Usefulness of the article: While many observers agree that the money multiplier is no longer relevant in today’s world, fewer really understand why. This article helps us understand that a central bank can control inflation even when liquidity is abundant. Consequently, even if economic activity were to rebound strongly in the eurozone, there would be no risk of inflation soaring due to abundant bank liquidity.

Summary:

- A frequently cited concern is that, given the abundance of bank liquidity (and therefore excess reserves), once economic activity picks up in the eurozone, money creation and credit could spiral out of control. This reasoning is based on the concept of the « money multiplier. »

- The article explains why the money multiplier was relevant in the monetary environment of the past;

- However, the presence of a rate on excess reserves makes it irrelevant in the current context, rendering the fears in question unfounded.

In the United States and other developed economies, there has been much debate in recent years about a potential surge in inflation once the crisis is over, due to the large amount of bank liquidity (Figure 1). The same debate is likely to arise in the eurozone once economic activity returns to a solid growth path, if the European Central Bank (ECB) leaves the large amount of liquidity in the banking system as it is.

Bank liquidity, total amount

Source: BSI Economics, Central Banks

The link between inflation and bank liquidity is explained by the « money multiplier » or « credit multiplier« theory. Simply put, this theory predicts that a large amount of bank liquidity (the famous liquidity that banks hold at the central bank) will ultimately lead to a surge in credit. During the financial crisis, central banks injected a significant amount of liquidity into the banking system, but credit did not increase dramatically. For some, the explanation was obvious: the credit multiplier was « broken, » mainly because the risk of lending was too high. Now that economic conditions have improved, the credit multiplier could return to its « normal » level, which could lead to an explosion in credit.

The purpose of this article is to explain:

- Why the monetary multiplier model was relevant in the « monetarist » framework that guided the monetary policy of most central banks before the 1990s;

- Why it is no longer relevant today, and more specifically, why since the crisis and the massive injections of bank liquidity, we can no longer rely on the multiplier model, due to the simple presence of a rate on excess reserves[3].

The (overly) simplistic view of the money multiplier

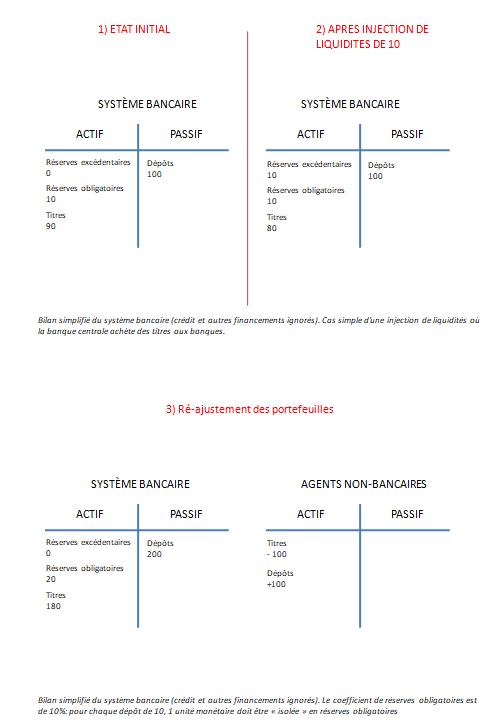

Simply put, the money multiplier tells us the following: as long as the banking system as a whole has sufficient liquidity to meet the reserve requirements[4]set by the central bank, it will seek to « use » its excess liquidity (reserves in excess of reserve requirements), either by purchasing securities from non-bank agents or by granting them credit. In doing so, the banking system will ultimately create new deposits.[5]Since deposits are money, the money supply will ultimately increase. In the graph below, this is what causes us to move from stage 1 to stage 3.

