Abstract:

· Global agricultural production reached a record high in 2016 with abundant stocks, and prices are significantly lower than they have been over the past decade.

· Over the next ten years, the drivers of demand growth are expected to decline, while food insecurity will remain a major risk;

· Trade in agricultural commodities and fish is expected to grow at half the rate seen over the past decade;

· Southeast Asia remains plagued by food insecurity despite considerable improvement in recent years. Self-sufficiency will only be possible through a significant increase in yields.

The previous decade was marked by an increase in agricultural production and demand, and by the food crisis of 2007-2008. According to FAO data, cereal production rose from 2.3 billion tons in 2007 to 2.8 billion tons in 2014 [1], an increase of nearly 22% in seven years, and the FAO forecasts a record production year for 2016.

Demand has been driven by the rise of the middle class in China and other developing countries, which have consumed more cereals, but above all much more meat, the production of which requires a significant amount of cereals (6% annual increase in animal feed consumption). In addition, biofuels have been heavily subsidized over the past decade, which has redirected a significant amount of agricultural production towards their production (8% increase per year).

Finally, the last decade has seen a rebuilding of global cereal stocks to 2.5 billion tons in 2016, fueling demand. Stocks stood at 2.2 billion in 2007. However, production trends over the decade have been relatively close to demand, particularly between 2009 and 2013 [2].

2017-2026 production outlook

From 2016 onwards, global agricultural production reached record levels and flooded the markets. In addition, high grain stocks reduced precautionary demand [3]. Growth in Chinese consumption is slowing due to stagnant incomes, but also because consumers are spending an increasingly smaller share of their income growth on food. Finally, biofuel production is receiving much less support from developed countries, and the moderate recovery in oil prices is likely to limit demand for these types of fuels.

Prices are thus falling below their average level for the previous decade: cereals were 20% cheaper in 2016, as were dairy products, oilseeds are 10% cheaper, and meat is returning to its average level after being 30% more expensive in 2014 and 20% more expensive in 2015. Only sugar, fish, and cotton are on an upward trend.

However, the outlook reminds us that food prices are historically very volatile and that the decline observed is not, in itself, a guarantee of reduced instability. Other variables, particularly the weather, government action, and stock levels, play a very large role in determining prices.

Due to slowing demand and moderate prices at the beginning of this decade, cereal production is expected to stagnate or even decline. This could be offset by catch-up yields in less advanced regions. Meat and poultry production is expected to increase at a slow pace due to stagnant per capita consumption in major consumer regions. Dairy production is expected to increase, driven by production in India and Pakistan.

2017-2026 outlook for consumption

The OECD and FAO outlook shows that there will be little or no convergence in per capita food consumption (see chart below). Thus, inequalities in the composition of food baskets from one region to another are expected to remain as large as they are today. Daily calorie intake is highest in OECD countries, and the corresponding consumption basket has been the most balanced since 2006 and will remain so until 2026. By that date, only China will have a basket with a calorie intake comparable to that of OECD countries. India and Southeast Asia will reach 2,900 kcal per day and Sub-Saharan Africa 2,500 (compared to 3,500 for the OECD).

Caloric intake by category in several regions

Reproduction – Reproduction of OECD and FAO projections

International trade in agricultural products is expected to increase, but at a slower pace, in line with changes in demand and production. However, this is also explained by the trend toward stagnation in trade as a proportion of global GDP (already observed before the crisis). In addition, the food crisis of 2007-2008 and the high prices that persisted for a significant period of time prompted many governments to launch investment programs to mitigate the risks associated with food insecurity. Country self-sufficiency inevitably works against the growth of international trade.

That said, some regions of the world, such as sub-Saharan Africa, will remain highly dependent on imports. For example, 24% of the cereals consumed in this region were imported in 2014-2016, and the OECD-FAO outlook predicts that this figure will rise to 27% in 2026. In Mozambique, imported cereals will account for no less than 40% of cereals consumed, in Algeria they will account for 80%, and in Saudi Arabia 100%.

