Usefulness of the article: This article identifies the mechanisms through which unconventional monetary policy affects asset prices. The aim is to provide background information for the debate on the emergence of asset price bubbles allegedly caused by unconventional monetary policy instruments.

Abstract:

- The Covid-19 crisis has reignited the debate on the possible adverse effects of unconventional monetary policy measures on asset prices. The abundance of liquidity injected into financial markets could fuel the formation of asset price bubbles.

- Asset purchase programs (or quantitative easing) affect asset prices mainly through the portfolio reallocation mechanism, but also through the signaling effect, the liquidity channel, the duration effect, and the risk-taking channel.

- It is particularly difficult to determine how much of an asset’s price increase is attributable to economic fundamentals and how much is attributable to the « bubble » component.

Since the 2007-2008 financial crisis, central banks have implemented a range of unconventional tools (asset purchase programs, exceptional loans to commercial banks, negative deposit rates, guidance on future rates) in order to compensate for the floor rate (key interest rate at 0% or close to 0). These instruments are designed to stimulate economic activity and put an end to financial market malfunctions.

These monetary policy tools were initially intended to be phased out as soon as signs of economic recovery appeared, particularly when inflation approached its target (close to 2% for the ECB). It now seems clear that central banks are not ready to remove these measures from their toolbox. Indeed, the coronavirus crisis has once again highlighted the importance of central banks in their role as lenders of last resort. They have responded quickly and intensively to the crisis, both by extending existing programs and by introducing new measures.

This reinforces the need to consider the possible unanticipated side effects of these instruments. Among these, the question of a possible adverse effect of unconventional monetary policy, particularly asset purchase programs, on asset prices had already been raised in the wake of the 2007-2008 crisis. This debate has become even more heated since the health crisis, as central banks have further increased the accommodative nature of their policies and have even gone against some of their legal constraints. For example, the Fed has acquired « fallen angels » (corporate bonds that have been downgraded to high yield[2]), even though its previous statements indicated that it would limit itself to investment grade bonds[3], and the ECB has decided to temporarily deviate from its proportionality rule regarding sovereign bond purchases.Could these various actions lead to distortions in asset prices?

On the other hand, it is important to remember that the 2007-2008 crisis and the Covid-19 crisis are very different in nature. In the second crisis, banks and other financial institutions are not at the root of the shock, and the financial system continues to function smoothly despite sharp declines in the stock markets. However, central banks have used the same instruments as in the previous crisis. This raises the following questions: are these instruments the right response to this crisis? Will they not lead to asset price bubbles, given that this shock originated in the real economy and not in the financial sphere?

1) Asset prices: an important channel for monetary policy transmission

Like conventional monetary policy, unconventional monetary policy affects economic activity in part through the asset price channel. However, the mechanisms are somewhat different. On the side of unorthodox monetary policy, particularly asset purchase programs, we find the portfolio reallocation mechanism, the signaling effect, the liquidity channel, and the duration effect.

1.1 The portfolio reallocation channel

Through their asset purchase programs on the secondary market, central banks target certain market segments and reduce the supply of securities on the bond market. Assuming that demand in this market remains unchanged, bond prices rise and yields on these securities fall, leading buyers to turn to other financial assets with the same maturity but higher risk-adjusted returns. Investors then turn to riskier securities, which are an attractive alternative to the securities purchased by central banks, whose yields are falling sharply or even entering negative territory (US Treasury bills, German government debt).

Although this is one of the expected effects of quantitative easing, the artificial reduction in risk premiums (the difference between the observed performance of a financial security and the risk-free interest rate) introduces the risk of asset price bubbles. There is an inverse relationship between the fundamental value of an asset and its interest rate: a rise in price leads to a fall in yield.

Central banks initially limited their purchases to assets considered risk-free (sovereign bonds), but then broadened their scope to include risky assets such as corporate bonds. Since March 2016, the ECB has been purchasing European corporate bonds as part of its CSPP (Corporate Sector Purchase Program). The Fed has gone even further and, since the coronavirus crisis, has been buying ETFs (Exchange-Traded Funds) specializing in high-yield bonds. By purchasing increasingly risky securities, central banks are encouraging investors to reallocate their portfolios towards ever riskier securities, driving up their valuations.

1.2 Other transmission channels

Other transmission channels include the signaling effect (or expectations channel). Unorthodox instruments can lower interest rates on long-term assets by reducing interest rate expectations. Investors also anticipate an improvement in economic fundamentals as a result of expansionary monetary policy. The credibility of the central bank’s commitment not to change its monetary policy if persistent inflationary pressures emerge is therefore essential.

The liquidity channel is also part of the asset price channel. When there is a money supply shock caused by central bank purchases of securities, the liquidity premium decreases, which reduces long-term rates and causes asset prices to rise. Through its asset purchase programs, the central bank effectively offers market participants a guarantee that they will be able to resell their securities. On the other hand, purchases of long-term assets reduce the average duration of the asset stock held by investors. With less maturity risk, investors should demand a lower premium to maintain this risk. Thus, asset prices should rise. This is known as the duration effect.

Finally, the risk-taking channel (Borio and Zhu, 2008), a channel for transmitting conventional monetary policy, also works for unconventional monetary policy. The underlying mechanism is as follows: central banks, through their unconventional monetary policy, reduce long-term interest rates. This leads to a decline in the profits of financial institutions. For banks, for example, lower lending rates squeeze the net interest margin (the difference between the interest rate at which banks lend and the rate at which they refinance), given that deposit rates for individuals cannot be below zero. To compensate for this loss, banks will increase their purchases of financial assets. De facto, increased demand for securities with unchanged supply will translate into higher asset prices. Here, investors are not seeking to substitute assets for securities purchased by central banks (portfolio reallocation channel) but are taking advantage of lower yields to increase the risk of their portfolios.

