Usefulness of the article: In this article, we attempt to provide an overview of the monetary policies of the various Nordic central banks, as well as the underlying determinants of price dynamics in these countries. We then explore the mechanisms and risk channels through which the trajectories of rate hikes could be altered.

Summary :

- Sweden: The recent reversal in real estate prices in an environment of persistently negative repo rates will continue to limit the Riksbank’s room for maneuver.

- Denmark: Pegging to the euro, against a backdrop of monetary policy easing by the European Central Bank (ECB), suggests a status quo for Danish monetary policy despite favorable domestic conditions;

- Norway: Bucking the trend, stronger-than-expected growth and the continued erosion of excess margins are triggering a marked tightening of Norges Bank’s policy;

- Given the domestic risks of household debt, the materialization of a slowdown in global growth will weigh on the pace of monetary normalization by the Danish and Swedish central banks.

Scandinavian economic models are structurally similar. They are based on strong government involvement in the economy and a system combining high living standards and high taxation to ensure strong social redistribution. These economies are very open to international trade and also show strong similarities in terms of fiscal discipline (with budget surpluses since 2016 of ½% to 1% of GDP in Denmark and Sweden, compared with more than 5% of GDP in Norway) and the actions and mandates of their respective central banks, which target inflation of close to 2%[1].

In this context, the scale of the 2009 economic crisis saw the Nordic countries experiment with similar unconventional monetary policies, following in the footsteps of the European Central Bank (ECB), notably through the use of negative key interest rates in Sweden (repo rate) and Denmark (deposit rate). For all countries, however, this decade of ultra-accommodative monetary policies has contributed to the build-up of risks weighing on central bank action, particularly household debt linked to changes in real estate prices. Thus, despite a synchronized recovery in economic activity in the Nordic countries in recent years, the medium-term outlook for Sweden, Denmark, and Norway is diverging, and some central banks are struggling to return to their pre-crisis monetary framework. The Swedish and Danish central banks are suffering the repercussions of an unfavorable external environment, but this has not prevented the Norwegian central bank from normalizing its policy.

1. The balance of risks is broadly similar for the region’s economies

Structural factors such as rising disposable incomes and marked imbalances between housing supply and demand have contributed, in the wake of the sustained easing of Nordic monetary policies since the financial crisis, to the build-up of risks in the respective real estate markets of these countries. This is particularly the case in Sweden and Norway, where prices in early 2019 were more than 50% above their pre-crisis levels (Chart 1, A). The impact of real estate markets on the economic cycle and, in fact, on the conduct of monetary policy is well documented: the sustained easing of global monetary policies means that a growing proportion of the population can access housing. As a result, demand for mortgage loans is increasing, leading to a significant rise in real estate prices and aggregate household debt. This debt poses significant risks to countries’ growth, as it constrains private household consumption, the traditional driver of growth in the Nordic countries.

Furthermore, Denmark and Sweden[2] are even more open to international trade than their European neighbors. The resilience of their economies therefore depends in particular on the strength of their exports in relation to global private consumption and thus on their openness to the world (Graph 1, B). Consequently, sluggish global growth has the potential to translate into a slowdown in Nordic growth.

Figure 1: Risks and characteristics of the Nordic countries

Source: OECD, World Bank, BSI Economics.

2. The Riksbank, bound hand and foot

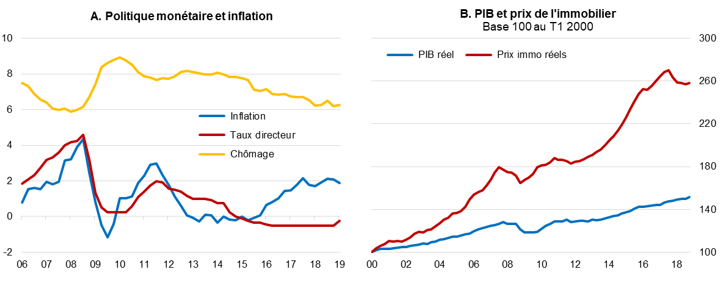

Swedish growth proved solid (2%) and stronger than the eurozone average

(1.2%) in the first quarter of 2019, but it was slowing down, as were its Nordic neighbors (with Denmark at 2.2% after an average of 1.4% in 2018 and Norway at 3.7% compared to an average of 2.5% in 2018), partly reflecting the decline in residential investment in GDP, which is now more than 10% below its peak in Q1 2018. Inflation, which has remained close to its 2% target since early 2017, has recently shown signs of weakness, particularly with the disappearance of the upward effects of energy prices and the slowdown in the labor market, with unemployment struggling to return below its pre-crisis low of 6% (Chart 2, A).

The surge in Swedish real estate prices (Figure 2, B) since the beginning of the century reflects a combination of factors, including:

- A chronic shortage of housing around major urban areas due to geographical and land-use constraints.

