The Tunisian economy post-revolution: ambition in the face of challenges (2/2)

The Business Climate

Summary :

· Decline in foreign direct investment (FDI) in Tunisia following the deterioration of the economic situation and, above all, the climate of insecurity and instability that characterized Tunisia in the post-revolution period of 2011;

· The « Tunisia 2020 » international investment conference heralds a new impetus for Tunisia, particularly in terms of attracting FDI;

· The success of the projects announced at the conference requires an improvement in the macroeconomic situation, a more effective fight against corruption, and, more generally, an improvement in the business environment.

Tunisia’s economic performance in 2016 was considered to be below expectations. In addition to weak growth, Tunisia has become less attractive to foreign investment. In order to return to growth, it is essential to improve the business climate.

This note provides a description of the current situation of foreign direct investment (FDI) in Tunisia and an assessment of the business environment.

The state of foreign investment in Tunisia

1- Foreign investment: Decline in inflows

In terms of capital movements, foreign investment has continued to decline in the post-revolution period. In 2016, investment fell by 7% (between January and November) compared with the same period in 2015. According to the BCT, foreign direct investment has been negatively affected by the deterioration of the geopolitical situation in relation to the Libyan crisis and the slowdown in the eurozone economy (Figure 1). In 2016, a 9.3% increase in FDI was recorded according to a report by the Foreign Investment Promotion Agency (FIPA-Tunisia).

Graph 1– Inbound FDI 2004-2015

2- Tunisia 2020: A breath of fresh air for the Tunisian economy

The link between FDI and growth has been well demonstrated in the literature. In particular, studies on Tunisia confirm the positive effect of FDI on growth (Soltani and Ochi, 2012; Bass, 2016)[1]. Recognizing Tunisia’s need to attract foreign capital, the government organized the « Tunisia 2020 » international investment conference in November 2016. This conference is part of the 2016-2020 investment plan designed by the government to enable Tunisia to achieve an annual growth rate of more than 4% from 2020 onwards.

The conference concluded with a series of investment, aid, and donation pledges from foreign donors totaling approximately €14 billion. In terms of pledges, Europe accounted for the lion’s share with €2.5 billion granted by the European Investment Bank (EIB) and more than €47 million from the European Bank for Reconstruction and Development (EBRD). Additional aid from the European Commission is planned for 2017. France is the leading foreign investor in Tunisia. According to the report by the ANIMA observatory on investment and partnerships in the Mediterranean, 211 French FDI announcements in Tunisia were already made during the period 2006-2015. The World Bank has also announced financial aid of €3.7 billion for the period 2016-2020.

Although these promises seem to offer hope for Tunisia’s economic transition, the realization of these potential investments (€6.1 billion represents firm commitments from foreign donors) is dependent on certain conditions, including macroeconomic stability, reform of public institutions, development of the financial sector, and, above all, improvement of the business climate.

The business environment: Review of developments

1- Democratic transition

Since 2011, Tunisia has been taking its first steps towards democratic transition, with a peaceful succession of governments, a multitude of political parties ranging from Islamists to liberals, and marked freedom of expression. According to the latest report (from 2015) by Global Democracy Rankings, Tunisia gained points on the democracy scale (+32 points) between 2010 and 2014. Although the impact of democracies on economic growth remains a subject of debate (Barro 1997, pp. 1 and 11), recent literature suggests that democracy has a positive effect on growth. Persson and Tabellini (2007) find that leaving a democracy causes a 2% decline in GDP per capita. Acemoglu et al (2015) find more conclusive results, with democratization having a positive effect on GDP per capita of around 20% in the long term. The authors also suggest that democracy’s effect on future GDP growth comes through encouraging investment, economic reforms, and education, and by reducing social conflicts. Based on these elements, Tunisia will need to leverage its democratic transition to boost economic activity.