Although it is difficult to predict changes in consumer habits, trends toward organic and short-chain consumption could ultimately have a significant impact on the dynamics of international food trade. Similarly, in addition to the numerous hygiene regulations governing the food trade, measures to protect the environment, animal welfare, etc. could also be introduced.

The outlook for Southeast Asia

The report focuses in particular on Southeast Asia (Myanmar, Thailand, Lao People’s Democratic Republic, Cambodia, Vietnam, Philippines, Malaysia, Brunei Darussalam, Singapore, and Indonesia). The decision to focus on this region is justified by the rate of undernourishment observed there. In the early 1990s, the undernourishment rate was around 30% (the highest in the world at that time), whereas in 2014 it was only 10%.

This is a spectacular change, which can be explained both by production policies and by these countries’ growing involvement in international trade. That said, the Asian subcontinent is still plagued by food insecurity. In 2014/2016, it accounted for 9% of the world’s population and 8% of the world’s undernourished people.

These countries have entered a period of sustained economic development. Agriculture accounts for an increasingly small share of their national production and employment in this sector is declining. At the same time, one would expect farms to grow in size. However, land redistribution policies are having the opposite effect, which is likely to have a significant impact on productivity. The larger a farm is, the easier it is to mechanize, both because the fields allow for the use of machinery and because a larger farm means higher income and therefore more scope for investment at all stages of production (purchasing machinery for sowing, harvesting, and shelling; improving storage techniques; vehicles for delivering goods to market, etc.).

Although the region is diversifying and production is being integrated into global value chains, agriculture is still largely focused on rice production (from 40% in 1963 to 30% in 2013). This is because the primary objective of governments is to achieve food self-sufficiency and thus eradicate undernutrition.

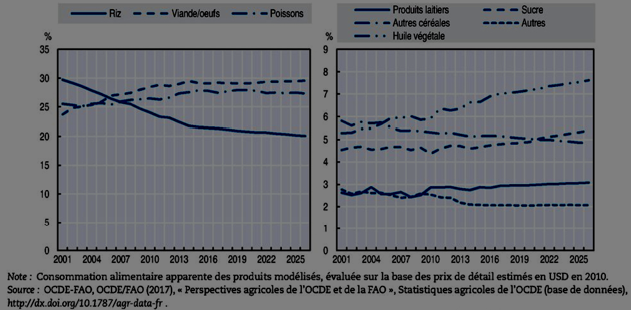

As the following graph shows, rice consumption as a percentage of food expenditure has been declining since 2001 and will continue to fall until 2025, albeit at a slower rate. This decline in rice consumption is benefiting meat and fish consumption, which is characteristic of consumption trends in rapidly developing regions.

Consumption trends in Southeast Asia

(share of food expenditure %)

Reproduction of OECD and FAO outlook

In general, growth in agricultural, aquaculture, and fishery production is expected to slow over the next decade. Several factors are at play, including the amount of arable land and environmental factors (global warming, but also the size of fish stocks). The increase in production will therefore be largely explained by higher yields.

Conclusion

Agriculture is emerging from a cycle of uncertainty and tension that has lasted since the food crisis of 2007-2008. Prices rose sharply and remained high for several years. They are now tending to fall as tensions ease, mainly due to very good harvests, the rebuilding of global stocks, and the weakening of institutional drivers of demand.

Prices should therefore be more stable and lower. However, the outlook does not anticipate any convergence in consumption patterns between the major regions of the world. On the other hand, changes in consumption, with a shift towards organic and short supply chains, could lead to significant changes, particularly in developed countries.

Finally, Southeast Asia, a key region for eradicating undernourishment, has made considerable efforts over the past 20 years. However, land reserves are now very limited and increasing production will require improved yields, which implies greater investment in agriculture, a sector that has traditionally received less funding.

[1] Data is only available up to 2014.

[2] http://www.fao.org/worldfoodsituation/csdb/fr/

[3] The demand for precautionary measures comes from countries close to food insecurity, but also from international cooperation organizations such as ASEAN, to guarantee market supply through stocks in the event of tensions on international markets.