeded 10% in all countries affected by the 1997-1998 Asian crisis, reaching as high as 50% in Thailand, is a good indicator of the risk to the banking system as a whole.

Conclusion

The currency crisis affecting Turkey may not be over, and further depreciation could occur in the coming weeks. However, the sharp depreciation of the Turkish lira should enable the current account to return to surplus, and Turkish companies could quickly take advantage of the lira’s weakness to regain competitiveness, both regionally and internationally.

However, only a rapid and successful restructuring of the private sector’s short-term debt (an issue on which the IMF could intervene), as well as the implementation of (1) a transparent and reliable orthodox monetary policy by the Turkish central bank and (2) credible economic reforms by the government, can put Turkey on the path to healthy and sustainable growth, ultimately enabling it to exploit its fantastic potential.

References

Ray Dalio, Principles for Navigating Big Debt Crises, Bridgewater, 2018.

Nevzat Devranoglu, “Turkey’s economy to contract in 2019, longer recession ahead,” Reuters, April 12, 2019.

Selcan Hacaoglu and Onur Ant, “Erdogan’s Slog in Cities Underscored by Decade-High Joblessness,” Bloomberg, April 15, 2019.

Junkyu Lee and Peter Rosenkranz, “Non-Performing Loans in Asia: Determinants and Macrofinancial Linkages,” ADB Economics, Working Paper Series, March 2019.

Elise Massicard, “A Decade of AKP Power in Turkey: Towards a Reconfiguration of Governance Modes?” Les Etudes du CERI – No. 205, July 2014.

Laura Pitel and Adam Samson, “Turkey props up reserves with billions of dollars in short-term borrowing,” Financial Times, April 17, 2019.

Ece Toksabay and Ali Kucukgocmen, “Turkey to inject $4.9 billion into state banks in economy reform package,” Reuters, April 10, 2019.

[1]A credit default swap ( CDS) is a form of insurance contract that allows the holder to protect themselves financially against a credit event (default, late payment, or restructuring) occurring on the underlying asset. The price of the CDS corresponds to the spread to be paid in basis points (bp). For example, a CDS with a spread of 500 bps (i.e., 5%) indicates that to insure $1 million, the CDS purchaser will have to pay an annual premium of $50,000. On a 5-year CDS, a spread of 500 bps implies a 25% probability of default (5 years x 5% = 25%).

[2]See Arthur de Moze’s (BSI Economics) note on the subject (https://bit.ly/2VYWNCA)

[3]Istanbul Stock Exchange indices such as the BIST 30 are not good indicators of equity market valuation due to high inflation affecting the Turkish lira, which pushes up Turkish indices in nominal terms while they depreciate in real terms.

[4]The main reserve currencies include the US dollar, the euro, the yen, the pound sterling, the Swiss franc, the yuan, the Canadian dollar, and the Australian dollar.

[5]Foreign exchange reserves represent all foreign currency assets and holdings, as well as gold reserves held by the central bank (https://bit.ly/2iXSfKe).

[6]Turkish banks are said to have lent part of their customers’ dollar deposits to the central bank.

[7]According to the Central Bank, at the end of 2018, 85% of foreign currency debt was held by 2,300 large companies out of 45,000 companies with foreign currency debt. The number of indebted companies (medium-sized or small) is therefore very significant, but their share of foreign currency debt is estimated to be no more than 15%.

[8]Asian Development Bank (ADB).