Summary:

- The combination of i) the slowdown in real estate demand following the Brexit referendum, ii) the tightening of monetary policy by the Bank of England (BoE), and iii) the introduction of new credit regulations has led to a slowdown in London real estate prices, which had been rising since the 1980s (excluding the 2008 crisis).

- The change in prices can be explained by the BoE’s key interest rate (a proxy for the average mortgage rate), net disposable household income, net inward migration, and the real effective exchange rate.

- All scenarios lead to the same conclusion for the London property market: a rise in prices is fundamentally unjustified.

- If there were to be a migration exodus in response to the UK leaving the European Union, a correction in the real estate market would then be conceivable.

In this article, we attempt to present the state of the London real estate market and explore the various underlying mechanisms through which residential real estate could be affected in the aftermath of Brexit. We then present a few post-Brexit scenarios based on the key variables that could be affected: i/ the monetary policy rate, ii/ net migration from the European Union, and iii/ the real effective exchange rate of the pound sterling.

The London real estate market has long been characterized by soaring prices since the 1990s and the possibility of a bubble. Factors such as highly accommodative monetary policy, flexible credit policies, dynamic demographics, and the particular appeal of the world’s largest financial center have all contributed to sustaining this sustained price surge since the crisis. Prices finally stabilized in the months following the Brexit referendum, before finally turning down this year (-0.2% year-on-year in August 2018, -0.7% in June). As the Brexit date approaches (March 29, 2019) and with the increasing likelihood of an abrupt exit of the United Kingdom from the European Union (the famous no-deal), downside risks are mounting for the real estate market.

1. Residential demand, housing stock, and pricing in London

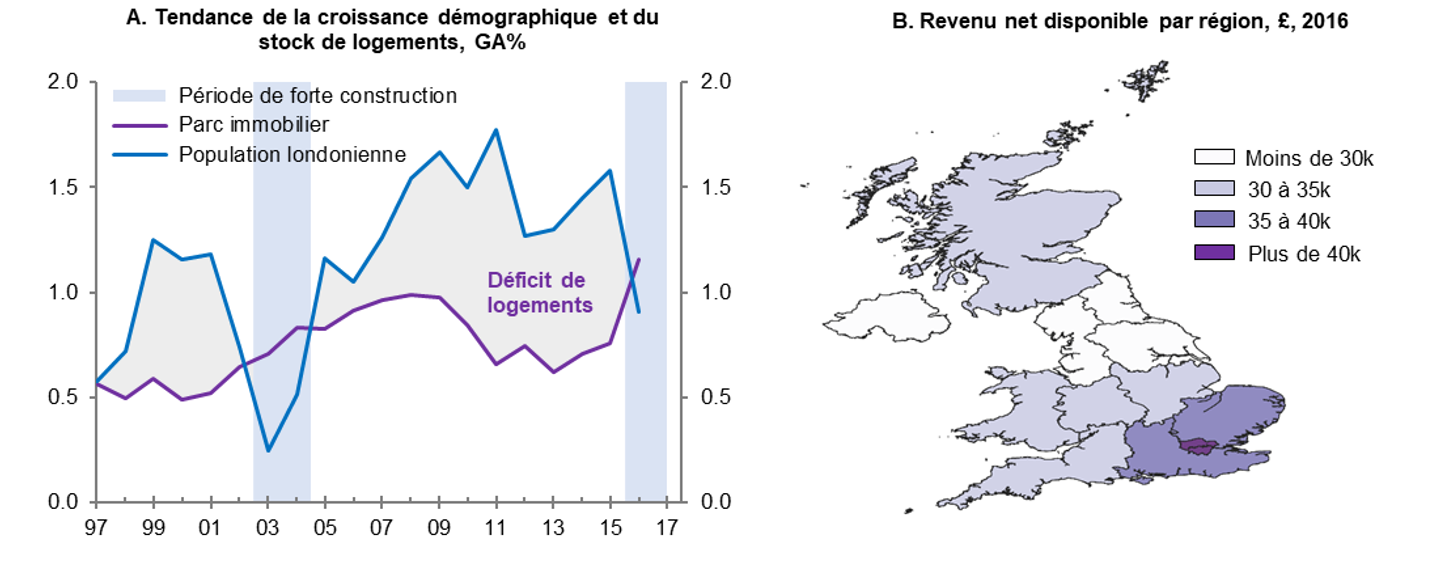

Apart from a few periods of strong construction, London’s population growth has been structurally more pronounced than the expansion of the housing stock over the past 20 years, reflecting sustained demand for the British capital (Chart 1, panel A).

