Abstract :

- After a very dynamic 2017, a high degree of uncertainty, trade tensions, and the slowdown in emerging economies are now clouding the economic outlook for the eurozone.

- The euro area will therefore need to refocus on its internal drivers of economic growth and will also have to rely on an improvement in the labor market and an increase in real wages to boost household consumption.

- In the coming months, euro area heads of state and government will have to decide on reforms that are crucial for the future of the euro area, including the introduction of a euro area budget, the reform of the European Stability Mechanism, and the completion of the banking union.

- However, the heterogeneity of member states’ economies makes it difficult to adopt these common structural reforms.

On December 14, at the European Council, the heads of state and government of the eurozone will aim to confirm the progress made on economic and monetary union. They will discuss possible reforms with a view to deepening the eurozone.This Eurogroup meeting is an opportunity to review the economic outlook for the eurozone.

After the sovereign debt crisis, which severely affected all of its economies, particularly the most fragile ones, the eurozone has experienced five consecutive years of growth, marking a sustainable and relatively widespread economic recovery. In the near future, however, economic growth in the eurozone is likely to be weakened by the turbulent international environment, but it will nevertheless be able to rely on domestic demand. The prospect of European elections should provide an opportunity to address the major economic challenges facing the heads of state and government of the eurozone.

1. Economic growth clouded by a highly uncertain international environment

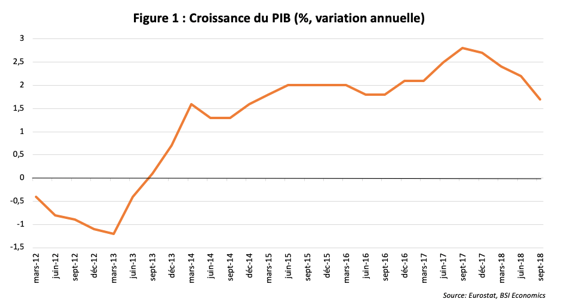

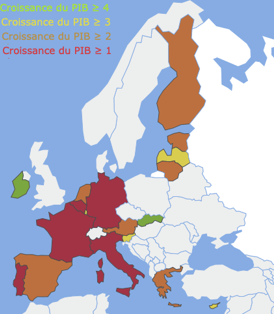

After peaking in 2017 (Figure 1) at 2.4% (its highest level in ten years, thanks in particular to a particularly favorable global environment), economic growth in the eurozone is expected to slow over the next three years, reaching 2.1% in 2018, then 1.9% in 2019 and 1.7% in 2020, according to the European Commission’s autumn 2018 forecasts, which have been revised downwards since those published in the spring. While growth will continue to be supported by strong domestic demand and investment, it will suffer from the deterioration of external factors, negatively affecting the contribution of foreign trade. While it will remain dynamic in Ireland and Slovakia (Figure 2), GDP growth will fall below 2% in Portugal in 2019 (1.8%, compared with 2.2% in 2018). In France, growth will slow to 1.6% in 2019, while it will increase to 1.8% in Germany.

Figure 2: GDP growth in 2019 (%)

Source: Eurostat, BSI Economics

The global economy is indeed going through difficult times:

- On the one hand, renewed trade tensions are negatively affecting global economic activity. The European Commission predicts that new tariff and non-tariff barriers will emerge, which will have a considerable impact on international trade and global growth.

- On the other hand, the tightening of US monetary policy is penalizing emerging countries.

The euro area is a relatively open economy, with strong integration into global value chains. It has solid trade relations with emerging and developing countries (27.3% of total euro area exports in 2017[1]). Eurozone commercial banks are also exposed to these markets. While the exposures of eurozone banks may appear relatively low at first glance (according to the ECB, balance sheet exposures to emerging economies as a whole amounted to €1.5 trillion, or 7% of total assets, at the beginning of 2018), the resilience of some euro area institutions could be tested if the turmoil persists. According to the ECB, ten large euro area institutions account for 93% of total exposures to certain emerging economies (namely Argentina, Brazil, China, Indonesia, Malaysia, Mexico, South Africa, and Turkey).

Furthermore, in the absence of a Brexit agreement, the eurozone could also suffer from the deterioration of trade and financial relations with the United Kingdom.

