Poor Countries and Tax Pressure (Part 2)

The Performance and Objectives of Tax Pressure inLow-IncomeCountries

Summary:

· Over the past ten years, Sub-Saharan Africa (SSA) has seen real improvements in terms of tax burden, as its increase in domestic resources has been one of the largest in the world.

· This performance can be explained in part by better management of direct taxes (on income, wealth, and corporate profits) and indirect taxes (VAT and other sales taxes) in a context of increasing trade integration leading to a decline in customs revenues.

· Nevertheless, tax evasion, corruption, and the lack of resources of the tax administrations in some countries continue to have a negative impact on the amounts collected. In response, initiatives aimed at increasing the physical and human capacities of these administrations and strengthening international tax cooperation have recently been launched and should enable low-income countries, particularly those in SSA, to move closer to their tax frontier in the medium term.

For nearly 50 years, it has been recognized that taxation and the ability to collect domestic resources are important levers for promoting economic and social development. In a previous article, the identification of economic, social, and political determinants provided an understanding of the foundations of tax pressure in sub-Saharan Africa. It is now necessary to examine the performance and objectives of tax pressure in this region in order to establish a baseline and see what objectives sub-Saharan African countries are setting for themselves.

Tax Performance in Sub-Saharan Africa

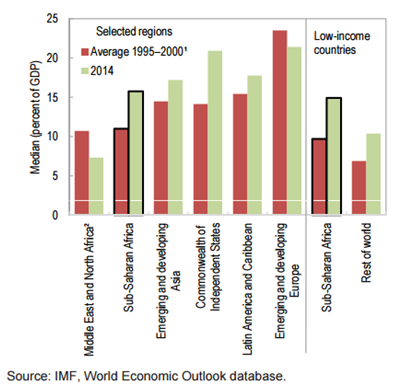

Historically, sub-Saharan African (SSA) countries have (on average) always had lower tax rates than low-income countries in other regions of the world. This trend continued throughout the 1990s and 2000s. But today, although it still has one of the lowest average tax rates in the world, the region has seen the most significant increase since 2000, particularly among the poorest countries (see Figure 1 below). This improvement partly reflects a catch-up effect, with SSA countries starting from lower tax levels and having greater room for maneuver to progress at a faster pace. Nevertheless, the fact that, at a similar level of development (among low-income countries), sub-Saharan Africa has also recorded greater growth in its domestic resources reflects a significant fiscal effort by African authorities to mobilize their domestic resources.

Figure 1: Regional comparisons of tax revenues among developing countries

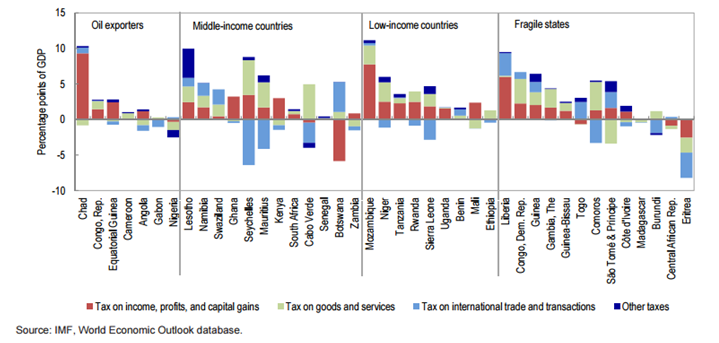

It would nevertheless be tempting to think that the increase in domestic resources within the region is due to the inflationary surge in commodity prices in the 2000s (and early 2010s), which would have inflated the domestic revenues of countries exporting these resources. However, Figure 2 below shows that while oil-exporting countries have indeed seen an increase in their tax revenues over the last decade (particularly Chad), this increase does not appear to be greater (on average) than that observed in non-oil-exporting countries (even though the price increase has spread to other commodities). Furthermore, revenues from the exploitation of natural resources most often take the form of royalties or exploitation rights and are therefore not counted as tax revenues in the strict sense of the term (taxes). Nevertheless, while the rise in the price of these resources does not seem to directly explain the total increase in revenue, it is possible that the increase in these prices has boosted the profits of companies operating in this sector, ultimately contributing to an increase in the amount of revenue collected on their profits and on the income of the people working there (even though these sectors are capital-intensive and therefore unlikely to inflate the average national income).