This demand can be interpreted in two different ways: i/ demand for housing stems largely from owner-occupiers’ need to find a place to live or to earn rental income, but ii/ distortions such as the purchase of housing as a long-term speculative investment (with the hope of benefiting from capital gains on resale) will, all other things being equal, lead to an unsustainable increase in prices.

As real estate is the main financial asset of households, a price explosion and the ensuing correction would clearly weigh on financial stability. On the homeownership front, prices in London are being driven up by the size of net migration flows and the typical profile of new arrivals. The latter are generally highly skilled workers from abroad with high incomes (Chart 1, panel B). On average, the disposable income of households in London is 33% higher than in other regions of the United Kingdom (ONS, 2017). Conversely, more British people are leaving London than moving there. An increasing proportion of local jobs are therefore filled by foreign nationals, who may leave the United Kingdom in the event of an unfavorable Brexit.

On the institutional investor side, demand for real estate in London has been steadily increasing since the beginning of the century, reaching 25% of all real estate transactions in certain prime London neighborhoods such as Westminster (Sa, 2016). As a global financial center, London has also been exposed to the synchronization of real estate prices with other world capitals (IMF, 2018), especially as ultra-accommodative monetary policies have depressed sovereign yields. Global trade-offs must therefore be taken into account when assessing the attractiveness of London residential real estate.

Chart 1.Structural determinants of London real estate prices

Sources: ONS, DCLG, Natixis, BSI Economics.

2. Brexit and the impact of underlying mechanisms on London real estate

For the three scenarios presented below and to forecast real estate prices in the near term, we estimate a VAR[1] model by reconciling London real estate prices with their fundamentals: i/ the monetary policy rate, ii/ the London working population, and iii/ the real effective exchange rate of the pound sterling. Supply measures, such as the construction index, housing starts, and the volume of building permits issued, do not improve the model’s accuracy and prove to be of little explanatory value.

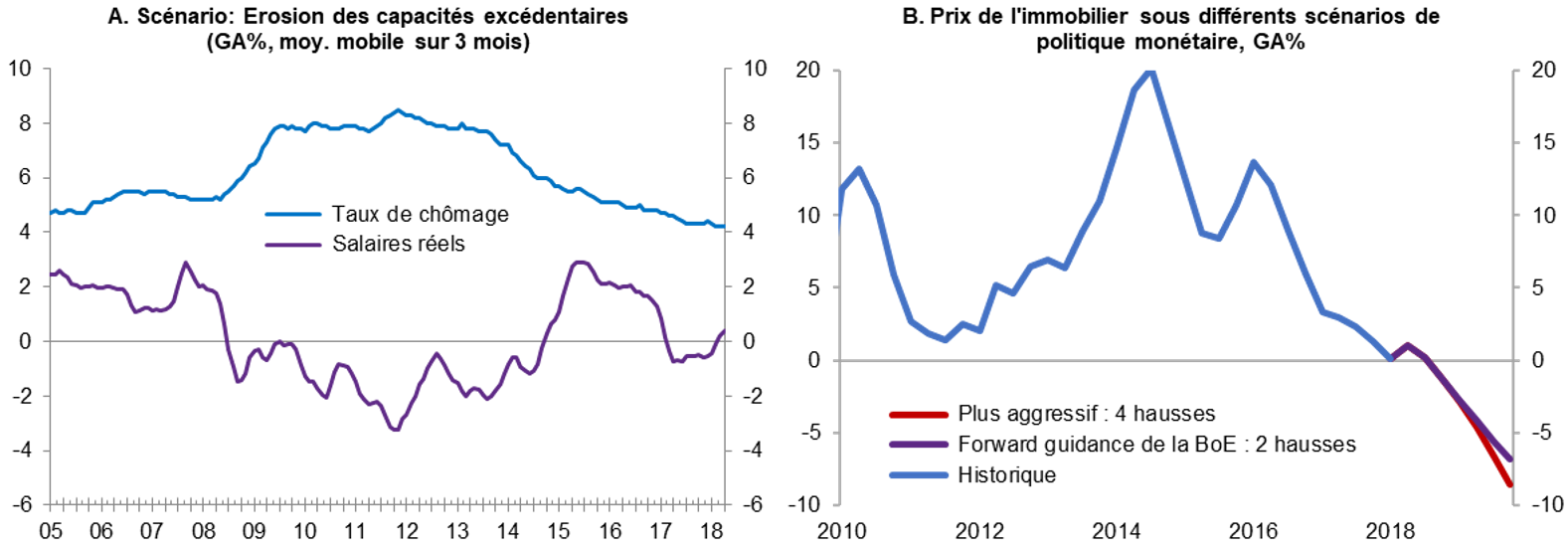

2.A. Monetary policy

The strength of the labor market (rise in real wages, unemployment rate at a record low of 4.0% in August) indicates that excess capacity continues to be absorbed in the United Kingdom.

