Usefulness of the article : A recent pan-European study on the impact of public credit guarantees shows their positive microeconomic impact in terms of growth and a reduction in the number of bankruptcies. This impact is even more positive for companies facing credit constraints, which are most likely to be affected by an economic downturn. Evaluating such policies makes it possible to compare this impact between countries and programs.

Summary :

- Corporate credit guarantee policies have multiplied over the past 25 years.

- European credit guarantee programs are now, for the first time, enabling an international assessment of their impact in Europe.

- Supported businesses generally experience higher growth and fewer bankruptcies than comparable unsupported businesses.

- Further research is needed to assess more precisely the role of banks and financial institutions in the implementation of these programs.

Since the 1980s, business credit guarantee policies have spread throughout most developed countries and have been implemented at the regional, national, and European levels. Since 2008, in a context of crisis followed by growth in corporate debt in Europe, public actors have been striving to secure access to credit, in particular through credit guarantees financed by the European Union and implemented by the European Investment Fund, part of the European Investment Bank Group.

As part of the negotiations on the European Union’s next multiannual financial framework for the period 2021-2027, the question of renewing these guarantee programs has arisen. The European Investment Fund has therefore conducted a pan-European study in collaboration with university researchers on the impact of the European « MAP » (Multiannual Program for Enterprises) and « CIP » (Competitiveness and Innovation Program) credit guarantee programs for small and medium-sized enterprises (SMEs) between 2002 and 2016 (Brault and Signore 2019). The aim is to examine the impact of these programs in terms of business growth and survival, and to understand how it differs across countries and types of businesses.

Policies that are increasingly widespread but rarely evaluated

SMEs account for 99.8% of European businesses, 60% of their added value, and 70% of their employees. They also account for up to one-third of total outstanding loans in Europe (source: OECD). However, SMEs suffer from structural difficulties in accessing credit. This is particularly the case in regions experiencing overall difficulties in accessing credit, and among start-ups that do not have tangible collateral. As a result, they either do not obtain loans or obtain them on unfavorable terms. This situation is exacerbated when banks are under pressure to meet their capital ratios. In order to address this market inefficiency, credit guarantee mechanisms, which serve as a substitute for collateral, have been put in place in many developed and emerging countries over the past several decades, particularly in times of crisis or economic downturn. In particular, the European Union has set up a program of counter-guarantees for loan portfolios intended for financial intermediaries serving SMEs.

The European framework programs have been in place since 1998 and are renewed every five years. The programs that were evaluated, MAP and CIP, ran from 2002 to 2016. The program for the competitiveness of enterprises and SMEs (COSME), currently underway, expires in 2020. The credit guarantees in question are set up under the « Entrepreneurship and Innovation » section of these programs: these are counter-guarantees or co-guarantees granted to financial intermediaries, banks, or guarantee institutions. These counter-guarantees generally cover half of the guarantees offered to businesses by these financial intermediaries. The European Commission for Internal Market, Entrepreneurship, and SMEs coordinates these programs, which are implemented operationally by the European Investment Fund. These guarantees coexist with numerous national programs as well as other European guarantee programs such as InnovFin, the Employment and Social Innovation Program (EaSI), and the Guarantee Program for the Cultural and Creative Sectors (CGS).

The aim of European guarantees is to address market inefficiencies in access to bank financing for small and medium-sized enterprises with growth potential. In particular, the aim is to limit the risk associated with investments in the knowledge, technology, and innovation economy, based on the Lisbon objectives (CCUE, 2011). The aim of this policy is to promote growth, innovation, and employment by supporting companies that do not have sufficient collateral. Since 1998, more than €50 billion in loans have been guaranteed by the European Union. The beneficiary companies differ from country to country. They tend to be more mature in France and Italy, and smaller and younger in the Benelux countries.

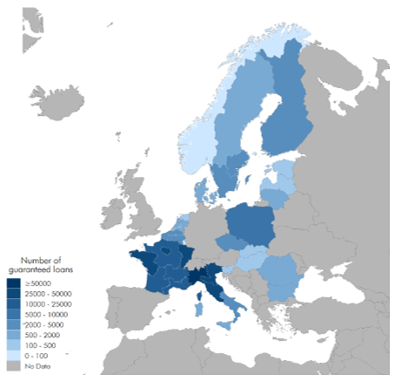

Figure 1: Loans guaranteed under the MAP and CIP programs in the countries covered by the study

Data: European Investment Fund. Note: CESEE = Central, Eastern, and Southeastern European countries.

