Usefulness of the article : this note highlights the limitations of monetary policy in the eurozone in the face of persistently low interest rates. In this context, the experience of the Bank of Japan may be useful to the European Central Bank, particularly in the context of its strategic review.

Summary:

- We review the decisions taken by the Bank of Japan in recent years to combat falling inflation expectations and the consequences of the persistent low interest rate environment.

- Given that the eurozone shares many similarities with Japan, we attempt to analyze the possible implications for the monetary policy of the European Central Bank (ECB).

- The timing is obviously significant, as the ECB is currently reviewing its monetary policy to assess the relevance of its inflation target, the effectiveness of its current tools, and the advisability of adopting new ones.

Over the past decade, the eurozone economy has tended to become more like Japan’s, forcing the European Central Bank (ECB) to explore negative interest rates and asset purchase programs in order to avoid deflationary pressures and attempt to revive sluggish economic growth. However, the Bank of Japan (BoJ) has continued to demonstrate creativity in recent years by implementing yield curve control[1] and intervening directly in the equity market throughETF purchases[2].

In January 2020, the ECB officially launched its strategic review. The objectives are multiple, as the assessment must cover the quantitative formulation of price stability, the range of monetary policy instruments, economic and monetary analysis, and communication methods. Other considerations relating to financial stability, employment, and sustainable development should also be taken into account in the assessment. In this context, there are probably lessons to be learned from the Japanese experience.

The purpose of this note is to analyze the costs and benefits of the various measures adopted by the Bank of Japan in recent years and to examine their transposability to the ECB’s strategy.

1. What inflation target?

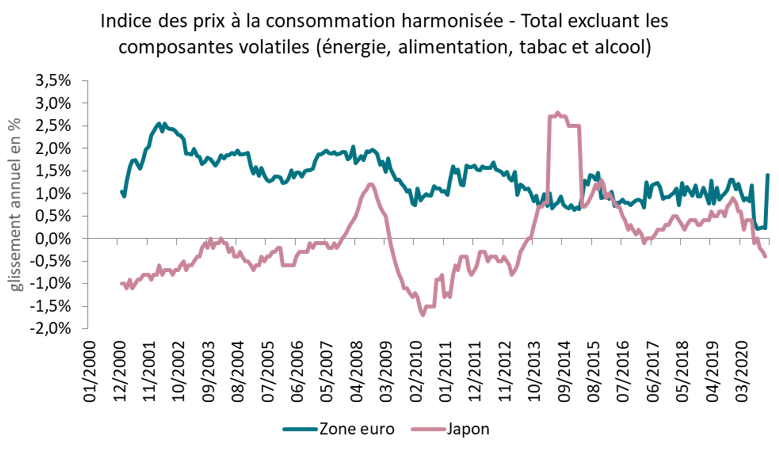

Price stability has been the primary objective of central banks since the late 1970s, but it was not until later that a quantified target was introduced. The Bank of Japan waited until 2013 to officially introduce an explicit target of 2%. Since 2016, the ECB has had more or less the same objective, as it must « achieve price stability in the medium term at a target close to but below 2%. » In retrospect, the target seems far removed from reality. In Japan, core inflation, which excludes volatile components such as food and energy prices, has struggled to exceed 1% (excluding the period of VAT increases in 2014). The Bank of Japan had already ruled out any change to its inflation target during its strategic review. However, the conclusions were interesting in terms of understanding the reasons for maintaining it. Beyond structural explanations (demographics, labor market), the main explanation lies in the fact that most inflation expectations in Japan are anchored in the past (adaptive expectations) and therefore require a strong commitment to reach the target so that economic agents can perceive it as feasible and no longer as an unattainable goal. In this context, lowering the target could be perceived as an admission of failure.

In the eurozone, the ECB’s strategic review could lead to a revision of its inflation target, particularly following the latest comments by former ECB President Mario Draghi, who suggested in 2019 that « a symmetric target essentially means that our 2% target is not a ceiling, and that inflation can deviate below as well as above . »[3] Following the example of the Bank of Japan and the Federal Reserve (Fed) in the United States, the ECB could commit more firmly to achieving its target. The Fed recently adoptedAverage Inflation Targeting, allowing the central bank to tolerate exceeding the target and thus give itself some time (and the economy some time to continue growing) before having to tighten its monetary policy. Another solution under consideration would be to adopt a target range, as the Bank of Australia has done, while maintaining a lower limit compatible with the current target of between 2% and 3%. Choosing too ambitious a target could trap the ECB in a perpetual accommodative policy. Conversely, lowering the target could be seen as a failure and undermine its credibility. The choice of target will be a question of balance and communication.

