Relevance of the topic : On May 5, 2019, Donald Trump increased tariffs on Chinese imports, which he had already taxed at 10% in September 2018. At the same time, the U.S. trade deficit reached its highest level in 10 years. This article explains why U.S. trade policy has not reversed this trend and highlights the structural problems that explain this deficit.

Summary:

- In 2018, the US increased tariffs on nearly $300 billion worth of imports. The goal announced by the US administration when these measures were introduced was to reduce the US trade deficit, the largest in the world. Despite these new tariff barriers, the trade deficit reached its highest level at the end of 2018.

- The theoretical effect of a protectionist policy implemented by a « major » country is uncertain, but the international division of labor and the pricing of foreign firms partly explain the failure of this policy. The tariff increases ended up being paid for by US consumers and firms.

- This raises the question of a country’s ability to rebalance its trade balance. A recent IMF study indicates that internal imbalances, which are the source of trade imbalances, should be addressed rather than attempting to regulate trade itself.

At the end of 2017, the US trade deficit stood at USD 800 billion (4% of US GDP), of which USD 375 billion was with China. The US administration seemed convinced that the US trade deficit was due to unfair practices on the part of its partners and excessive trade barriers abroad. It therefore decided to impose additional tariffs on more than $300 billion worth of imports in 2018 alone. The underlying logic is that higher tariffs can increase the price of foreign products, leading to a decline in the quantities imported and thus improving the trade balance.

However, the US trade deficit continued to widen, reaching its highest level in 10 years at the end of 2018, as shown in Figure 1. Between 2010 and 2018, it increased by 37%, and by 53% with regard to China. Bilateral trade balances with the partners most affected by the increase in tariffs, namely China, Canada, the European Union, South Korea, and Mexico, have also remained on their initial trajectory. In particular, the trade deficit with China accounted for 47% of the total deficit in 2018, signaling the failure of US trade policy, at least in the short term.

What explains this lack of results in the US trade balance? What theoretical factors could have predicted and explain these initial results?

Figure 1: U.S. trade balance, trade in goods, in millions of USD (2010-2018)

« I’m a tariff guy, » Donald Trump (2018)

In theory, tariffs increase the price of imported goods and services, thereby reducing the quantities imported, which, all other things being equal, should lead to an improvement in the trade balance. However, several theoretical articles (see Lindé and Pescatori, 2019[1]) show that things are not that simple. A protectionist policy, by increasing the price of imported products (whether consumed or used in the production of other goods), can lead to a rise in the general level of consumer prices, and in response to this inflation, the central bank is forced to raise interest rates. This theoretically implies a relative appreciation of the currency, which weighs on the price competitiveness of exports, causing them to decline, but which will increase imports (foreign products cost less in domestic currency, but domestic products cost more in foreign currency). Ultimately, the effect is neutral on the trade balance: this is Lerner’s symmetry.

However, this reasoning does not take into account the particular position of the United States. The effect of a trade policy differs depending on whether it is implemented by a small or a large country (where the size of a country is defined according to its ability to influence global demand or supply). If a country introduces a new tariff, this will have the effect of reducing domestic demand for the targeted good. However, if this country is « large » and represents a significant share of the market in question, this decline will be felt globally: foreign producers will be impacted and will adjust their prices downward to compensate for the drop in demand. According to the theory of optimal tariffs, it is possible to find a tariff that, when implemented, will drive down the global price in the short term, when production quantities have not yet adjusted. Thus, the increase in the final price (including tax) is less than when considering a small economy, whose demand conditions are negligible relative to global demand.

The theoretical effect of a large country increasing customs duties is therefore uncertain. However, the specific conditions of current globalization are important factors that explain why a trade policy can ultimately backfire on the country that implements it.

