Abstract:

· Private equity aims to provide equity financing to SMEs and mid-cap companies, which are generally unlisted, by acquiring majority or minority stakes in these companies.

· This activity is an essential link in the equity financing of unlisted French companies: holdings managed by private equity funds represent around 6-8% of the capital of unlisted companies[1];

· After several difficult years, the private equity market has now returned to fundraising levels close to those seen before the crisis. This momentum can be explained in particular by the return of foreign investors, in a context where public support has also been growing for several years.

· Public intervention could lead to a risk of dependence on the most upstream segments of private equity.

Private equity activity aims to provide equity financing to SMEs and mid-cap companies, which are generally unlisted, by acquiring majority or minority stakes in the capital of these companies. This activity is an essential link in the equity financing of unlisted companies.

The origin of the funds flowing into each of the different segments (venture capital, growth capital, buyout capital, and turnaround capital) varies considerably: private institutional investors are structurally more present in the downstream segments (growth capital, buyout capital, turnaround capital), while public interventions account for a very significant share of funds in the upstream segments (seed capital, venture capital, « small » growth capital). After several difficult years, the private equity market has now returned to fundraising levels close to those seen before the crisis.

1. France is now thesecond-largest private equity market in Europe

1.1. Private equity business segments

Private equity activity aims to provide equity financing[2] to SMEs or mid-cap companies, which are generally unlisted, by acquiring majority or minority stakes in the capital of these companies. This activity is in fact quite different (and therefore relatively segmented) depending on the « maturity » of the companies invested in.

Around 1,650 companies received financing from members of the AFIC (Association Française des Investisseurs pour la Croissance) in 2015, placing France second in the world in terms of the number of companies financed (5,000 in the United States, 1,300 in Germany, 900 in the United Kingdom, 200 in Italy and Spain). In addition, the French private equity market has grown tenfold since the mid-1990s, from €876 million invested in 1996 to €10.7 billion in 2015 (AFIC figures).

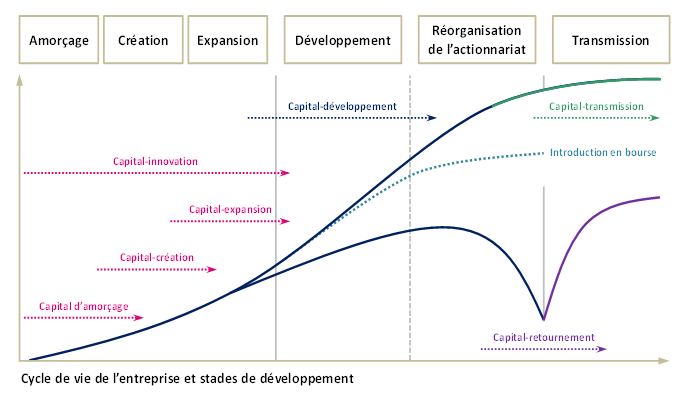

Private equity can be broken down into several types of activity corresponding to different stages in the life of a company. According to AFIC terminology, a distinction is made between (see Fig. 1):

· innovation capital: financing for companies that are being created or in the early stages of development;

· development capital: financing for companies that have reached profitability and are generating profits. The funds are used to increase production capacity, sales force, develop new products and services, conquer new international markets, etc.;

· Leverage buy-out (LBO): acquisition of existing companies by a team of financial investors and managers from within or outside the company through the use of leverage;

· turnaround capital: financing of companies in difficulty.

Figure 1: Segmentation of private equity activity

during a company’s life cycle

Source: AFIC

It should be noted that, in each of these segments, fund managers very often play a decision-making role in the companies in which they invest, through their presence in governance bodies, and thus participate fully in the strategic development choices made by the companies. The importance of private equity therefore goes beyond the mere provision of funds; the quality of support is also an essential aspect of the added value of this activity.

1.2. Private equity financing players in France

Private equity involves a variety of investors in the capital of unlisted companies:

· Institutional investors: banks, insurance companies, and pension funds acting through dedicated vehicles such as Professional Private Equity Funds (FPCI);

· private investors grouped together in family offices[3];

· individuals grouped together in tax funds such as FIPs (local investment funds) and FCPIs (innovation mutual funds), which offer income or wealth tax reductions;

· Corporate investors (large companies): however, this type of investor remains in the minority in France; French and foreign public entities: Bpifrance, foreign sovereign wealth funds, etc.