Sources: European Central Bank, Bank of Japan, BSI Economics

The Bank of Japan has adopted new tools in recent decades and, despite mixed results, it is possible to analyze their success or failure and thus debate their transposition to the ECB’s monetary policy.

2. Innovating in a low interest rate environment

The Bank of Japan was not the first to introduce negative policy rates, but it has considerable experience in a low interest rate environment. In fact, apart from a period of tightening between July 2006 and December 2008, the short-term rate remained at 0% from the early 2000s until February 2016, when it moved into negative territory (-0.1%).

In theory, lowering short-term rates should reduce rates across the entire yield curve and encourage a depreciation of the exchange rate. All other things being equal, if Japanese nominal interest rates fall, the difference in real interest rates (nominal interest rates adjusted for inflation) with other countries is greater, so capital inflows are lower, leading to a depreciation of the domestic currency. Lower financing costs and a weaker domestic currency should, in theory, contribute to economic recovery.

However, demographic decline, lack of economic prospects, and deflation have prevented Japan from returning to a phase of economic expansion, leaving the Bank of Japan with no choice but to maintain its key interest rates at extremely low levels. The persistence of this low interest rate environment has complicated the transmission of monetary policy, particularly through the banking channel.

The difficulties facing the Japanese banking sector are not new and emerged in the wake of the 1990 financial crisis and the so-called « lost decade, » which was characterized by very low growth and a period of deflation. In 2008, the banking sector was more resilient than in other countries because it was less exposed to « toxic » assets, even though it suffered a significant decline in its solvency ratio, which required recapitalization. Finally, the Japanese banking system is heterogeneous, with a few large banks having access to international markets and therefore able to diversify their revenues, and a multitude of regional banks experiencing a steady decline in profitability directly linked to demographic decline and low diversification. The persistence of a low interest rate environment (and even negative rates on reserves) is eroding capital and therefore the ability of banks to lend.

The Bank of Japan has put in place two mechanisms aimed at mitigating the effect of negative rates and encouraging banks to continue lending. First, it has developed lending programs for financial institutions where low interest rates were conditional on lending to businesses and households. A second incentive concerns the rate of return on private banks’ reserves at the central bank. Instead of applying a single rate to reserves, the BoJ has introduced a « tiered system » with three different rates: +0 .1 %; +0.0%; and -0.1%. The BoJ is therefore offering banks the opportunity to place a larger portion of their reserves in positive territory on condition that they continue to extend credit to households and businesses.

The use of these two instruments, long-term loans and tiering, clearly illustrates the limitations and costs of maintaining a low interest rate environment. However, the Bank of Japan cannot rule out further cuts to its key interest rate, particularly if the yen appreciates significantly. Reducing the real interest rate differential with its economic competitors means accepting the risk of an influx of investment that appreciates the value of your currency and raises fears of imported deflation, thereby negating efforts to increase inflation.

The parallel with the eurozone is quite obvious, with the difference that the European banking system is not (yet) as fragile as in Japan. Short-term rates have been in negative territory since 2014, long-term lending operations (TLTROs) are now part of routine operations to support the banking sector, and tiering was introduced in 2019. The ECB seems reluctant to lower key interest rates any further, aware that the costs of such a policy probably outweigh the benefits, particularly for the financial sector. For the same reasons as the BoJ, the ECB will probably retain the option of lowering its rates again, so it needs to consider compensatory measures for the banking sector.

New long-term loans or a recalibration of tiering are unlikely to be sufficient, especially as this comes at a « cost » since these are « loss-making » operations for the central bank. The central bank’s objective is not to make a profit, but it must nevertheless reconcile its balance sheet with its actions. Hence the possibility of considering new tools in the face of new objectives. The BoJ recently took this step in the name of financial stability by announcing the creation of a « subsidy » for banks that improve their cost/income ratio or engage in mergers and acquisitions.