Figure 2 also shows that a large part of the gains in tax revenues come from significant improvements in income, profit, and capital gains taxation. The increase in indirect taxation on goods and services also appears to have contributed to raising the level of domestic resources in SSA countries, all of which now have a value added tax (although the complexity of the systems varies greatly from one country to another).

Figure 2: Sub-Saharan Africa: change in tax revenues

Average for 2000-04 and 2011-14

These improvements are the result of greater fiscal efforts by African states over the past decade. The concept of fiscal effort reflects the willingness of the authorities responsible for collecting taxes or non-tax resources to collect what their economy generates in terms of revenue. In other words, optimal fiscal effort means that these authorities succeed in collecting all available taxes within the country, given the current economic performance and institutional framework. In other words, the state manages to reach its fiscal frontier.

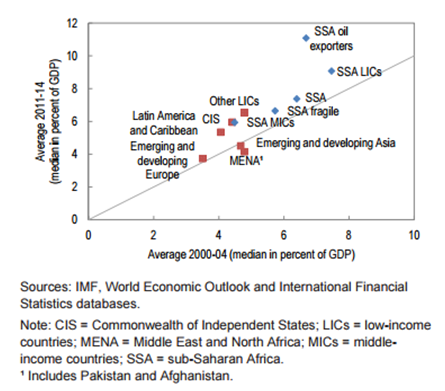

The fiscal frontier is defined as a function of the determinants of domestic resource mobilization (discussed in a previous article) and can therefore be estimated econometrically. Once this fiscal frontier has been obtained (i.e., potential revenue given the level of structural factors that make up the tax base), a comparison with the observed level of revenue makes it possible to define the distance between the government and its fiscal frontier. A study by Brun et al. (2015) undertook this exercise by estimating the average fiscal frontier for the region over several three-year sub-periods and comparing it each time with the observed tax ratio (in the data). The results show that the increase in public revenues observed above is indeed due to a steady increase in the tax effort since the early 2000s, with the gap between potential and observed tax revenues narrowing during this period. According to the authors, these developments can be attributed to the strong performance of the WAEMU[1] and COMESA[2] countries, where mineral resources remain relatively limited. According to the IMF, these additional efforts, probably driven by a growing awareness among SSA countries of the need to develop their own sources of financing rather than systematically resorting to international borrowing, have largely benefited from public investment aimed at increasing the collection and monitoring capacities of tax authorities (see Figure 3 below).

Figure 3: Public Administration Investment (2000-04 and 2011-14)

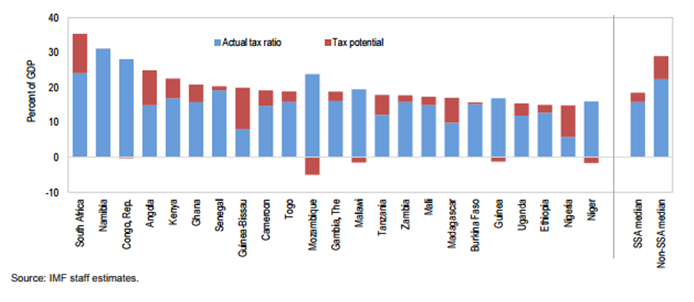

At the same time, in its latest Regional Economic Outlook, the IMF estimates the individual fiscal potential of SSA countries, but this time only for 2014, thus providing a very recent picture of the region’s performance (see Figure 4). The results show that the fiscal potential of SSA countries is positive on average, implying that there is still room for maneuver. Nevertheless, disparities between these countries remain significant. Countries that produce non-renewable raw materials (oil, diamonds) are those that, on average, have the highest fiscal potential, demonstrating that specific tax regulations for these activities are necessary to ensure that this wealth is taxed fairly and benefits the entire nation.

Figure 4: Sub-Saharan Africa, effective and potential tax ratio, 2014

Objectives and Latest Initiatives

The most recent analyses therefore tend to show that Sub-Saharan African countries are gradually catching up with the tax revenue levels of emerging countries, at the cost of significant fiscal efforts. Nevertheless, there is still room for improvement, which will be necessary in view of these countries’ growing needs in terms of infrastructure (both economic and social) and also in view of the ambitious sustainable development goals set at the United Nations summit last September. Where do these opportunities for improvement lie? Here we present some proposals from the IMF and a sample of the initiatives adopted at the third development conference held last July in Addis Ababa.