1.3. The development of private equity in France

This activity emerged in the early 1950s in the United States. Its development in France is more recent: there has been a significant increase in funds raised and investments made during the 2000s (see graphs 1 and 4). At the end of the 2000s, on the eve of the crisis, the private equity market in France had become the second largest in Europe behind the United Kingdom.

While the number of companies targeted and the volumes invested may seem low, particularly in relation to the number of SMEs, it provides particular support to the knowledge economy and sectors of the future (IT, biotechnology, telecommunications, green technologies), on which the future competitiveness of the French economy depends. Thus, 40% of the companies financed in 2014, mainly through innovation capital, belonged to these sectors. Industry and chemicals, which remain major economic drivers, alone account for nearly 20% of the total amount invested over the last 10 years.

2. Fundraising in line with investments made

2.1. Fundraising trends

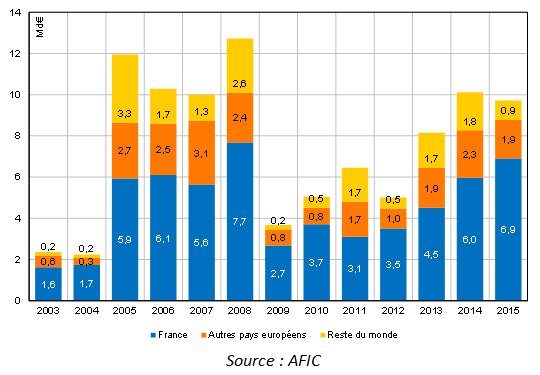

Funds managed by French private equity firms that are members of AFIC raised €10.7 billion in 2015, confirming the upturn in activity seen since 2013 (€8.7 billion in 2014; €6.5 billion in 2013; €6.1 billion in 2012). This level, which is significantly higher than the amounts raised in 2009 and 2010, is in line with the pre-crisis levels of around €10 billion, which may nevertheless have been affected by a « bubble » effect (Figure 1).

The rebound in fundraising observed since 2013 is mainly due to the return of large-scale fundraising: €5.7 billion was raised on average over the two years by vehicles larger than €200 million, compared with €1.3 billion in 2012.

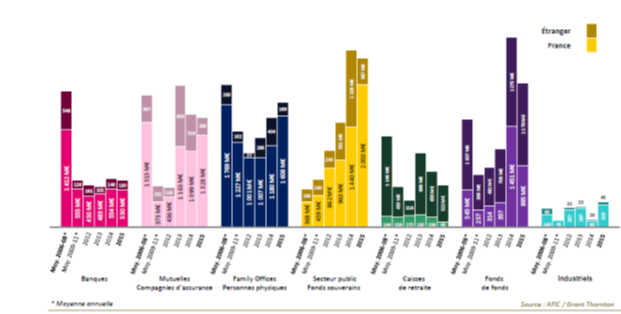

It should be noted that funds of funds and the public sector appear to have been the main drivers of the recent rebound in fundraising (Figure 2).

Graph 1: Fundraising by French management companies by geographical origin…

Source: AFIC

Chart 2: …and by main types of subscribers (annual average)

Source: AFIC

2.2. Investment trends

Across all geographic origins, approximately 1,650 companies received financing from French private equity operators in 2015, with new investments totaling €10.7 billion (see Chart 3). The number of companies supported has remained stable overall since 2006. Across all segments, this makes France theleading European market in terms of the number of companies supported.

Graph 3: Investments made by French private equity fund management companies

Source: AFIC

Over the past two years, investment levels have risen significantly (+65% compared to 2013) and are now back to pre-crisis levels (more than €10 billion in annual investment).

Over the past two years, the recovery has been particularly noticeable in growth capital transactions (+88% compared to 2013) and buyout capital transactions (+56% over one year), while in the innovation capital segment, with €758 million invested in 499 companies, activity has been less dynamic (+18% compared to 2013). However, over the long term, the amounts invested in innovation capital have remained relatively stable at around €600 million invested in 400 companies. On the other hand, in terms of amount and number of companies, support for companies already in the portfolio (reinvestments) is high. In 2015, nearly 50% of investments were reinvestments.