« How to lose a trade war, » Paul Krugman (July 2018)

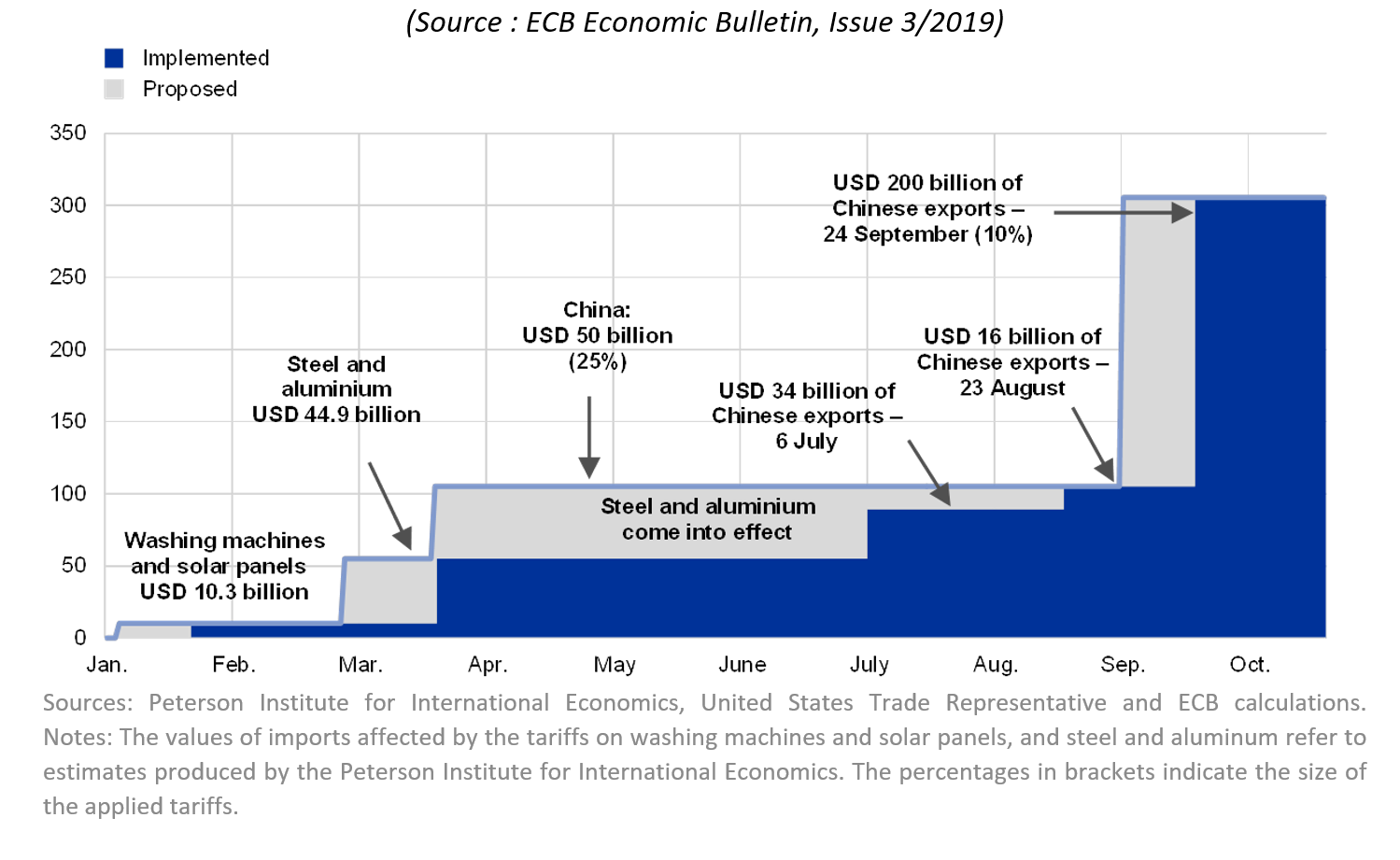

One of the first threats that a protectionist policy poses to an economy is inflation. The link between higher tariffs and inflation is based mainly on the behavior of foreign companies. When a tariff increases, a company may choose to pass on all or part of the increase to its selling price, in which case it is the consumer who bears the tax. But it may also decide to absorb part of the tariff increase into its margin, which will decrease. The higher this share, the less prices will increase, and vice versa. In a recent study, Amiti, Redding, and Weinstein[2] showed that the margins of firms exporting to the United States remained unchanged, indicating that the entire increase in tariffs was passed on to selling prices. It was therefore American consumers and American companies importing goods necessary for their production that paid the protectionist taxes. They estimate that by the end of 2018, the total cost of these measures was USD 4 billion per month. Jean and Santoni[3] estimate that if all the protectionist measures announced by Donald Trump were implemented (see Figure 2, taken from the work of Gunnella and Quaglietti[4]), this would push inflation up by one percentage point[5]. A further rise in inflation could prompt the Fed to raise interest rates, which it has already begun to do since 2017, given the current period of economic stability and low unemployment in the United States. This normalization of monetary policy, after years of near-zero interest rates, partly explains the appreciation of the dollar during 2018, which may have had a negative impact on the US trade balance, further reducing the possibilities for improvement.