Ultimately, the prospects of an economic slowdown in the eurozone are largely due to the weak contribution of net trade to growth. With external demand set to weaken further, support for GDP growth will therefore depend mainly on domestic indicators.

2. The eurozone will have to rely on its domestic fundamentals

Growth in private consumption (+1.6% in 2018 and +1.8% in 2019, according to Eurostat data) is expected to remain one of the main drivers of growth. This will be stimulated by improvements in the labor market, wage increases, and expansionary fiscal measures in certain Member States, such as Portugal and Ireland.

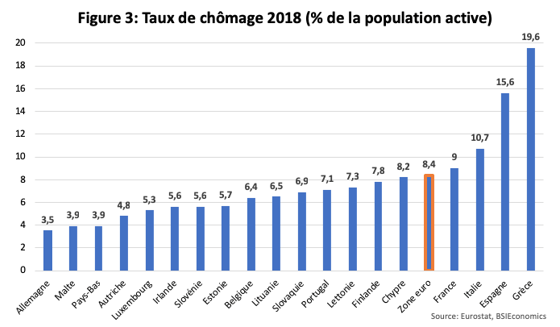

Within the eurozone, according to the European Commission, the unemployment rate is expected to fall to 8.4% this year (from 9.1% in 2017), then to 7.9% in 2019 and 7.5% in 2020, despite the slowdown in growth. However, job creation is expected to be hampered by growing labor shortages and slowing economic growth. Net job creation in the eurozone is therefore expected to slow from 1.4% in 2018 to 1.1% in 2019 and 0.9% in 2020. Although it is expected to fall in all euro area countries in 2018 and 2019 (with the exception of Ireland and Malta), the unemployment rate remains very uneven across countries (Figure 3), ranging from 3.5% in Germany to 19.6% in Greece in 2018. At the same time, real compensation per employee is expected to grow by 0.6% in 2018, 0.2% in 2019, and 0.8% in 2020. The rise in inflation (to 1.8% in 2018 and 2019, compared with 1.5% in 2017) could slow down a stronger increase in household purchasing power.

According to European Central Bank (ECB) projections, inflation is converging towards levels below, but close to, 2% in the medium term, in line with its target. At the end of December 2018, the ECB will therefore end net purchases under its asset purchase program (better known as » quantitative easing « ), which is designed to support inflation while bolstering economic activity. However, the institution has indicated that it does not intend to end its expansionary monetary policy, specifying that its key interest rates will remain at their historically low levels at least until the end of summer 2019.

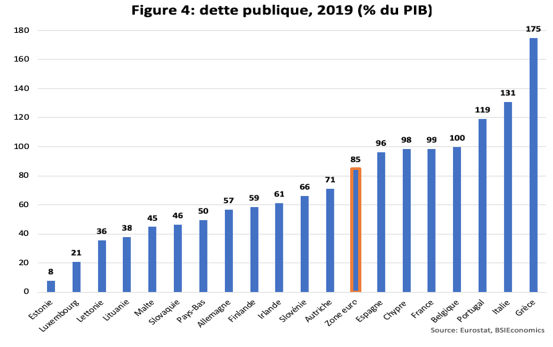

At the same time, several eurozone countries will adopt expansionary fiscal policies. The eurozone’s aggregate structural public balance (the public balance adjusted for the effects of the economic cycle) is therefore expected to deteriorate slightly in 2019, from a structural public deficit of -0.7% of GDP in 2018 to -1% of GDP in 2019. The high degree of heterogeneity in public finances (Figure 4) would be a major obstacle to the implementation of common fiscal tools (see Part 3).

Furthermore, certain internal tensions within the eurozone are clouding its economic outlook. Uncertainty surrounding the health of Italy’s public finances is leading to higher interest rates on the country’s public debt and raising the issue of the interaction between sovereign debt and the banking sector. Indeed, the rise in the eurozone sovereign spread (the difference between the interest rate on Italian and German sovereign bonds, the latter being considered risk-free) marks an increase in the risk perceived by financial markets with regard to Italian debt. This increases the cost of borrowing for the Italian government, which must borrow more to finance a higher public deficit (2.4% of GDP in 2019) than initially planned. Italy’s public debt-to-GDP ratio is the second highest in the eurozone (131% of GDP in 2018) after Greece. According to the ECB, persistent tensions on the Italian bond market could affect other indebted eurozone countries and lead to higher borrowing costs. In addition, eurozone financial institutions (excluding the European System of Central Banks) hold €262 billion of Italian public debt, according to ECB figures (11.5% of total public debt). However, when the interest rate on a bond rises, the price of that bond falls. Thus, the rise in Italian sovereign bond yields is eroding the value of banks’ assets and could, if it persists in the longer term, affect the European banking system. But while this risk is currently contained, the Italian crisis poses a major challenge for future reforms of the eurozone.