In this simple view, which is often presented, this process of money creation is limited by several forces. First, with each new deposit created, the reserve requirements for the banking system increase. The reason is simply that the amount of reserve requirements is set according to the total deposits of the banking system: when deposits increase, reserve requirements increase. With each new deposit created, the level of excess reserves therefore decreases. Similarly, a second constraint arises from the fact that some depositors will simply withdraw part of their deposits in cash. Thus, if deposits increase, banks can expect that some of the new deposits will be withdrawn by depositors and leave the banking system. This second « leakage » of deposits should therefore also reduce the excess reserve base available after each deposit creation, thus limiting the multiplier process.

Ultimately, these reserve requirements and natural « leakages » of cash deposits are the factors that lead us to believe that the money multiplier is not unlimited but, on the contrary, finite.

Understanding the money multiplier in more detail

The description provided above is based on some important shortcuts. Other factors come into play to ensure that the initial stage of « increased liquidity » leads to the final stage of « increased money supply,« particularly the following factor: excess reserves do not earn interest.

Without interest on excess reserves, with positive interest rates (let’s assume for simplicity that the representative « securities »[8] have a yield of 4%), a drastic increase in reserves will normally encourage banks to make adjustments: the money multiplier mechanism will work. A simple but coherent way of understanding how this mechanism works is as follows: if a bank finds itself with excess reserves earning 0% interest,[9] it will quickly seek to dispose of its reserves by purchasing securities, which pay 4% interest.[10] Having an asset that pays 4% interest rather than one that pays 0% is always preferable: the bank’s profit will be all the greater for it.

If a bank buys securities from another bank, the « hot potato » of unremunerated reserves is passed on to another bank, which will then buy other securities. The « hot potato » is simply passed on, but not cooled down.

If a bank buys securities from non-bank agents, the latter obtain deposits and the bank’s reserve obligations increase: excess reserves decrease.

Ultimately, when interest rates are positive, a simple condition for the « hot potato » of excess reserves to cool down is for the portfolios of banks and non-bank agents to be adjusted. Once banks have acquired enough securities from non-bank agents (creating deposits through these actions), so that excess reserves have become zero, the process of money multiplication ends. For this portfolio adjustment to take place, banks must convince non-bank agents to sell their securities. The price of securities will therefore inevitably have to adjust upwards in the process, and interest rates will have to fall, in order to satisfy the banks’ frenzied demand for securities.

The mechanism described above corresponds to the mechanics of the money multiplier as described in Bernanke (1988), for example. The reasoning is applied to securities, but it could be extended to credit creation. In particular, we can see it this way: with lower interest rates, financing costs will generally fall, including those of banks, which will therefore be able to lend at lower rates while remaining profitable. The initial increase in banks’ balance sheets can also be seen as a simultaneous adjustment in securities and credit in the same spirit as the process described above, as also explained by Bernanke (1988).

This mechanism corresponds to the idea of monetary policy transmission in a « monetarist » framework, where the money supply is targeted.

Why the money multiplier was theoretically relevant before

In a world where the central bank targets the money supply, as was the case before the 1990s in the United States, for example (see Bindseil (2014)), the central bank injects bank liquidity (i.e., reserves) with the aim of increasing the money supply[11]. Stabilizing the growth rate of the money supply is seen as relevant in this context for many reasons: fundamentally, it is seen as ensuring a stable inflation rate over time, based on reasoning that uses the quantity theory of money as a frame of reference[12] (see Bernanke (1988) or Friedman (1970)).

In such a world, the central bank therefore sought to control the money supply, rather than interest rates directly as it does today. By injecting liquidity, since the central bank knows that it is profitable for banks to use excess reserves for other purposes until these excess reserves disappear (via the mechanism described above), the central bank could hope to control the money supply.

Why the money multiplier is no longer relevant in the current context

In addition to reasons related to the monetary policy framework, which could be the subject of a separate article, the money multiplier is no longer relevant in the current context for the simple reason that excess reserves are now remunerated by the central bank. The central bank remunerates excess reserves in order to control interest rates (primarily the interbank market rate), which is the main focus of monetary policy today. For example, the ECB has always operated with a deposit facility, allowing banks to earn interest on their excess reserves at a certain rate (currently negative, but positive in the future, as it used to be before the crisis). The Fed has been paying interest on excess reserves since 2008.