These subsidy mechanisms for banks are technically possible in the eurozone but unthinkable at the political level. In this context, why not add a new objective in addition to price stability and financial stability? The fight against climate change can claim to be one of the objectives accepted by politicians. The ECB could create a carbon « bonus/malus » around the refinancing rate, calculated for each bank based on its carbon footprint, which is itself calculated on the basis of the financing it grants (Kempf (2020)). If commercial banks turn away from interbank lending, they can obtain refinancing credits from the central bank by exchanging assets (collateral). The ECB could follow the same logic and apply a carbon premium based on the ecological quality of the collateral.

However, immediate implementation could create a distortion of competition. A system that rewards the most virtuous at a given moment in time but also takes improvements into account could mitigate distortions. Thus, the « premiums » received by banks could offset an even more accommodative monetary policy, for example in the event of further rate cuts. There are much more effective options for « greening » the ECB’s monetary policy (QE, green TLTROs, etc.), but here we are only discussing those that could give the ECB some leeway to increase the effectiveness of its negative interest rate policy.

3. Promoting flexible asset purchase programs

The second major family of instruments is based on asset purchases. In 2013, the Bank of Japan launched a vast asset purchase program, Quantitative and Qualitative Easing. This involves buying back domestic sovereign debt securities (JGBs, or Japanese Government Bonds) or corporate debt securities for a pre-announced amount. The expected effect on inflation was based on three transmission channels:

(1) a fall in nominal interest rates via the compression of term premiums;

(2) a rebalancing of portfolios towards riskier assets due to the appreciation of low-risk assets;

(3) currency depreciation via capital outflows.

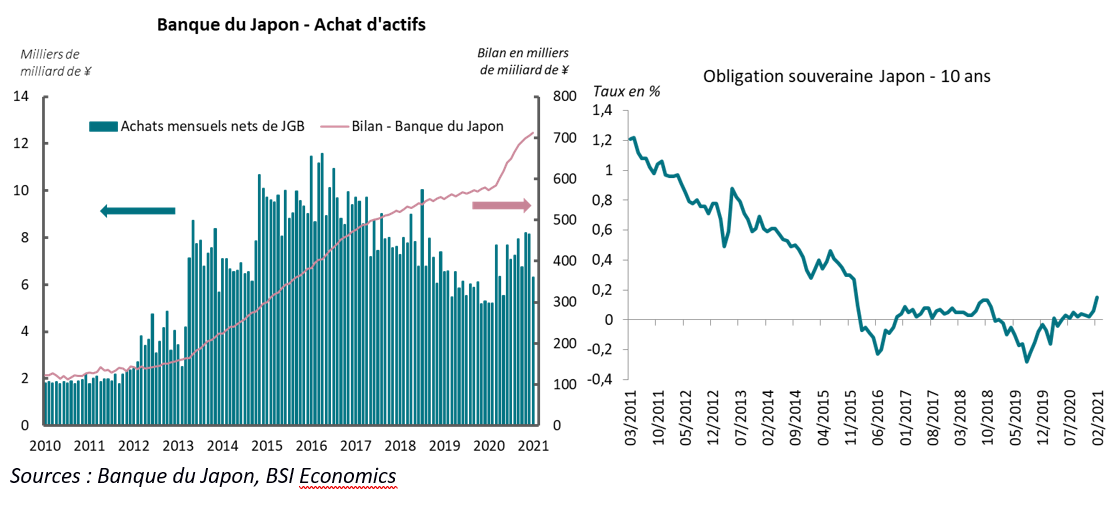

Like many central banks, the Bank of Japan has never really managed to raise inflation expectations, despite tripling its balance sheet. In 2016, it therefore opted for a tool already adopted by the United States in 1942 [5]: yield curve control. More specifically, the BoJ committed to adjusting its asset purchases so that the interest rate on 10-year sovereign bonds would fluctuate around 0% plus or minus 20 basis points. In other words, if the bond rate is too close to the upper range (+0.2%), the BoJ buys more in order to bring it back to the target rate—and vice versa if the rate reaches the lower range (-0.2%). If the central bank is sufficiently credible, the rate remains close to 0% without even having to buy securities.

The flexibility of the program plays a key role in its effectiveness, as net monthly purchases of sovereign debt have fallen from €90 billion in April 2016 to €40 billion in February 2020. However, during the COVID crisis, the BoJ reacted quickly and increased its net purchases to around €62 billion per month since March 2020. The other advantage is that this avoids jeopardizing the cost of public debt by compressing interest rates so that they remain below the real growth rate.