An initial pan-European assessment

The upcoming end of the COSME program and ongoing discussions on the development of the future European multiannual financial framework by the new European administration have led the Commission to mandate the European Investment Fund to conduct a rigorous pan-European evaluation of the MAP and CIP programs in the area of credit guarantees. Collaboration with researchers from the Polytechnic University of Milan and EM Lyon ensured its independence. It has resulted in several articles (Bertoni, Colombo, and Quas 2018; Bertoni, Brault, Colombo, Quas, and Signore 2019). This evaluation concludes today with a pan-European summary article (Brault and Signore 2019).

This study compares the future of supported companies with that of comparable companies that did not receive guarantees[1]. The regions covered by the study are Benelux, France, Italy, the Nordic countries, and the countries of Central, Eastern, and Southeastern Europe. However, France and Italy account for the majority of the loans concerned. The methodology chosen is microeconomic, comparing the evolution of supported companies with comparable « twins.«

Map 1: Number of loans guaranteed under the MAP and CIP programs

(by region, for France, Italy, Benelux, Central and Eastern European countries, and Nordic countries)

Data: European Investment Fund

A policy that promotes business growth

The results of the study are generally positive. Guaranteed loans lead to growth in business assets (between 7% and 35% depending on the country), sales (between 6% and 35%), and employment (between 8% and 30%). Supported businesses are also between 4% and 5% less likely to go bankrupt. The share of intangible assets in total assets, a way of approximating the importance of innovation in businesses’ business models, increases by a third for businesses that have benefited from the guarantee. These results can be broken down by type of business. Guaranteed loans thus have more positive effects for small and young companies, which are more likely to experience credit restrictions. Similarly, service companies benefit more than industrial companies. Finally, the size of the loan plays a role, with the effect increasing with the size of the loan. However, this effect varies depending on the region concerned. It is most significant in the Benelux countries. Next come the Nordic countries, Central and Eastern European countries, Italy, and France. The characteristics of the industrial landscape, which vary greatly between European countries, explain some of these differences in impact, but also the ways in which these counter-guarantees have been implemented by financial intermediaries, a point to which we will return below.

The limitations of these programs are also apparent. Guaranteed loans have no significant impact on profitability, and the effect on productivity is ambivalent. In the short term, up to five years in Central and Eastern European countries, it is negative. This medium-term impact could be due to inefficiencies in the allocation of resources following the initial increase in production factors or to a period of adjustment following the granting of the loan. The long-term impact could not be assessed. However, it is positive in France in both the short and long term, between five and ten years after the loan is granted. This long-term effect is encouraging, as productivity growth is a long-term process. High-tech or knowledge-based sectors do not show a more significant impact of the policy. In this sense, generic credit guarantees such as MAP and CIP are probably not always the most appropriate tools for improving profitability and productivity or specifically supporting these sectors. Other guarantees that are more targeted at innovative companies, such as InnovFin, are better suited to these objectives. Other policies, such as venture capital investment or hybrid instruments combining equity and debt, could also be more effective in this area.