- A decade of ultra-accommodative monetary policy, which has depressed borrowing rates and thus made it easier for households to access mortgage credit.

- Favorable tax factors, such as the deductibility of mortgage interest payments from income tax.

The reversal in prices observed since mid-2018, if it continues, would be a cause for concern given the level of aggregate household debt (which currently averages more than 180% of disposable income), especially since three-quarters of outstanding mortgage loans are variable-rate. A rise in interest rates would automatically increase these households’ interest payments and thus weigh on their solvency.

In an environment of low inflationary pressures, unemployment hysteresis[3], doubts about household solvency, and uncertain international developments (impact of a potential manufacturing slowdown in Germany[4] or the escalation of the Sino-American conflict on value chains) and after a 25 bp increase in the repo rate in May 2019, it will become increasingly difficult for the Riksbank to justify a more pronounced tightening of its monetary policy in the medium term. In the minutes of its latest inflation report, the central bank even hints at a postponement of any rate hike until 2020.

Chart 2: Economic and risk indicators in Sweden

Source: Statistics Sweden, Riksbank, OECD, and BSI Economics.

3. Status quo in Denmark despite some favorable conditions

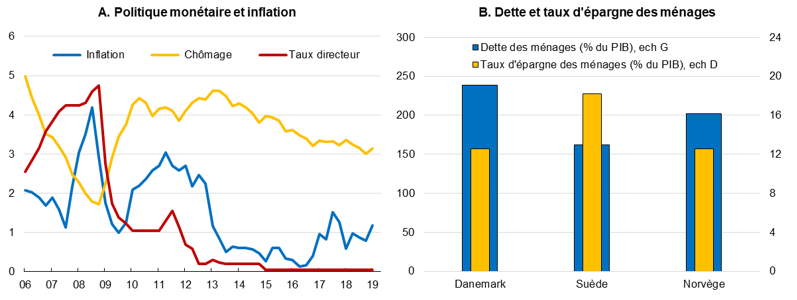

Despite a slight slowdown in 2018 (1.4%), Denmark has returned to growth, posting consecutive GDP increases of 2.6% and 2.2% (in GA) since the last quarter of 2018, thanks in particular to robust exports and sustained private consumption despite a record household savings rate (12.6% of disposable income). Given Denmark’s specialization in high value-added sectors[5] that are less correlated with the business cycle, exports are expected to remain strong in 2019.

The marked tightening of the labor market, characterized by (i) declining unemployment (3.7%), (ii) the emergence of labor shortages, with nearly 20% of companies reporting skilled labor shortages as the main obstacle to their business (the highest since 2010), (iii) sustained wage growth since 2016 (+2.5% in Q1 2019) and (iv) manufacturing capacity utilization at its highest cyclical level since the 2009 financial crisis, should revive inflationary pressures, which have been sluggish since early 2013 but have shown signs of picking up since 2017 (Chart 3, A). Rising real wages and falling unemployment should also support private household consumption, even if households continue to save in view of the risk of debt, which reached 239% of GDP in 2017 according to Eurostat.

With real wages accelerating, growth picking up and inflation moving closer to its medium-term target, while the same conditions are tending to ease in the eurozone, the conditions appear to be in place for an earlier (albeit slight) tightening by the Nationalbank compared with the ECB. However, raising rates[6] would imply an appreciation of the domestic currency against the euro (while the central bank is seeking to maintain the Danish krone’s peg at DKK 7.46 per EUR), and could undermine exports, which are expected to remain robust throughout the year, as well as raise the prospect of certain real estate risks materializing, such as a deterioration in household solvency given their high levels of debt (Chart 3, B). However, these risks are lower than in Sweden, as the majority of mortgages are fixed-rate. Other uncertainties weighing on the international environment, such as a more pronounced slowdown in growth in the eurozone than anticipated or a no-deal Brexit[7], also point to a status quo in monetary policy.

Figure 3: Economic and risk indicators in Denmark

Source: Statistics Denmark, Danmarks Nationalbank, Eurostat, and BSI Economics.