Coupled with stronger-than-expected growth in Q3 – despite an unexpected slowdown in private investment – these factors gave the BoE sufficient leeway to raise its key interest rate on August 2, 2018. Healthier-than-expected public finances and the possibility of greater fiscal policy support for the economy (via the end of Philip Hammond’s austerity measures) would also favor the withdrawal of the post-crisis monetary bias.

In its August quarterly inflation report, the BoE also hinted at an earlier reduction in its balance sheet under QE (as soon as the key interest rate reaches 1.5%, rather than 2% as previously) and upside risks from an orderly Brexit (notably through trade and private investment contributing more to growth), suggesting that monetary policy tightening could therefore be more aggressive than initially expected by 2020.

In the very short term, however, and due to the continuing uncertainties surrounding Brexit, which are paralyzing private investment, the BoE is unlikely to respond to any signs of labor market overheating or accelerating domestic cost pressures by raising rates, at the risk of causing a more pronounced weakening of investment. The central bank and its governor have insisted that the current uncertainty justifies the status quo, and that the next rate hike towards normalizing the BoE’s monetary policy would be conditional on an orderly withdrawal from the EU, the most favorable scenario for long-term potential growth. Thus, in the event of an orderly exit from the EU, a further 25bps rate hike could occur in May 2019.

To assess and compare the impact of monetary policy on London residential property prices, we also incorporate another more extreme scenario (although not currently envisaged) into our model , with a more pronounced tightening than expected by the BoE, characterized by a rate 1% higher than our expectations by the end of 2019. This random scenario could, for example, accompany a possible overheating of the British economy in the event of an orderly exit from the European Union.

The impact on real estate is intuitively bearish: a rise in rates automatically leads to higher mortgage costs (as mortgage rates are linked to key rates), as well as an increase in variable-rate mortgages, which are common in the UK (around 15% of new loans issued over the last five years). As the cycle of monetary tightening accelerates and all other things being equal, households’ affordability and solvency are reduced, as is demand for real estate, even though the London price index has risen by 73% over 10 years (August 2018/August 2008).

As shown in Chart 2 below, the prospect of monetary policy normalization (regardless of the degree of tightening) in a context of widespread weakness in real estate demand will weigh on prices in the short term. While in the stress scenario, with tighter-than-expected monetary policy, prices would fall by 8.6% YoY in Q4 2019, our baseline scenario still points to a decline in London real estate prices. All other things being equal, this means that keeping rates lower than otherwise would be beneficial to the UK real estate market, particularly through more favorable mortgage rates.

Chart 2.Property prices and monetary policy trajectories

Source: ONS, DCLG, Natixis, BSI Economics.