From a geographical perspective, of all the investments made by French private equity players, investments made in France represent €7.1 billion (nearly 85% of the total, see graph 4) invested in nearly 1,645 companies in 2015 (for the record, in 2012 there were 136,444 SMEs excluding micro-enterprises and 5,012 mid-sized companies in France)[5].

2.3. Forecasts for the allocation of funds raised

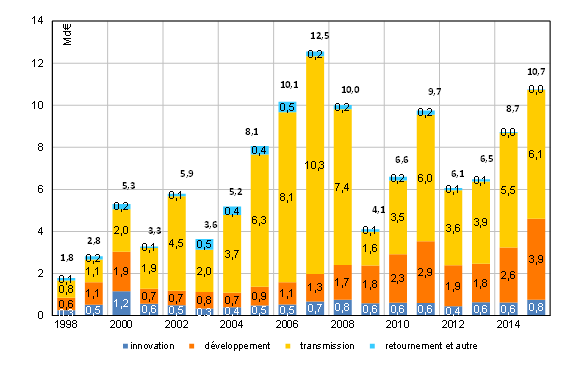

Most of the funds are raised for capital development operations (€5.0 billion in 2015 – see graph 4). The recovery in fundraising in this segment (+45%) is tempered by the decline observed in the buyout segment (down 41% to €3.3 billion in 2015), resulting in an overall stabilization of fundraising (€9.7 billion in 2015 after €10.1 billion in 2014). After a decline in 2014 (-40%), funds earmarked for venture capital rose again (+67% allocation intentions to €1.4 billion in 2015), returning to the level seen in 2013.

Figure 4: Fundraising by business segment

2.4. Public intervention could lead to a risk of dependence in the upstream segments of private equity

Although they declined over 2014 as a whole, funds earmarked for venture capital have risen sharply in recent years (+83% in planned allocations of funds raised at the end of 2014 compared with 2011[6]) (see Figure 5).

On the retail investor side, the number of subscribers to FIPs and FCPIs declined steadily between 2008 and 2012, and the funds raised by these vehicles fell, mainly due to changes in taxation (reduction in tax relief, reform of the ISF wealth tax, overall cap on tax breaks).

However, over the past two years, there has been a recovery in the number of subscribers and the amounts raised, possibly linked to changes in the number of taxpayers subject to the ISF. Funds raised averaged €723 million over the last two years, compared with €628 million in 2012 and €1.1 billion in 2008, involving 97,000 subscribers in 2014, compared with 83,000 in 2012 and 145,000 in 2008.

The increase in subscriptions from public entities, which contribute significantly to venture capital and development capital investments, has risen significantly since 2009. This is particularly true of French public entities, whose subscriptions rose from €230 million in 2009 to €2.05 billion in 2015.

More specifically, the last two years have stood out from the 2009-2013 period due to the strong growth of funds of funds and public sector entities (both French and foreign, including sovereign wealth funds) in the total funds raised by French private equity. both of which ranked first among capital providers to the asset class in 2015, accounting for nearly 20% of total fundraising. This coincides with the rise of various mechanisms (FNA, MultiCap Croissance funds, funds of funds subscribed by Bpifrance Participations), of which Bpifrance, via Bpifrance Investissement, is the main operator.

Thanks to this financing structure, French private equity has one of the highest domestic market coverage rates[7] in the world: approximately 0.9% of French companies with more than 10 employees are financed by French private equity players. This domestic market coverage ratio was comparatively 0.6% in the United States, 0.4% in the United Kingdom, and 0.3% in Germany (see Box 2).

Conclusion

In conclusion, venture capital financing in France and Europe has been showing signs of recovery since 2013 after a difficult period following the 2008 crisis.

Nevertheless, the need to revitalize venture capital to address the weakness of equity investments in young and innovative companies remains an important challenge. European companies may still encounter difficulties in obtaining capital financing, particularly in the most mature markets, in the later stages of venture capital, where unit financing needs are greater[8]. A forthcoming study will attempt to explain in greater detail the issues related to private equity activity.