Figure 2: US protectionist measures announced and implemented in 2018

Sources: Peterson Institute for International Economics, United States Trade Representative, and ECB calculations.

Notes: The values of imports affected by the tariffs on washing machines and solar panels, and steel and aluminum refer to estimates produced by the Peterson Institute for International Economics. The percentages in brackets indicate the size of the applied tariffs.

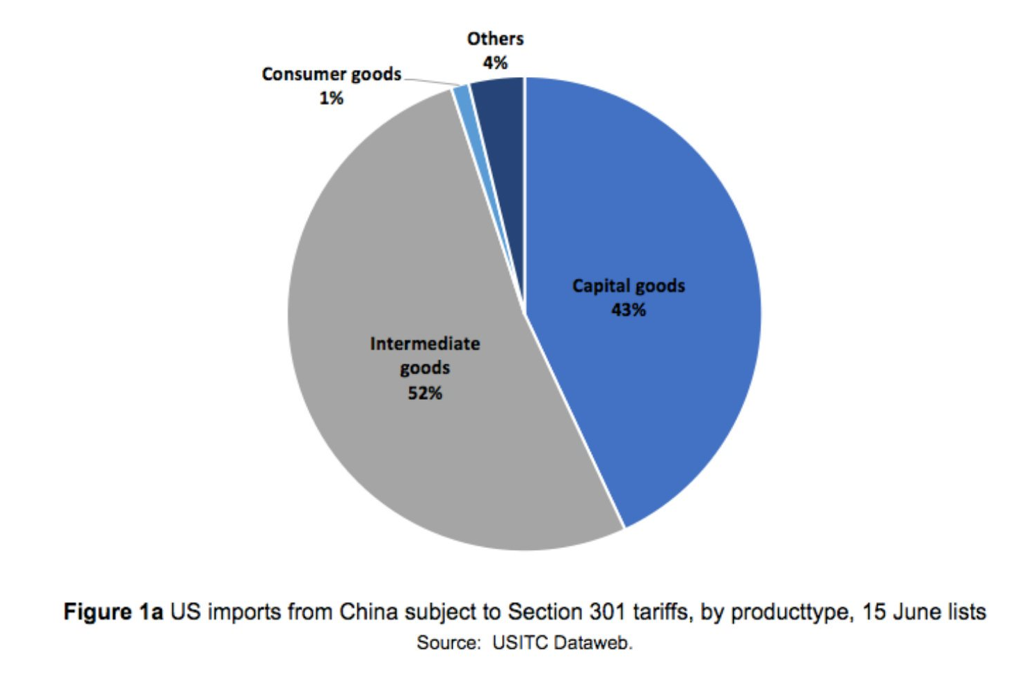

Furthermore, in order to hope for an improvement in the trade balance, this price increase would have had to be followed by a decrease in the quantities imported, which does not seem to have been the case. This is due in particular to the fact that the global economy is now organized around an international division of labor. A country does not produce a good from start to finish; it imports various parts necessary for the production of that good, just as it produces intermediate goods that it will then export: these are international value chains. Due to this growing interdependence between globalized economies, an increase in customs duties can have negative repercussions on the national economy. From this perspective, the US measures appear particularly « ill-conceived »: 95% of them concern intermediate consumption goods or capital goods (e.g., machinery), as illustrated in Figure 3, taken from the work of Bown, Jung, and Lu[6].