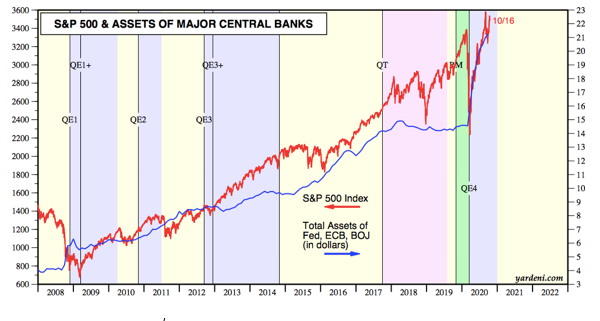

There seems to be a consensus on the positive effect of unconventional monetary policy tools on asset prices. Although correlation does not imply causation, the chart below shows that there is a high correlation between changes in the size of central bank balance sheets (a proxy for balance sheet policies) and the S&P 500. On the other hand, the question of whether the rise in asset prices is excessive or not in relation to fundamentals is more controversial.

Chart 1: Total assets on the balance sheets of the Fed, the ECB, and the BOJ (Bank of Japan) and the S&P 500

Source: Yardeni Research

2) By repeatedly using this channel, unconventional monetary policy could fuel the formation of asset price bubbles.

The objective here is to clearly define the term « asset price bubble » and to show the complexity of the debate surrounding the possible contribution of unconventional measures to the formation of bubbles.

2.1 Rising asset prices do not necessarily mean asset price bubbles

A speculative bubble occurs when the price of an asset rises continuously and excessively, to the point where it deviates from its real value[5]. This initial rise is then self-perpetuating due to investor behavior and eventually becomes completely disconnected from the real economy. This long phase of rising prices is followed by the sudden bursting of the bubble, bringing prices back to their initial levels.

The fundamental value of an asset can be defined as the total anticipated profits of the company, to which must be added changes in the risk premium and interest rates. It therefore depends on macroeconomic factors (growth rates, inflation rates) as well as financial factors (availability of credit, liquidity).

Any increase in the price of an asset, even a significant one, cannot therefore be considered a bubble. A bubble occurs when the appreciation of an asset is disconnected from its fundamental value. It is particularly difficult to detect the emergence of a financial bubble because the fundamental value of an asset and the bubble component are not observable and must therefore be inferred from empirical or theoretical models.

2.2 Arguments that the ultra-accommodative nature of unconventional monetary policy could lead to future speculative bubbles

Returning to the portfolio reallocation channel defined above, investors may not fully grasp the extent of the risk being added to their portfolios because fundamentals may not improve at the same pace as expansionary monetary policies affect the price and yield of securities purchased under asset purchase programs. As a result, yields are falling much faster than the pace of improvement in economic fundamentals.

The search for yield is pushing investors to take ever greater risks in order to avoid losing profits. This frantic quest for yield, due to the flattening of the risk-return curve, may lead investors to act independently of fundamentals.

Furthermore, if the rise in asset prices is merely a reflection of central bank action, this would contribute to distorting the overall functioning of financial markets. In the absence of intervention by monetary authorities, market prices are determined by investor preferences (demand) and the economic health of companies (supply).

Furthermore, while studies do not seem to have reached this conclusion for the post-financial crisis period of 2007-2008, the results could be different for the post-Covid-19 crisis period. The argument is as follows: as stated in the introduction to this article, the Covid-19 crisis originated in the real, non-financial sphere. Therefore, in the absence of undervalued assets and financial market dysfunction, does the massive intervention by central banks not risk artificially increasing the value of assets and fueling the formation of bubbles?

To demonstrate the role of unconventional monetary policy in bubble formation, we need to be able to calculate its impact on the component of asset prices that is not explained by economic fundamentals (Blot, Hubert, and Labondance, 2015).

Conclusion

The unconventional monetary policy measures implemented by central banks since the 2007-2008 financial crisis and reinforced since the Covid-19 crisis affect the real economy in part through the asset price channel. While these measures have proven effective in calming financial tensions and reviving economic activity in recent years, the systematic use of these tools could also have undesirable effects. In particular, the abundance of liquidity injected into financial markets could lead to overvaluation of financial assets and thus fuel the formation of asset price bubbles, the bursting of which would threaten the entire financial system.

Bibliography

- Amundi Asset Management (June 2020), “The day after 5 – New frontiers for central banks”

- Bloomberg (July 25, 2019), “Central Bankers Are Playing a Dangerous Game With Asset Prices”

- Blot C., Hubert P. & Labondance F. (2015), “Does monetary policy create bubbles?”, OFCE Review, 144

- BNP Paribas Wealth Management (June 26, 2020), “Central bank QE: How far will risk taking go?”

- Borio C. and Zhu H. (2008), “Capital regulation, risk-taking and monetary policy: a missing link in the transmission mechanism?”, BIS working paper, No. 268

- Lacalle D. (2018), “Are the effects of unconventional monetary policy on financial markets causing bubbles?”, https://doi.org/10.26870/jbafp.2018.01.003

[1] See the articles by Julien Pinter and Aymeric Ortmans on the responses of the European Central Bank (ECB) and the US Federal Reserve (Fed) to the Covid-19 crisis for a comprehensive list of these measures.

[2] High-yield bonds are speculative debt securities with a rating below BBB- from Standard & Poor’s or Baa3 from Moody’s.

[3]Investment grade bonds are bonds issued by borrowers that receive a rating ranging from AAA to BBB- from rating agencies, according to Standard & Poor’s scale.

[4] An ETF (exchange-traded fund), also known as a tracker, is an index fund that seeks to track the performance of a stock market index as closely as possible, both upwards and downwards.