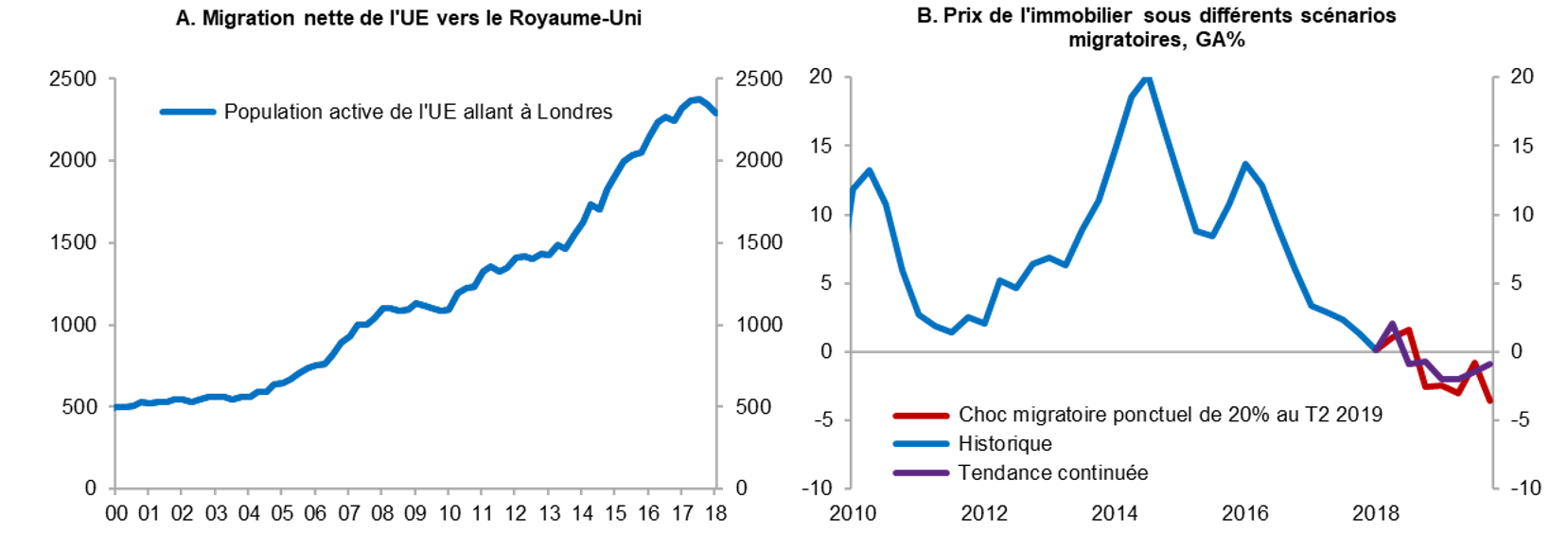

2.B. Net migration from the European Union

From a statistical point of view, it is difficult to estimate the share of EU nationals in the UK workforce, which explains why the UK Parliament has asked the Migration Advisory Council to conduct an audit on migration from the EU ( with a view to designing a post-Brexit immigration regime). However, given the significance of non-British investment in London real estate and in order to model post-Brexit migration scenarios, we need to estimate the proportion of European nationals who are able to buy property in London.

We are therefore exploring two simplified scenarios:

i/ a net migration flow from the EU behaving in London as elsewhere in the UK, with a steady decline of 2.43% in the number of EU nationals in the UK workforce over the forecast horizon, and

ii/ an arbitrary and persistent 20% shock to net migration from the EU, followed by an estimate of the impact on the London workforce.

As migration flow figures are only available for the UK as a whole on a quarterly basis, we extrapolate them for London based on two key criteria highlighted by the House of Commons on migration in its February 2018 report:

1/ EU nationals accounted for 42.3% of net migration to the UK in 2017

2/ they represent 13.4% of London’s working population

Based on these two facts, and because our model only covers the London workforce, we can reasonably estimate the impact of changes in the workforce on real estate prices. While the credit channel suggests that monetary policy has the potential to impact both the supply of real estate and residential demand, a lower net migration balance in the short term should directly affect real estate prices. Thus, without considering the worst-case scenario of a mass exodus from London back to the European continent, we expect that a lower net migration of European nationals to London will reduce housing shortages and therefore negatively affect prices in the short term.

However, our model shows that a slowdown in migration flows is unlikely to more than offset the negative effects of monetary policy (Chart 4). This seems to corroborate Marc Carney’s comments that a disorderly Brexit could lead to a correction in the London property market. The BoE’s worst-case scenario stress tests predict a price correction of -20%/-35% in the event of a shock to the banking system.

Chart 3. Property prices and migration scenarios

Source: ONS, DCLG, Natixis, BSI Economics.