3. What reform proposals are there to strengthen the eurozone?

For several months, eurozone finance ministers have been working on a set of specifications for deepening Economic and Monetary Union (EMU), which will be discussed by heads of state and government at the eurozone summit in mid-December.

To prevent another crisis, some eurozone countries, including France, are seeking to increase the integration of economies within the zone, notably through a eurozone budget, a European monetary fund, and the completion of banking union. However, many disagreements remain between member states.

3.a) Towards the introduction of a eurozone budget by 2021?

In mid-November, the French and German finance ministers announced a joint position on the idea of giving the eurozone its own budget. The idea is to promote competitiveness, convergence, and stabilization in the eurozone. Initially, this financial capacity would focus on convergence between the still very heterogeneous economies of the member countries. In addition, eurozone member states would only benefit from this financial capacity if they accepted the recommendations of the European Commission as part of its annual budgetary surveillance.

Ultimately, this joint contribution could be used to finance European unemployment insurance and supplement the Fund for Strategic Investments in States temporarily unable to ensure the balance of their public finances, thereby supporting long-term investment.

However, Member States are still divided on this issue. Some even dispute the usefulness of such a financial capacity for the eurozone. The Nordic and Baltic countries are not convinced that it is necessary to have a separate budget to strengthen the single currency.

3.b) The transformation of the European Stability Mechanism into a European Monetary Fund

The European Stability Mechanism (ESM), created in the context of the sovereign debt crisis, is a rescue fund used in the event of financial crises. A majority of eurozone governments are in favor of transforming the current ESM into a regional equivalent of the International Monetary Fund in order to prevent further crises on a scale comparable to the sovereign debt crisis. However, they are still far from agreeing on a common project.

The German version of the « European Monetary Fund » project to help eurozone countries in difficulty in the future sets out strict eligibility criteria, which would effectively exclude countries deemed too lax in reducing public debt. To be eligible for financial assistance, Germany believes that a country should have a budget deficit of less than 3% of GDP and public debt of less than 60% of GDP, unless it has reduced its debt by 0.5 percentage points of GDP in each of the three years prior to its request for assistance.

3.c) Completing the banking union

The roadmap for eurozone leaders also includes the completion of the banking union, with the creation of a European deposit guarantee scheme for savers. However, Germany, among others, is reluctant to do so. While all countries agree that this instrument is useful, they disagree on the preconditions. These are linked, on the one hand, to the risk of the banking system, which in some cases still contains too many non-performing loans, and, on the other hand, to the excessive proportion of sovereign debt securities on the balance sheets of banks in some countries.

Conclusion

The eurozone could experience a period of economic slowdown due to an unfavorable international environment. However, it will be able to count on strong domestic demand, stimulated by rising wages, to support growth.

With the European elections approaching, several proposals are on the table for heads of state and government to reform the eurozone and move towards greater integration. Nevertheless, the heterogeneity of the member states’ economies makes it difficult to adopt a common roadmap to best prepare the eurozone for the next crisis.

Bibliography:

European Economic Forecast, Autumn 2018, European Commission

OECD Economic Surveys, Euro Area, June 2018, OECD

Economic Surveys of the Euro Area 2018, OECD

Cyclical Adjustment of Budget Balances, Autumn 2018, European Commission

Euro Area Policies, July 2018, IMF

Financial Stability Review, November 2018, ECB

[1] Calculation made by subtracting exports from advanced economies (IMF classification) from total exports outside the euro area: United States, Canada, United Kingdom, Denmark, Switzerland, Sweden, Norway, Iceland, Czech Republic, Australia, New Zealand, Hong Kong, Singapore, Taiwan, South Korea, and Israel.