A call for more research on the role of banks and guarantee institutions

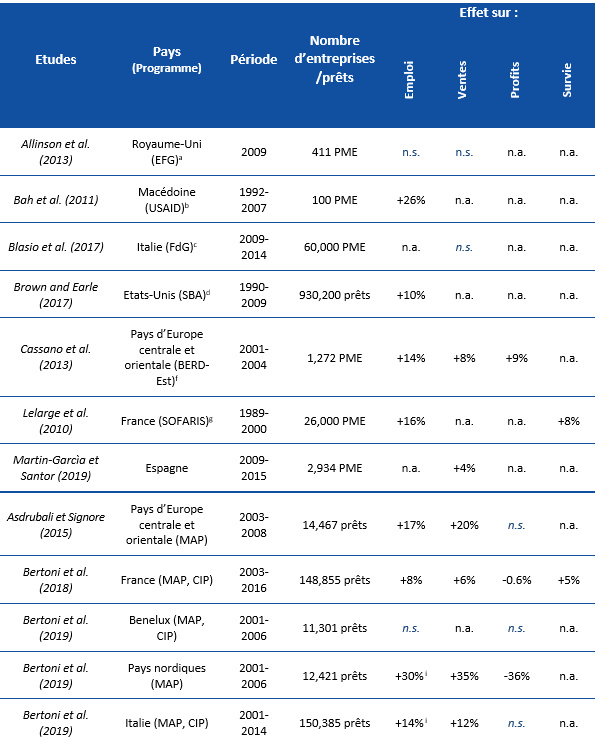

The evaluation broadens the scope of research on credit guarantee assessment and compares the impacts of these policies in different countries. We show that the effect of European programs on employment, turnover, and business survival is similar to that of other comparable programs around the world.

Table 1: Comparison of the effects of credit guarantee policies around the world (based on Brault and Signore, 2019).

Notes: See Brault and Signore (2019) for details of the evaluation methods. n.s.: no significant effect ![]() 0.05; n.a.: not available; a Enterprise Finance Guarantee Program of the British Business Bank; b SMEs supported by the United States Agency for International Development; c Credit guarantees allocated by the Fondo di Garanzia; d Loans supported by the Small Business Administration; f SMEs supported by the EBRD in Bulgaria, Georgia, Russia, and Ukraine; g Credit guarantees from the SOFARIS program;h Loansguaranteed by Avalmadrid

0.05; n.a.: not available; a Enterprise Finance Guarantee Program of the British Business Bank; b SMEs supported by the United States Agency for International Development; c Credit guarantees allocated by the Fondo di Garanzia; d Loans supported by the Small Business Administration; f SMEs supported by the EBRD in Bulgaria, Georgia, Russia, and Ukraine; g Credit guarantees from the SOFARIS program;h Loansguaranteed by Avalmadrid

Another explanation for the differences in impact between countries probably relates to financial intermediaries, i.e., banks and credit institutions that make loans counter-guaranteed by the European Investment Fund. It would therefore be interesting to study in greater depth the differences between these institutions in terms of the implementation of these policies, the specific clientele of these banks and credit institutions, and loan allocation procedures. Similarly, the reasons for the partially negative effects of these policies on profits need to be explored in greater depth, in particular to determine whether there are conditions under which the impact would be positive. The reasons for the negative effects on productivity should also be explored in greater detail. Indeed, the J-curve theory predicts limited or negative returns following an initial investment. In a second stage, productivity improves. Finally, in a third stage, profitability increases, allowing the initial investment to be repaid. This hypothesis has been verified in the case of France, the only country studied over a period of more than five years. In the future, this long-term perspective should be extended to other countries. Finally, it would be interesting to assess the impact of these policies on the interest rates offered by banks.

Conclusion

The expansion of credit guarantee programs in Europe and around the world therefore calls for more evaluations of these policies. The pan-European study presented here provides a better understanding of the impacts of these policies and allows for comparisons between countries and programs. The microeconomic impact is broadly positive in terms of growth and a reduction in the number of bankruptcies, especially for companies facing credit restrictions, which are most likely to be affected by an economic downturn. Monitoring the long-term financial sustainability of these programs is therefore essential. Differences between countries also call for a more in-depth future assessment of the role of financial intermediaries. The study cited (Brault and Signore 2019) sheds light on the delicate trade-off between the growth policy objectives promoted by institutions and the many differences that affect their impact on the ground.

Bibliography

Allinson, G. F., Robson P., Stone, I. (2013). Economic Evaluation of the Enterprise Finance Guarantee (EFG) Scheme. Department for Business, Innovation and Skills Project Report.

Ashenfelter, O. (1978). Estimating the Effect of Training Programs on Earnings. The Review of Economics and Statistics, 60, 1. pp. 47-57.