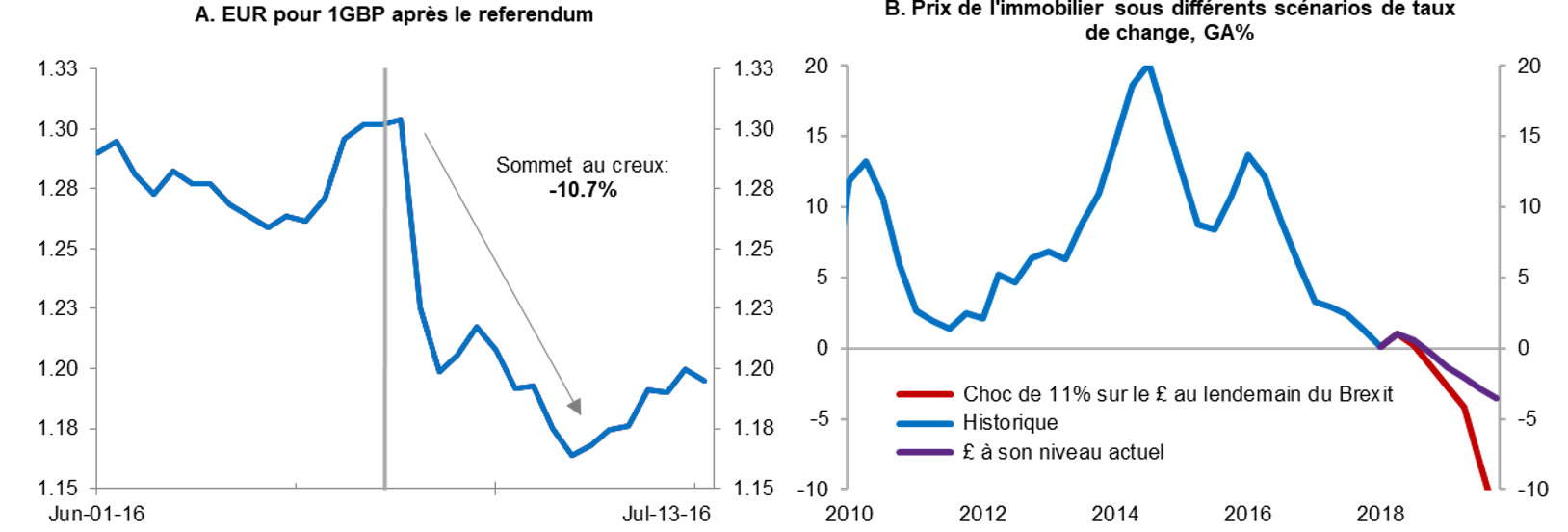

2.C. The real effective exchange rate of the pound sterling

In the month following the June 2016 referendum, the real effective exchange rate of the pound sterling depreciated by 10.7% between its peak and trough, representing a decline of more than 15% over 12 months against the major currencies. The depreciation of the pound subsequently led to high imported inflation (with the input PPI rising by 9.8% in June 2017), weighing on real household income and ultimately depressing private consumption. So far, after several months of volatility, the pound sterling exchange rate has been the main observable macroeconomic consequence of Brexit on the economy. We can therefore assume that a disorderly exit from the EU (assuming no agreement is reached before March 2019) would inevitably lead to a further sharp depreciation of the pound sterling against major currencies.

To estimate the potential impact of exchange rate fluctuations (a proxy for the global factor), we identify two scenarios:

i/ the pound sterling remaining at its current level throughout the forecast horizon, and

ii/ as after the 2016 referendum, an 11% quarter-on-quarter depreciation of the real effective exchange rate of the pound (between Q1 and Q2 2019, to reflect the effective exit date of March 29, 2019).

The decision to explore the exchange rate channel is explained by its significance in terms of the attractiveness of London to foreign investors. For example, the real estate market experienced an unexpected rebound in the aftermath of Brexit due to foreign investment, with London residential property becoming 11% cheaper month-on-month in foreign currency terms. Thus, a rebound in real estate prices following a depreciation of the pound would indicate a shift in residential demand away from British individuals and toward international demand.

Our model corroborates the general idea that Brexit will affect the overall attractiveness of London real estate, to the extent that a sharp depreciation of the pound sterling would not translate into an aggregate rebound in prices. In practice, the loss of appeal of London real estate from an institutional investment perspective can also be explained by the combined effect of the general weakness of the market (with prices in negative territory and no returns in sight) and the end-of-cycle normalization of global monetary policies improving bond yields.

Chart 4. Real estate prices and real effective exchange rate

Source: ONS, Bank of England, Natixis, BSI Economics.

Conclusion

Regardless of the transmission channel explored, the real UK economy and the uncertainty surrounding Brexit will not support London real estate in the short term. As monetary policy tightens, and despite certain government initiatives such asHelp-to-Buy, the rising cost of credit will limit access to home ownership and therefore have a negative impact on prices.

Whether Brexit is orderly or not, migration factors and the end of a speculative era in London real estate are likely to have a negative impact on prices. As for the longer-term trajectory of the real estate market, this will largely depend on the post-Brexit arrangements negotiated between the United Kingdom and the European Union.

Bibliography:

Alberts, W. (1962). Business cycles, residential construction cycles, and the mortgage market. The journal of political economy, 263-281.

Claessens, A. (2008). What happens during recessions, crunches and busts? IMF working paper 08/274.

Fair, R. C. (1972). Disequilibrium in housing models. The Journal of Finance, 207-221.

Girouard, N. (2005). Recent house price developments: the role of fundamentals. OECD working papers.

Hawkins, O. (2018). Migration Statistics, Information Paper, House of Commons Library.

IMF (2018). House price synchronization: what roles for financial factors? (pp. 93-133).

Leamer, E. (2007). Housing IS the business cycle. NBER working paper no. 13428.

The Financial Times. How will Brexit affect UK house prices and mortgages?; October 15, 2018.