Thus, if the central bank injects a quantity of excess reserves remunerated at 4%, when the rates on securities are 4%, there is no incentive for banks to dispose of their excess reserves. Consequently, the initial multiplier process cannot be triggered. Since financing costs are not reduced, if the demand for credit at the prevailing rate is satisfied, there is no reason for banks to extend credit either. Ultimately, if reserves earn interest and that interest rate is equal to the rate on securities in our example, there is no reason for the money multiplier process to be triggered.[15]

This situation is similar to that currently experienced by the banking system in the euro zone. Liquidity is so abundant that any new injection does not encourage banks to pass on a « hot potato » of excess reserves: they simply agree to hold the excess reserves because they do not consider holding securities to be a more profitable operation: they are indifferent between holding securities or excess reserves at the prevailing rate. The ECB could therefore easily maintain this situation when it raises interest rates, by increasing the rate on excess reserves (to 4% in our example) while maintaining the same volume of liquidity. With a « normalized » economic and monetary situation, the existence of a rate on excess reserves would be sufficient to render any « money multiplier » mechanism irrelevant, despite the large amount of liquidity in the banking system. A corollary to this conclusion is that there would therefore be a very negligible risk of a surge in credit or inflation if the ECB were to keep the same amount of liquidity in the banking system once economic activity had returned to a solid footing: the central bank could simply control activity with a rate on excess reserves.

Conclusion

This article has explained that the existence of a rate on excess reserves (e.g., the deposit facility rate for the ECB) means that, in periods of excess liquidity, the predictions made by the credit multiplier (or money multiplier) theory are not relevant.

Thus, if the ECB decides to raise rates while leaving the current abundant liquidity volume unchanged, the analysis in this article shows that there would be no risk of a surge in credit or inflation due to the very large amount of liquidity.

While the credit multiplier may have had theoretical relevance in a monetary targeting framework, the concept is no longer relevant today for understanding the essence and consequences of current monetary policies.

Bibliography

Ben S. Bernanke, 1988. « Monetary policy transmission: through money or credit?, » Business Review, Federal Reserve Bank of Philadelphia, Nov. issue, pp. 3-11.

Ben S. Bernanke, 2003. « Friedman’s monetary framework: some lessons, » Proceedings, Federal Reserve Bank of Dallas, Oct. issue, pp. 207-214.

Bindseil (2014) Monetary Policy Operations and the Financial System

Claudio Borio & Piti Disyatat, 2010. « Unconventional Monetary Policies: An Appraisal, » Manchester School, University of Manchester, vol. 78(s1), pages 53-89, September.

Frank Decker, Charles Goodhart, 2018. « Credit mechanics: A precursor to the current money supply debate »

Carpenter, Seth & Demiralp, Selva, 2012. « Money, reserves, and the transmission of monetary policy: Does the money multiplier exist? », Journal of Macroeconomics, Elsevier, vol. 34(1), pages 59-75.

Milton Friedman “The Counter-Revolution in Monetary Theory”, IEA Occasional Paper, no. 33.

Raymond E. Lombra, 1992. « Understanding the Remarkable Survival of Multiplier Models of Money Stock Determination, » Eastern Economic Journal, Eastern Economic Association, vol. 18(3), pages 305-314, Summer.

Jakab, Zoltan and Kumhof, Michael, Banks are Not Intermediaries of Loanable Funds – And Why This Matters (May 29, 2015). Bank of England Working Paper No. 529.

[1]It could theoretically do so by choosing to target the EONIA at the level of its deposit facility rate. However, there is currently no indication that it will do so.

[2]The money multiplier is a more general concept than the credit multiplier. In the money multiplier, loans and bonds are perfect substitutes, so the distinction between loans and bonds is irrelevant. In the second concept, all money created can be seen as the result of an increase in credit. The focus on the credit multiplier is relevant insofar as credit and bonds are not perfect substitutes and credit growth has a greater impact on the economy than simply focusing on money creation. In this article, the distinction is irrelevant to the point under discussion: either one wouldultimately lead to moreinflation. The two terms are therefore often used interchangeably here. See Bernanke (1988) for a discussion.