Asdrubali, P. and Signore, S. (2015). The Economic Impact of EU Guarantees on Credit to SMEs. Evidence from CESEE countries. European Commission’s European Economy Discussion Paper 002 and EIF Working Paper 2015/29. July 2015. http://ec.europa.eu/economy_finance/publications/eedp/pdf/dp002_en.pdf, and http://www.eif.org/news_centre/publications/eif_wp_29_economic-impactguarantees_july15_fv.pdf

Bah, E., Brada, J.C., Yigit, T. (2011). With a little help from our friends: The effect of USAID assistance on SME growth in a transition economy. Journal of Comparative Economics 39, 205–220.

Beck, T., Klapper, L. F., & Mendoza, J. C. (2010). The typology of partial credit guarantee funds around the world. Journal of Financial Stability, 6(1), 10–25. https://doi.org/10.1016/j.jfs.2008.12.003

Bertoni, F., Colombo, M. G., & Quas, A. (2018). The effects of EU-funded guarantee instruments on the performance of Small and Medium Enterprises: Evidence from France. EIF Working Paper 2018/52, EIF Research & Market Analysis. November 2018. http://www.eif.org/news_centre/publications/EIF_Working_Paper_2019_52.htm

Bertoni, F., Brault, J., Colombo, M. G., Quas, A., and (2019). Econometric study on the impact of EU loan guarantee financial instruments on growth and jobs of SMEs. EIF Working Paper 2019/54, EIF Research & Market Analysis. February 2019.

http://www.eif.org/news_centre/publications/EIF_Working_Paper_2019_54.htm

Brault, J., and Signore, S. (2019). The real effects of EU loan guarantee schemes for SMEs: A pan-European assessment. EIF Working Paper 2019/56, EIF Research & Market Analysis. June 2019. http://www.eif.org/news_centre/publications/EIF_Working_Paper_2019_56.htm

Brown, J. D., Earle, J. S. (2017). Finance and Growth at the Firm Level: Evidence from SBA Loans. Journal of Finance, 72(3), 1039–1080.

Cassano, F., Jõeveer, K., Svejnar, J. (2013). Cash flow vs. collateral-based credit. Economics of Transition, Vol. 21, pp. 269–300.

Chatzouz, M., Gereben, A., Lang, F., and Torfs, W. (2017). Credit Guarantee Schemes for SME lending in Western Europe. EIB Working Paper 2017/02 and EIF Working Paper 2017/42. http://www.eif.org/news_centre/publications/EIF_Working_Paper_2017_42.htm

European Court of Auditors (2011). The Audit of the SME Guarantee Facility.

Lelarge, C., Sraer, D., Thesmar, D. (2010). Entrepreneurship and credit constraints: Evidence from a French loan guarantee program. In: Lerner, J., and Schoar, A., International Differences in Entrepreneurship.

Martin-Garcìa, R., Morán Santor, J., (2019). Public guarantees: a countercyclical instrument for SME growth. Evidence from the Spanish Region of Madrid. Small Business Economics. Manuscript submitted for publication.

OECD (2013). SME and Entrepreneurship Financing: The Role of Credit Guarantee Schemes and Mutual Guarantee Societies in supporting finance for small and medium-sized enterprises (Final Report).

OECD (2019). Financing SMEs and Entrepreneurs 2019. An OECD Scoreboard.

Rosenbaum, P. R., Rubin, D. BN. (1983). The central role of propensity score in observational studies for causal effects. Biometrika, 70(1), 41–55.

Riding, A. L., and Haines, G. (2001). Loan guarantees: Costs of default and benefits to small firms. Journal of Business Venturing, 16(6), 595–612. https://doi.org/10.1016/S0883-9026(00)00050-1

[1]To do so, it uses a sample representing 60% of the guarantees granted by these programs, supporting more than $22 billion in loans in 19 countries.

[2]According to the Rubin model, combining propensity score matching (Rosenbaum and Rubin, 1983) and difference-in-differences (Ashenfelter, 1978). The study uses data from the European Investment Fund, cross-referenced with two Bureau Van Dijk databases, Orbis and Diane, containing data, particularly financial data, on numerous companies. The constraints and limitations associated with these databases are explained in the articles cited.

[3]Detailed breakdowns can be found in the full study (Brault and Signore 2019).