2- Corruption

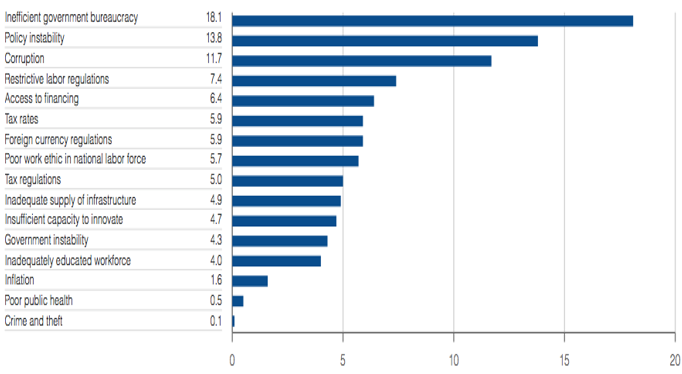

Corruption[2] was considered a hallmark of the regime that was overthrown in 2011. According to the 2016 Corruption Perceptions Index, Tunisia ranks75th, tied with Bulgaria, Kuwait, and Turkey. According to the same index, the level of corruption has remained relatively stable since 2012 (a score of 41/100, with 100 being the score for the country with the lowest level of corruption). This indicator is based on the assessment of political institutions and the quality of anti-corruption laws. The fight against corruption in Tunisia does not therefore seem to be making much progress. This observation is supported by the results of a survey of Tunisian business leaders on the business climate. 11.7% of respondents consider corruption to be the most problematic constraint to the success of projects (Figure 2). It should be noted, however, that the government is making serious efforts to combat corruption, notably through the « national anti-corruption strategy » officially adopted at the end of the national congress on the fight against corruption held in Tunis in December 2016, and the activities of the National Anti-Corruption Authority (INLUCC).

3- Quality of the business environment

In terms of the business environment, Tunisia’s position appears to be satisfactory, ranking 77th out of 190 countries considered in the World Bank’s Doing Business reports. In terms of ease of doing business, Tunisia performs better than the average for the MENA (Middle East & North Africa) region. Tunisia ranks behind Morocco (68th), which has been gaining points in recent years in terms of economic development and prosperity.

Figure 2 – Main constraints in the business environment

Source: World Economic Forum, Executive Opinion Survey 2016

According to the Doing Business 2017 report[3], Tunisia ranks103rd when taking into account all the procedures, costs, and time required to start a business. Morocco ranks40th, meaning it is easier to start a project in Morocco than in Tunisia. According to the rankings, Tunisia comes106th in terms of ease of paying taxes. It is nevertheless important to note that since 2011, Tunisia has introduced electronic payment methods, which have simplified tax payment procedures. Tunisia’s position improves when it comes to resolving insolvency (58th position).

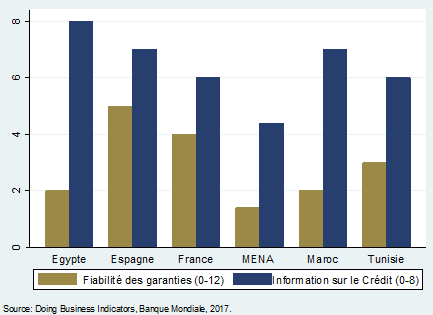

In terms of access to credit, Tunisia has moved up in the rankings compared to 2015, rising from127th to101st, tied with Morocco. The quality of access to credit is defined by Doing Business according to two indicators: the collateral reliability index (0-12), and the credit information index (0-8). Although Tunisia’s performance remains well above the MENA region average (Figure 3), the degree of collateral reliability is still considered low (3/12), but access to credit information can be considered acceptable (6/8). Access to finance is a necessary condition for ensuring the activity and sustainability of businesses. In Tunisia, despite the weight of small and medium-sized enterprises (SMEs), these firms continue to experience credit rationing (80% of SMEs surveyed[6] according to a study by Adair and Fhima, 2013). This is partly due to the guarantees required by banks, which exceed the capacities of SMEs. This idea is confirmed by the results of the 2016 Executive Opinion Survey, which assesses the major obstacles to the smooth running of business. Although inefficient public administration and political instability top the list, 6.4% of the firms surveyed cite access to finance as the major obstacle to business (see Figure 2). This obstacle has consistently been among the main constraints on business over the last decade (Schwab and Sala-i-Martin, 2014).

Figure 3 – Measures of the quality of access to credit

In terms of the business environment related to foreign trade, Tunisia is ranked92nd (out of 190). The assessment of this environment is based on the ease[8] of obtaining the documents necessary for transport, transit, and customs clearance in the ports of the destination country/country of origin, which enable the export/import to be completed, the quality of customs services, and the quality of transport. In this regard, the literature on international trade considers the quality of institutions to be one of the determinants of international trade (Lavallée, 2006). Improving export/import procedures would therefore lead to an improvement in Tunisia’s trade with the rest of the world.

Areas for improvement

Promoting Tunisia’s attractiveness in terms of FDI requires improving the country’s image in terms of security, macroeconomic stability, and, above all, the quality of the business environment.

Taking these various factors into account, the IMF stresses the need to reform the civil service, increase public investment, and improve the transparency of public finances by improving the quality of macro-fiscal forecasts, proposing a medium-term fiscal strategy, and including the social security fund budget in the annual budget legislation (IMF fiscal transparency evaluation, 2016).