4. Norway bucks the trend

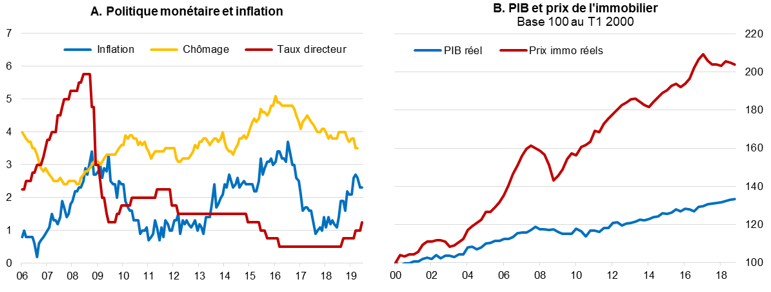

Bucking the slowdown in economic activity in Europe and among the major advanced economies, Norwegian growth is showing signs of acceleration (+0.3% in GT for the continental economy in Q1 2019, after +1.1% in Q4). This acceleration in activity is mainly due to strong private consumption and exports (up 0.5% and 2.2% in real terms, respectively) and is expected to continue throughout the year with the development of certain oil projects. The IMF has revised its forecast for Norwegian mainland GDP growth[8] upwards to 2.5% this year, after 2.2% in 2018, despite signs of a slowdown among its main trading partners, particularly in Europe. Although Norwegian inflation has slowed slightly since the beginning of the second quarter, it remains above the Norges Bank’s target due to the combined effects of a tightening labor market (Figure 4, A), with solid real wage growth (+2.8% in 2018) and a decline in the unemployment rate (3.8%), and the slight depreciation of the Norwegian krone that accompanied the downward trend in Brent prices at the end of 2018.

Despite this domestic outlook, Norway is exposed to risks linked to the recent reversal in real estate price dynamics, which had more than doubled since the crisis (Chart 4, B). Nevertheless, solid real wage growth, healthy bank profitability, and the strengthening of the prudential framework provide reassurance about the potential adverse effects of monetary policy tightening on households’ ability to finance their debt (which reached 200% of GDP at the end of 2018).

Against a backdrop of robust domestic indicators, a positive output gap since the end of 2018, an upbeat outlook for 2019, and a broadly neutral balance of risks, the central bank has raised rates three times (by 25 basis points each time) since September 2018 (most recently on June 20, 2019) and expects its monetary policy rate to reach 1.75% by early 2020, up from 1.25% currently.

Chart 4: Economic and risk indicators in Norway

Source: Statistics Norway, Norges Bank, OECD, and BSI Economics.

Not all « in the same boat »

Monetary policy decisions in the Nordic countries reflect divergent outlooks and trajectories for their economies. While real estate risks and domestic developments are hampering the Riksbank’s actions in Sweden, they appear to be contained and favorable to the outlook for Denmark and Norway. Swedish monetary policy is therefore likely to remain cautious in the wake of monetary easing by the Fed and the ECB, just as the krona’s peg to the euro will force the Danish central bank to follow the ECB’s lead despite favorable domestic conditions. Only Norway, bucking the global economic trend and with a broadly neutral balance of risks, can proceed with the normalisation of its monetary policy.

Bibliography

Danmarks NationalBank (2019), « Comments on the Danish Economic Council’s discussion paper, Spring 2019 »

Danske Bank (2019), « Nordic Outlook: Economic and financial trends, » March 28, 2019

Financial Times (2019), « Hawkish Norges Bank raises rates for a third time in 12 months, » June 20, 2019

Norges Bank (2019), “Monetary Policy Report with financial stability assessment 2/19”

OECD (2019), OECD Economic Outlook, Volume 2019 Issue 1, OECD Publishing, Paris, https://doi.org/10.1787/b2e897b0-en.

Reserve Bank of New Zealand (2015), « Economic implications of high and rising household indebtedness, » Bulletin volume 78, No. 1, March 2015.

Smith, D., M. Hermansen, and S. Malthe-Thagaard (2019), « The potential economic impact of Brexit on Denmark, » OECD Economics Department Working Papers, No. 1544, OECD Publishing, Paris, https://doi.org/10.1787/41a95fb3-en.

Sveriges Riksbank (2019), Monetary Policy Report July 2019.

[1] In Denmark, the central bank’s main objective is to maintain the exchange rate within a range around 7.46 DKK/EUR. In effect, this transposes the ECB’s mandate into Danish monetary policy, namely to keep inflation « below, but close to, 2% » in the medium term.

[2] Norway’s openness to foreign trade is more difficult to quantify given the concentration of the country’s experts on petroleum products.

[3] Unemployment hysteresis refers to a situation where the unemployment rate remains structurally high despite a significant recovery in economic activity.

[4]Potentially reflecting common value chains, there is a very strong and lasting correlation between German and Swedish manufacturing PMIs. It would therefore be difficult to explain a manufacturing slowdown in Germany without Sweden feeling the repercussions, especially after the publication of German growth figures pointing to a contraction in the second quarter of 2019.

[5]Notably in the pharmaceutical, shipbuilding and wind turbine component industries.

[6]Denmark has several monetary policy rates, like the ECB. The rate shown in Figure 2A is the rate at which the Central Bank grants loans to banks.

[7]The United Kingdom is one of Denmark’s main export markets.

[8]Excluding offshore activities related to the oil industry.