DISCLAIMER: The opinions expressed by the author are personal and do not reflect those of the institution that employs him.

Usefulness: This article examines the reasons for and consequences of the recent change in monetary policy by the Fed against a backdrop of dynamic economic growth and concerns about liquidity. While keeping rates at their current level appears to mark the end of a cycle of easing, the Fed’s stance remains accommodative.

Summary:

- After three cuts in its key interest rates between July and October 2019, the US Federal Reserve (Fed) decided to leave them unchanged since December 2019.

- While this decision marks the end of a (short) cycle of monetary easing, it does not necessarily mean a return to tightening in the short term.

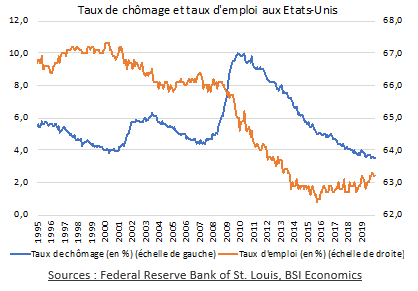

- Economic growth in the United States remains very strong, bringing the unemployment rate to its lowest level in 50 years, even though the employment rate is still well below its pre-crisis level.

- The pressure on bank liquidity, which had caused concern in September 2019 and led the institution to inject tens of billions of dollars into the markets, appears to have eased. However, the Fed remains attentive to developments and risks, particularly geopolitical risks, weighing on the markets.

At the meeting of the US Federal Reserve’s monetary policy committee on December 11, 2019, the Board of Governors decided to keep key interest rates unchanged[1], marking a pause in the cycle of monetary easing that began in the summer of 2019. The Fed confirmed this stance at its first meeting of 2020 on January 29. While the US economy is entering its eleventh consecutive year of expansion and unemployment is at a historic low, inflation, which averaged 1.4% year-on-year in 2019, is struggling to reach the institution’s target (2%), and liquidity pressures emerged in the interbank market in the fall of 2019. The US central bank’s monetary policy is thus faced with the dilemma of supporting the economy while preparing for a possible recession by preserving its room for maneuver.

1. After three consecutive increases in its key interest rates, the US Federal Reserve suspends its cycle of monetary easing

a) A decision consistent with the US economic outlook

In terms of monetary policy, 2020 is starting very differently from 2019 in the United States. A year earlier, the US Federal Reserve had raised its key interest rates by 25 basis points, to between 2.25% and 2.50%, for the last time in the monetary tightening cycle that began in late 2015, in response to inflation that was still above its 2% target. It then reversed the trend by cutting key interest rates three times, by 25 basis points each time, between July and October 2019. Despite strong economic activity (2.5% annualized quarterly growth in the first half of 2019), which contributed to a very low unemployment rate (3.7% in June), inflation had once again fallen below the 2% threshold. Beyond this observation, US central bankers were also concerned about rising trade tensions between the United States and its trading partners, particularly China, and the consequences for investment and exports.

Three rate cuts later, with the markets expecting a further cut, the Fed decided to pause on December 11, 2019, keeping the key rate between 1.50% and 1.75%. The reasons given for this decision were the strong growth, with a stable rate of around 2% on an annualized quarterly basis in the third quarter, and a still very dynamic labor market, characterized by an unemployment rate that had fallen to 3.5%, its lowest level in 50 years.

Nevertheless, this decision may have come as a surprise, given that it comes at a time of low inflation. Inflation rates are down compared to last year and below the monetary institution’s target, suggesting that policy is still too restrictive. The inflation index monitored by the US Federal Reserve, personal consumption expenditures (PCE), rose by 1.3% year-on-year in October 2019, while the underlying index (excluding food and energy prices) grew by 1.6%, both well below the institution’s target.

Despite the acceleration in job creation, wage growth remains moderate (average hourly earnings per private sector employee up 2.9% year-on-year in December 2019), which limits the increase in costs to be absorbed by businesses and therefore does not point to an overheating labor market. One explanation for this may be the employment rate, which has been rising gradually since the mid-2010s but has not yet returned to its pre-2008 crisis level: it is three percentage points lower, indicating that many Americans have not returned to the labor market and still represent a labor reserve for US companies. Thus, the presence of this potential labor supply mitigates the effects of the decline in the unemployment rate on wage growth and, therefore, on prices.