[3]For other criticisms of the money multiplier not fully addressed in this article, see Decker and Goodhart (2018), Carpenter and Demiralp (2012), Zoltan and Kumhof (2015), Bindseil (2015), or Borio and Disyatat (2009).

[4] See this post for an explanation of reserve requirements: http://www.bsi-economics.org/407-reserves-obligatoires-et-gestion-des-liquidites-comment-cela-marche-pour-une-banque-en-zone-euro

[5] See this post for an explanation of how deposits are created by the banking system: http://www.bsi-economics.org/449-le-taux-negatif-de-la-bce-quelques-remarques-pour-dissiper-les-confusions

[6]For a critique of this overly simplistic version of the multiplier, see also Lombra (1992), in addition to the studies cited above. Lombra (1992) explains that the money multiplier is the reduced form of a more complete model, and therefore that there are implied institutional and structural relationships between the two stages explained above. Understanding why the multiplier is stronger or weaker at certain times requires an understanding of these relationships. The monetary multiplier in its pure form is a model that focuses on supply (i.e., only on the behavior of the bank). If we take into account the demand for money (which has no reason to automatically adjust to supply), we can understand why and how other variables implicitly adjust in the multiplier process. The importance of modeling these variables depends on the importance we attach to them: for monetarists, these variables did not have the paramount importance that others attach to them. See Bernanke (1988) on this point.

[7]This was the case in the United States before 2008 (seehttps://fredblog.stlouisfed.org/2018/06/paying-interest-on-excess-reserves/.).

[8]We simplify the reasoning by considering a representative « security, » which can be considered a Treasury bill, for example.

[9]This is what would happen in practice after an open-market operation by the central bank, which would buy assets from banks, sold by the latter with the aim of profiting from the operation, while hoping to reinvest the reserves in more profitable assets afterwards.

[10]In a simple framework where reserves and securities are perfect substitutes, the incentive would exist as long as securities and reserves had different rates. We can reason in this framework here; imperfect substitutability is simply a limit on the size of the multiplier and not a limit on its theoretical relevance.

[11]There are actually several variants. The central bank could control the amount of unborrowed reserves (at the discount window), the amount of excess reserves, or other related variables (see Blindseil (2014) chapter 4 for a discussion). Note that from 1974 (or even 1970 according to others) to 1979, the Fed targeted the Fed Funds rather than a quantity of liquidity. See Blindseil (2014) or Lombra (1992).

[12]For a constant velocity of money, an increase in the money supply is expected to lead to an increase in activity, first in the short term and then to inflation in the long term, as explained in Bernanke (2003), e.g. The reasoning involves an indirect effect on stimulating spending (via lower interest rates) and a direct reasoning of portfolio rebalancing towards durable and semi-durable consumer goods. This monetarist view lost importance when the demand for money became unstable (both due to the creation of close substitutes for money and technological innovations).

[13]In short, central banks today seek to control interest rates, not the money supply. They control interest rates by setting the rate on the interbank market. Setting the rate on the interbank market requires responding to the demand for reserves at prevailing rates. Today, under normal circumstances, the central bank responds passively to the banking system’s demand for reserves, so the multiplier process is fundamentally reversed (which was obvious until 2008).

[14]If it is not, it is because banks were constrained by liquidity. For the argument we are discussing, this particular case is irrelevant: once these constraints become irrelevant, new injections of reserves would have no effect on credit per se.

[15]It may of course be that the rate on reserves is not equal to the rate on securities, or, to be more realistic, it may be that banks have an incentive to take on assets at rates lower than the rate on excess reserves. This is the case if they are not perfect substitutes. But sooner or later (and sooner rather than later in reality), the rate on reserves will become binding due to the mechanism described above: banks will no longer have an interest in purchasing new assets or offering credit at lower rates once interest rates have fallen sufficiently given the level of remuneration on reserves.