The fight against corruption and the strengthening of legislative and security frameworks require additional efforts on the part of governments and the relevant authorities. Improving access to finance will also enable projects in Tunisia to run more smoothly, particularly those involving SMEs. In this context, the AfDB has approved a €60 million credit line for the BH, intended to strengthen the financing of activities of companies engaged in international trade. On this point, the literature on international trade highlights the importance of financing constraints in explaining the performance of exporters (Chaney, 2005; Manova, 2013).

Finally, reducing social inequalities and controlling unemployment would help send positive signals about Tunisia’s international situation, which would make it more attractive to foreign investment.

Conclusion

The increase in terrorist attacks in Tunisia in 2015 and poor economic growth largely explain the decline in FDI inflows to Tunisia.

The establishment of a new investment code and the « Tunisia 2020 » international investment conference are positive signals for attracting foreign investors once again.

Improving the business climate is also essential to ensure that this attractiveness is reinforced. This would involve, in particular, strengthening anti-corruption procedures, improving access to finance, and reforming the financial sector.

Bibliography:

– Acemoglu, D., & Robinson, J. A. (2015), « The rise and decline of general laws of capitalism, » The Journal of Economic Perspectives, 29(1), 3-28.

– Adair, P., & FHIMA, F. (2013). SME financing in Tunisia: dependence on banks and credit rationing. International SME Review, 26(3-4).

– Central Bank of Tunisia (BCT), 2017, https://www.bct.gov.tn/

– Barro, Robert J. (1997), “Determinants of Economic Growth: A Cross-Country Empirical Study”, Cambridge, Mass.: MIT Press, 1997.

– Chaney, T. (2016), “Liquidity constrained exporters,” Journal of Economic Dynamics and Control, 72, 141-154.

– Global Democracy Rankings Report, 2017, http://democracyranking.org/wordpress/

Hanousek, J., & Kochanova, A. (2015),“Bribery environment and firm performance: Evidence from central and eastern European countries”.

– IMF (2016),“Tunisia: Fiscal Transparency Evaluation,” IMF Country Report No. 16/339.

– IMF (2016),“Corruption: Costs and Mitigating Strategies,” Staff Discussion Note No. 16/05.

– Tunisian National Institute of Statistics INS (2017), www.ins.nat.tn/

– Lavallée, E. (2006), “Institutional similarity, institutional quality, and international trade,” International Economics, (4), 27-58.

– Manova, K. (2013), “Credit constraints, heterogeneous firms, and international trade,” The Review of Economic Studies, 80(2), 711-744.

– Mauro, P. (1995), « Corruption and growth, » The Quarterly Journal of Economics, 110(3), 681-712.

– Persson, T., & Tabellini, G. (2007), “The growth effect of democracy: Is it heterogeneous and how can it be estimated?”

– Schwab, K., Sala-i-Martin, X., Semans, R., & Blanke, J. (2014),“The Global Competitiveness Report 2014–2015”, Report of the World Economic Forum. ISBN 978-92-95044-98-2.

– Schwab, K & Sala i Martin, X., « The Global Competitiveness Report 2016-2017, « Report of the World Economic Forum, 09/2016. ISBN 978-1-944835-04-0.

– World Bank Group (2016),“Doing Business Economy Profile 2017: Tunisia”, World Bank, Washington, DC. © World Bank. https://openknowledge.worldbank.org/handle/10986/25654 License: CC BY 3.0 IGO.

[1] Other studies on the link between FDI and growth in Tunisia do not confirm the role of FDI in growth (see Belloumi, 2014).

[2] Despite the common belief that corruption negatively affects growth (Mauro, 1995), IMF SDN/16/05), other studies present mixed results (see Hanousek and Kochanova (2015)).

[3] For each aspect of the quality of the business environment detailed below, Tunisia’s position is considered out of 190 countries ranked from the highest performing (1) to the lowest performing (190).

[4]This indicator makes it possible to verify whether certain characteristics that facilitate lending exist in the applicable legal framework related to guarantees and insolvency. 0 indicates low quality guarantees and 12 indicates better quality.

[5] This indicator measures the rules and practices affecting the coverage, scope, and accessibility of credit information, with 0 indicating poor credit information.

[6] This is a panel of 1,275 Tunisian SMEs observed between 2001 and 2006.

[7] According to a 2015 study by CONECT (Confederation of Tunisian Citizen Enterprises), insufficient collateral is a barrier to access to finance for 68.8% of SMEs.

[8] In terms of time, paperwork, and cost.