Although the deterioration in the global economic situation weighed on the US economy in 2019, the Federal Reserve saw the easing of trade tensions as the beginning of an easing of concerns weighing on investment and exports. Trade tensions between the United States and China appear to be moving towards a positive outcome, with the signing of the first phase of an agreement on January 15, 2020. The risk of the United Kingdom leaving the European Union without a trade agreement has been temporarily averted, and global growth no longer appears to pose a risk of negatively impacting US growth.

The Federal Reserve’s decision to keep key interest rates unchanged can be understood in light of its desire to continue supporting growth and, symmetrically, the labor market, without weighing on inflation, which is approaching the 2% target.

b) Close monitoring of the effects of monetary policy on financial markets

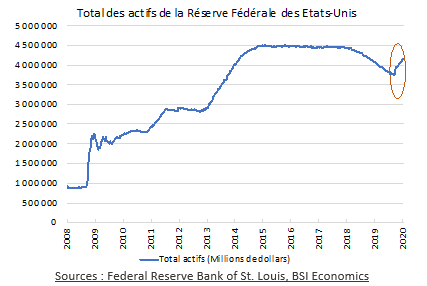

In October 2017, the Federal Reserve began a process of normalizing its balance sheet. Nearly 10 years after the start of the crisis and, consequently, its asset purchase program designed to provide liquidity in sclerotic financial markets, it began to significantly reduce its balance sheet, which stood at more than $4.4 trillion compared to $900 billion in mid-2008. However, in September 2019, liquidity tensions emerged: the sharp rise in the secured overnight refinancing rate well above the Federal Reserve’s key rates, between which it usually fluctuates, generated serious concerns about the financing capacity of US banking institutions.

The reasons for this episode of stress can be found in the liquidity held by US banks, as explained by Benoît Cœuré[2]. Whereas in the past high levels of liquidity reflected uncertainty or a malfunctioning money market, they are now seen as a means of guaranteeing the short-term interest rate desired by the monetary authorities. However, two factors explain why the current level of liquidity does not ensure that this interest rate remains stable. First, liquidity is unevenly distributed among US banks: 86% of excess reserves are held by 1% of banks, with four banks alone holding 40%. Liquidity conditions are therefore dependent on the willingness of these banks to meet the needs of other financial intermediaries. On the other hand, financial intermediaries without access to central bank financing have seen their role grow since the crisis. The inability of some financial players to obtain financing from the central bank has an impact on the supply of available liquidity, making it less elastic, and thus also explains some of the tensions. These two aspects therefore make the transmission of monetary policy more complex. Although the accommodative monetary policy pursued in recent years has provided banks with very high levels of liquidity, these shortcomings mean that they may occasionally prove insufficient in the event of sudden pressures on the supply of liquidity.

To alleviate these tensions, the Federal Reserve took emergency action by injecting tens of billions of dollars, triggering a rebound in the monetary institution’s balance sheet. On the one hand, it announced a resumption of purchases of short-term US bonds worth $60 billion per month, which it will continue until the second quarter of 2020 at the earliest, and on the other hand, it initiated refinancing operations (overnight repurchase agreements and term repurchase agreements), at least until April 2020. These exceptional measures reflect the central bank’s desire to maintain a stable level of bank reserves, if not higher than that prevailing in September. The aim is to ensure that banks are able to absorb an economic shock and avoid the risk of a liquidity shock. While the Fed’s responsiveness in September 2019 was reassuring, the sudden and unexpected onset of such tension raises the question of the need for standardized monetary interventions, as was the case before the 2008 crisis.

Since then, repo operations have gradually decreased in scale, reducing pressure on liquidity in the interbank market. Short-term financing conditions have stabilized, limiting the need for intervention by the central bank.

2. What consequences can we expect from this decision?

a) The end of the monetary easing cycle does not necessarily mark the beginning of a tightening cycle

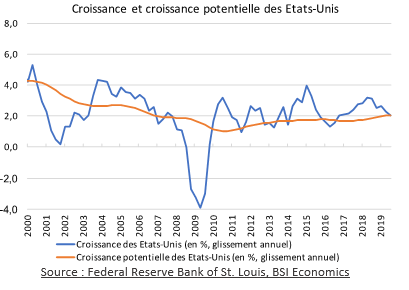

Although GDP growth rates are tending to decline, they nevertheless demonstrate the strong momentum of the US economy (which is outperforming the eurozone and Japan). Economic activity shows no signs of slowing down, and the employment rate should continue to rise, benefiting the middle classes, whose wealth has only recently returned to its pre-crisis level, mainly due to the decline in the share of wages in value added.