Figure 3: US imports from China taxed under Section 301 (Bown et al., 2018)

Finally, even if these measures had succeeded in reducing US imports, they did not take into account the retaliatory measures taken by partner economies. Half of Chinese exports to the United States are affected by these additional tariffs, which explains China’s protectionist response. Thus, at the end of July 2018, China, Canada, the European Union, Mexico, Turkey, and India increased their tariffs on agricultural products from the United States in response to the taxes on aluminum and steel. In total, nearly $27 billion worth of US agricultural exports are now subject to retaliatory tariffs, which will not help the US trade balance to recover.

« No more massive trade deficits! » Donald Trump (June 4, 2018)

What about the US trade deficit? A new IMF study[7] shows that it is difficult to set a target for a specific trade balance, and that if this is the government’s intention, macroeconomic policies (which aim to influence domestic demand and production) should be implemented rather than microeconomic policies (such as tariffs).

Trade imbalances are symptoms of economic imbalances across the entire country. When domestic production is too low to satisfy domestic consumers, they turn to foreign goods, thereby increasing imports: it is excess demand that drives the trade deficit. At the same time, if demand is high, savings will decline, reducing companies’ investment opportunities and thus their ability to adapt production to domestic demand. A trade deficit therefore reflects excess domestic demand and a savings deficit. Gross savings accounted for 17.5% of GDP in the United States in 2018, compared with 28% in Germany and 47% in China, two countries with large trade surpluses.

As a result, it is more difficult to influence trade balances by trying to control trade flows than by addressing internal imbalances, of which trade imbalances are merely a reflection. The United States would therefore need to implement policies to support savings, for example by limiting credit consumption. The growing proportion of the aging U.S. population also represents a major challenge. Modigliani’s life cycle theory explains that the life of an economic agent is organized into three phases: the student population incurs debt, the working population consumes more but also saves more in anticipation of the third phase, retirement, during which consumption exceeds savings. Thus, with an aging population, US savings will decline, risking a further widening of the trade deficit. US economic policies must take these dynamics into account, as their impact on savings is likely to be exacerbated by recent decisions. Indeed, last year’s tax cuts , by increasing the purchasing power of American households and thus imports, will most likely contribute to an increase in the trade deficit.

This is without mentioning the special position of the United States as the cornerstone of the international monetary system. A negative trade balance indicates that a country consumes more foreign goods than it sells to other countries. The counterpart to a trade deficit is therefore debt to the rest of the world, meaning that foreigners invest and lend more to the United States than the United States does abroad: nearly one-third of U.S. public debt is held by foreign investors. This massive debt is made possible because the dollar is the main reserve currency. Foreign economic agents want to hold dollars and prefer to invest in US assets, which they consider to be safer. It is therefore the status of the US currency, because it is always in demand, particularly in times of crisis, that imposes a trade deficit on the United States and allows it to be financed at low cost. To balance its trade, the US would therefore have to give up the international status of its currency, as well as the easy financing of its public debt, the famous « exorbitant privilege. »

Conclusion

Balancing the trade balance through trade policy alone is an almost impossible task today, given the interdependence of economies. We can therefore expect the new tariffs (25%) on Chinese imports to further worsen the US trade deficit, especially since the Chinese « retaliated » on May 13, 2019 with tariff increases on US imports. If Donald Trump truly wants to rebalance the trade balance, structural policies must be put in place to increase savings and reduce demand for foreign goods.

[1] Jesper Lindé and Andrea Pescatori, « The macroeconomic effect of trade tariffs: revisiting the Lerner symmetry result » (2019). Journal of International Money and Finance.

[3] Sébastien Jean and Gianluca Santoni, “How far will Trump protectionism push up inflation?” (2018). CEPII Policy Brief No. 23-2018.

[4] Vanessa Gunnella and Lucia Quaglietti, “The economic implications of rising protectionism: a euro area and global perspective,” ECB Economic Bulletin, Issue 3/2019.

[5] The inflation rate was 1.91% in December 2018 (OECD).

[6] Chad Bown, Euijin Jung, Zhiyao (Lucy) Lu, “Trump, China, and tariffs: From soybeans tosemiconductors” Vox Column, June 19, 2018

[7] “The drivers of bilateral trade and the spillovers from tariffs” (2019). World Economic Outlook, Chapter 4. International Monetary Fund.

[8] US household debt accounted for 77% of US GDP in 2017 (see IMF Global Debt Database).