Box Trends in the French and European private equity markets: some points of comparison

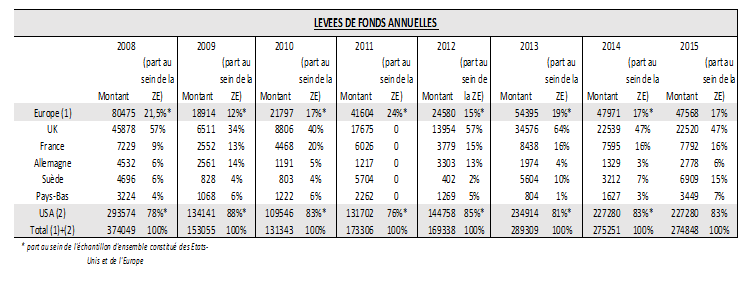

Across the eurozone, EVCA data showed a sharp decline in private equity fundraising after the 2008 crisis. In 2008, new private equity funds raised nearly €80 billion per year, half of which was raised in the United Kingdom and around 10% in France. These amounts subsequently fell sharply in the eurozone (-86% year-on-year in 2009) and in the United States, but to a lesser extent in France (-67%). After hitting a low point in 2009, fundraising gradually recovered in Europe, while remaining overall below its pre-crisis level in 2014 (nearly €45 billion).

Table : Change in annual fundraising in the private equity sector (in millions of euros, sources: EVCA, NVCA)

Three leaders stand out in the European private equity market: France, Germany, and the United Kingdom. Compared to the other two markets, France appears to have shown greater resilience during the crisis: at the end of 2013, funds raised remained above their pre-crisis level (+10% compared to 2007), unlike the United Kingdom (-33%) and Germany (-74%). Furthermore, although the decline in activity was less severe overall in the United States (54% contraction in 2009), it had still not returned to its 2008 level by the end of 2014.

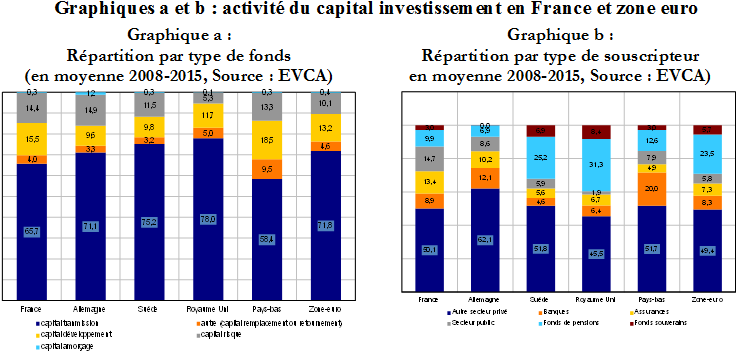

This stronger performance in France can be explained in particular by the increased involvement of public and industrial players, which helped to limit the sharp decline in activity by other players (notably banks, insurance companies, and pension funds). It should be noted that in other eurozone countries, the type of investor present in the private equity market is not the same as in France: in the United Kingdom and Sweden, pension funds (and to a lesser extent sovereign wealth funds) play an important role, while in Germany, activity seems to be more closely linked to that of banks (charts a and b).

[1] Source: Report on the financing of growing SMEs and mid-cap companies, October 2015, Business Financing Observatory

[2] Equity financing is the most appropriate form of financing for growth operations and risk-taking. It can take two forms:

– « Internal » financing, which allows for an increase in equity capital through the allocation of profits to reserves;

– « external » financing through an opening of the capital, most often involving either market investors or private equity players.

[3] A family office is an organization of individuals serving one or more families, offering advice to families exclusively in the interests of their assets. A family office therefore aims to preserve family cohesion with a long-term, transgenerational vision.

[4] INSEE counts 136,444 SMEs (including financial and insurance activities). Source: « Les entreprises en 2015 » (Businesses in 2015), INSEE

[5]Source: « Les entreprises en France » (Businesses in France), 2015 edition

[6]It should be noted, however, that this contrasts with the actual investment volumes (see 3) in this segment, which remained relatively stable over the period. There is, however, a potential time lag of several years between the moment when funds are raised and when they are actually invested.

[7]The national market coverage rate is the ratio between the number of national companies financed by national private equity players of all sizes and the number of companies with 10 or more employees in the national economy. Sources: OECD, NVCA, PEBCC, BVK, BVCA, AFIC)

[8] Source: Web Investors Forum, France Digitale, 2014 Study conducted for the European Commission, « Boosting digital startup financing in Europe, » as part of the Startup Europe initiative.