Real wage growth is in line with productivity growth[6] and economic growth is close to its potential, at around 2% year-on-year, which does not signal any risk of a significant increase in inflation. The economic outlook therefore does not call for monetary policy tightening. From the perspective of financial markets, excessive tightening would increase liquidity risks and could lead to a downward correction in financial asset prices.

Nevertheless, it is unlikely that the Federal Reserve will opt for further easing in the short term. The minutes released following the Federal Reserve’s last meeting in December 2019 indicate that 13 of the 17 members of the Board of Governors anticipate that the key interest rate will remain stable throughout 2020, before modest increases in subsequent years.

b) Which economies will benefit from this monetary policy?

As Fischer explained in 2015[7], all economies integrated into the global economic system are affected by the Fed’s decision. At the start of the previous monetary tightening in 2015, much attention was paid to the reaction of emerging markets, which were considered to be beneficiaries of the US’s accommodative monetary policy after the Great Recession and therefore sensitive to the risk of foreign capital flowing back to developed economies when US interest rates rise. Conversely, monetary easing by the world’s leading economic power creates conditions conducive to risk-taking by making foreign assets more attractive.

By keeping interest rates low, the US central bank creates an environment that encourages asset price increases, attracts capital flows from abroad and, as a result, global growth by allowing the world’s largest economy to finance itself at low rates. Under these conditions, emerging economies benefit from relatively more attractive assets, particularly their currencies, which automatically makes their foreign currency-denominated debt less expensive and reduces imported inflation. Controlled inflation in turn allows them to lower their own key interest rates in order to support domestic growth (this is currently the case in Brazil and Russia, for example). On the other hand, for other economies, such as the eurozone and Switzerland, monetary policy cycles have become decoupled since the crisis and their already negative rates cannot follow the Federal Reserve’s rate changes. It is therefore unlikely that their monetary policy will be impacted by that of the Fed.

Nevertheless, the markets will remain attentive to developments in various types of tensions, both in the United States and elsewhere. A deterioration in trade relations or geopolitical tensions could wipe out the gains made thanks to US monetary policy.

Conclusion

The recent decision by the US Federal Reserve Board of Governors to keep its key rates unchanged after three successive cuts is consistent with economic conditions, despite modest inflation. From the perspective of the financial markets, it reflects an easing of liquidity tensions. However, it does not necessarily herald a future tightening of monetary policy. As long as inflationary pressures remain absent, the status quo is likely to persist.

The Federal Reserve nevertheless insists that it may adjust its position in the event of significant changes in the economic environment, particularly with regard to international issues. The prospect of an easing in the trade war between the United States and China has improved monetary conditions, but the absence of a trade agreement between the United Kingdom and the European Union, escalating social tensions in Hong Kong and Latin America, and developments in the campaign for the November 2020 presidential elections could reverse this trend. This decision illustrates the decision-making policy used by Chairman Powell, which favors data analysis and adjustments based on short-term prospects, and may signal the end of the vision of monetary policy through successive long cycles of tightening and easing.

[1]Minutes of the Federal Open Market Committee, December 10–11, 2019

[2]Cœuré, B. (November 12, 2019). A tale of two money markets: fragmentation or concentration

[3]Federal Reserve of New York, October 11, 2019 https://www.newyorkfed.org/markets/opolicy/operating_policy_191011

[4]Federal Reserve, Press release, January 29, 2020

[5] This was the case during the Great Recession of 2008, which contributed to the amplification of the crisis by disrupting the functioning of financial markets and the economy.

[6]Clarida, R. H. (January 9, 2020). US economic outlook and monetary policy Speech, C. Peter McColough Series on International Economics, Council on Foreign Relations, New York City

[7]« And of course, actions taken by the Federal Reserve influence economic conditions abroad. Because these international effects in turn spill back on the evolution of the U.S. economy, we cannot make sensible monetary policy choices without taking them into account. » Fischer , S . ( May 26, 2015). The Federal Reserve and the Global Economy