However, this tool does not only have advantages and continues to be a concern for institutional investors bound by long-term commitments (insurance companies, pension funds). Indeed, the latter have to contend with extremely low rates of return across the entire yield curve and are therefore seeking returns from riskier assets and/or drawing on their own funds, while regularly revising downward their promised returns to savers. To mitigate these effects, the BoJ has opted for a steeper yield curve—a more pronounced difference between very long-term interest rates and short- to medium-term rates—by purchasing fewer securities with very long maturities (10-40 years) and maintaining significant purchases of « shorter » maturities (0-10 years).

An explicit transposition of the yield curve control strategy in the eurozone seems complicated because there are as many sovereign debts as there are countries in the eurozone, and targeting a reference rate (such as the weighted average of each country’s interest rates) could meet with political resistance. However, the ECB seems to have found a solution with the Pandemic Emergency Purchasing Program (PEPP), introduced last March, which allows it to flexibly purchase most eurozone sovereign and corporate debt. The ECB implicitly controls yield curves through the flexibility of its purchases, which evolve according to « financing conditions, » a definition that is deliberately vague since the ECB takes a « holistic and multifaceted » approach. Although this program is not intended to be permanent, the ECB has given itself some leeway by postponing the end of net purchases until March 2022 and reinvestment operations until the end of 2023.

The ECB must also reconcile its actions with the holding limits defined in the European treaties, yet the ECB’s debt stock is approaching these limits, particularly in terms of sovereign debt. Faced with this challenge, there are two alternatives: change the current rules or reduce the ECB’s net purchases (in other words, ensure that the stock grows more slowly than GDP).

The first solution would require significant political trade-offs, such as increasing or even removing these holding limits. After all, neither the Bank of Japan nor the Federal Reserve has official limits on the percentage of debt it can hold. Another option could be to target purchases more in countries where the risks are highest. However, this seems unlikely given the differences between member countries on these options. Once the crisis is over, we can assume that the ECB will instead look for ways to reduce its net purchases in the medium term. Communicating a purchase volume in advance and sticking to it provides some visibility to financial markets, but in the case of the ECB, it would be difficult to increase its current program without undermining its credibility under European treaties. It therefore seems appropriate to extend the principle of flexibility from the PEPP to the APP[7], which could once again become the only asset purchase program in a few semesters, even if this assumption is not necessarily being discussed officially at this stage. As highlighted by the Japanese experience, the ECB’s credibility will be essential in enabling it to purchase only when necessary.

The Bank of Japan does not only purchase government or corporate bonds. Faced with the risk of inflation expectations falling, the BoJ decided in 2014 to combine and increase its use of unconventional instruments by intervening directly in the stock market via ETFs orJapanese Real Estate Investment Trusts. The aim was to stimulate consumption and therefore inflation by increasing financial assets through a wealth effect, but also to lessen the shock in the event of a downturn.

Seven years later, the BoJ’s assets have exceeded the equivalent of €350 billion and now represent 7% of the Japanese stock market and 90% of the Japanese ETF market. The BoJ is now accused of distorting prices and fueling a possible bubble in the equity markets, as well as complicating the governance of certain companies, as the BoJ has seats on boards of directors but must remain neutral. Finally, it exposes its balance sheet to significant losses in the event of a downturn.

The ECB may be tempted to add this tool to its monetary arsenal, even though the risks of inflation expectations falling short are still quite far removed from what Japan has experienced. However, if it buys « directly, » governance issues will arise, and if it buys ETFs, it will be accused of favoring passive management. In addition, there could be significant political resistance from certain governors who consider that the ECB’s interventionism is already too strong. Finally, consideration would need to be given to the rule for allocating purchases: replication of the current share in sovereign bond purchases (capital key) or a new rule (by sector), maximum holding limits, etc. Finally, if such a measure is adopted, purchases will need to be flexible, for example increasing during periods of stress and decreasing during periods of expansion.

4. What about closer cooperation between fiscal and monetary policy?

On a different note, but still with a view to achieving the central bank’s objectives, coordination between fiscal and monetary policy must be stepped up. In theory[8], a strong fiscal stimulus, combined with a well-calibrated accommodative monetary policy, should help to create positive growth momentum and ultimately generate inflation.