First, as emphasized by the IMF, SSA countries will only be able to reach their fiscal frontier if they have competent and effective tax authorities. It is therefore essential to strengthen the capacity of governments to collect taxes by increasing human and physical capital (in terms of both quality and quantity) within tax agencies. Effective administration also requires a certain degree of transparency and accountability. Any initiatives aimed at reducing corruption within public services will therefore help to move closer to the fiscal frontier.

At recent conferences on development financing, emphasis has also been placed on combating tax evasion in developing countries, particularly those in sub-Saharan Africa. With the aim of combating capital flight, the OECD and UNDP have jointly launched the Tax Inspector Without Borders (TIWB) initiative, which aims to strengthen the human capital capacities of the countries most affected by this phenomenon. This initiative aims to enhance North-South and South-South international cooperation and to provide countries in difficulty with specific expertise and training on the financial arrangements that enable capital flight.

In the same spirit, The Addis Tax Initiative, signed by more than 30 countries, requires signatory countries to double their technical assistance in the area of taxation and the mobilization of other domestic resources (particularly those derived from the exploitation of natural resources). This charter also commits to combating tax evasion. In addition, particular attention is paid to eradicating corruption within public services with the aim of collecting available revenues as fairly as possible, but also ensuring their fair and efficient use. These medium-term initiatives (5 to 15 years) will, if properly implemented, improve the functioning of governments and strengthen their legitimacy to levy taxes on taxpayers who are still very reluctant to pay their taxes given the low economic and social returns they perceive.

Secondly, both the IMF and the signatory countries ofthe Addis Tax Initiative recognize the need to broaden the tax base in developing countries. This broadening is all the more desirable in SSA, where regional trade integration is intensifying and tending to significantly reduce customs revenues. This will require the government’s ability to tax informal activities without hindering micro-entrepreneurship. The IMF also recommends the gradual elimination of economically and socially unjustified tax exemptions that are granted in many countries in the region to large companies and that foster corruption and opacity within public services.

Direct taxation systems will also need to be harmonized, both nationally and regionally, in order to prevent tax avoidance. Indirect tax systems will need to be sufficiently progressive to ensure that micro and small enterprises do not find themselves in a tax bottleneck. In a 2005 paper, Chambas points out that most SSA countries apply single-rate VAT systems with a fairly high tax threshold in order not to penalize the poorest taxpayers. However, he argues that these systems are not sufficient to offset the loss of revenue caused by regional trade integration. This concern is all the more pressing today given the significant funds needed to finance sustainable development. One of the solutions proposed by Chambas, in addition to taxing previously unregistered activities, is to abolish VAT exemptions on basic commodities. In poor countries where the population is predominantly rural, households subsist on their basic production and the sale of their products. However, when producers pay VAT on their intermediate consumption, a VAT exemption on final consumption (and therefore on final sales) tends to reduce their unit margin and thus their income. Abolishing these exemptions would therefore not only broaden the tax base, but also reduce the costs incurred by rural producers. However, this abolition would be likely to lead to an increase in consumer prices for basic commodities, negatively affecting the poorest consumers. Compensation mechanisms would then need to be considered and could be financed by additional taxes resulting from VAT liability.

Thirdly, the IMF and the signatory countries ofthe Addis Tax Initiative propose the definition of a specific tax for the natural resources sector, particularly fossil fuels, given their finite nature. These proposals are fully in line with the Extractive Industries Transparency Initiative (EITI) and would significantly increase the amount of tax collected by countries with large fossil fuel reserves.

Last but not least, it is essential that the use of domestic resources improves the living conditions of the poorest in a sustainable manner, without which it will be difficult, if not impossible, to maintain tax compliance, which is (in part) the key to effective and sustainable taxation.

Conclusion

While sub-Saharan Africa appears to be on the right track in terms of tax pressure, it is still a region where taxation is relatively low and tax systems are inefficient. However, the efforts made in recent years and the initiatives recently defined at international summits should, in the long term, enable these countries to catch up with the rest of the world. Moreover, these improvements appear necessary given the significant financial resources required to achieve the sustainable development goals that poor and middle-income countries have committed to meeting by 2030. But while there is still a long way to go, the course has been set and progress appears to be accelerating.

Bibliography

Jean-François Brun, Gérard Chambas, and Mario Mansour. « Effort fiscal des pays en développement, une mesure alternative » in Financer le développement durable, Economica (2015)

Gérard Chambas, « VAT and fiscal transition in Africa: the new challenges, » Afriquecontemporaine 2005/3 (No. 215), pp. 181-194.

Regional Economic Outlook: Sub-Saharan Africa. IMF, April 2015.