Drawing a parallel with Japan, Europe could draw on the recent experience of Abenomics, which was based on « three arrows »: (1) quantitative easing (QQE), (2) a « flexible » fiscal policy, i.e., pro-growth in the short term, aiming for a balanced primary balance in the medium term, then a reduction in public debt beyond that, and (3) an ambitious structural reform agenda designed to promote private investment and raise growth potential to 2%. Make no mistake, this is not about replicating Abenomics. The characteristics of the economies are not identical and the success has been only partial: Japan has effectively emerged from deflation, but inflation remains well below target, while potential growth has made little progress. However, such coordination between fiscal and monetary policy could inspire eurozone members.

The European Union’s recovery plan partially responds to this notion of closer cooperation. The plan aims not only to accelerate the energy and digital transition, but also more broadly to stimulate all public and private actors in order to create an environment conducive to higher growth. The plan itself is probably insufficient to substantially change potential growth, but the initiative has the merit of existing and we cannot rule out new plans in the future, especially as it creates new assets eligible for the asset purchase program that do not fall within the ECB’s country holding limits.

Conclusion

The ECB’s strategic review is an opportunity to redefine or reaffirm its objectives and, above all, the tools used to achieve them. Drawing on Japan’s experience, we will need to pay particular attention to developments in negative interest rate policy and the various compensation measures. We have seen that adding a climate objective, combined with the creation of new tools such as a carbon bonus/penalty, can create new opportunities. A second point of attention will be the future of asset purchase programs, particularly their flexibility and the possibility of extending them to the equity markets. Thirdly, cooperation between fiscal and monetary policy must be strengthened.

The ECB has also announced that the strategic review should be used to assess monetary policy action to combat global warming. We have not dealt with this subject exhaustively in this note because, firstly, the Bank of Japan is not innovative in this area and, secondly, most of the options considered are modifications of existing programs (e.g., QE, green TLTROs ) and do not in any way provide the ECB with greater room for maneuver. A future note exploring ways to green monetary policy could provide a more complete understanding of the issues at stake in this strategic review.

Bibliography

Kempf (2020) « Greening monetary policy, » Revue d’économie politique 2020/3, vol. 130

Kenneth Garbade (2020), “Managing the Treasury Yield Curve in the 1940s” – Federal Reserve Bank of New York Staff Reports

C.Blot, J.Creel and P.Hubert (November 2019) “Thoughts on a Review of the ECB’s Monetary Policy Strategy”

Speech by Mario Draghi at the monetary policy briefing (July 2019)

Speech by C. Lagarde (September 2020) “The monetary policy strategy review: some preliminary considerations”

O. Blanchard & L. Summers (2019) “Rethinking stabilization policy: evolution or revolution?” – NBER Working Paper

J. Furman & L. Summers (2020) “A Reconsideration of Fiscal Policy in the Era of Low Interest Rates” – Peterson Institute

[1] As part of the BoJ’s policy, the volume of bond purchases is adjusted to match the desired interest rate level (i.e. if the bond rate rises above the target, the BoJ buys more bonds to bring it back to the target rate – and vice versa if the rate falls).

[2] An Exchange Traded Fund is a fund that replicates the performance of a predefined index (e.g., the CAC 40).

[3] Speech by Mario Draghi in July 2019.

[4] In this case, inflation must be kept above the target if it has previously been below it, so that, on average and over a given period, inflation is at the target level.

[5]Kenneth Garbade (2020), “Managing the Treasury Yield Curve in the 1940s” – Federal Reserve Bank of New York Staff Reports

[6] There are no official limits under the PEPP, as the ECB wanted to retain maximum flexibility, but it must reconcile its purchases with those already made under the APP program and, for example, cannot hold more than 50% of a sovereign issuer’s debt.

[7] The APP (Asset Purchase Program) is the ECB’s asset purchase program, launched in 2014 to combat deflationary risks. Under this program, the ECB purchases sovereign debt as well as investment-grade corporate bonds. In 2018, the ECB stopped net purchases but continued to reinvest the amount of maturing securities. In November 2019, it relaunched the program with net purchases set at €20 billion per month.

[8]O.Blanchard & L. Summers (2019) “Rethinking stabilization policy: evolution or revolution?” – NBER Working Paper

J. Furman & L. Summers (2020) “A Reconsideration of Fiscal Policy in the Era of Low Interest Rates” – Peterson Institute