Usefulness of the article: Highlighting the concept of the natural interest rate shows that monetary policy in the eurozone is simply adapting to the cyclical and structural forces that are pulling the equilibrium rate down. While the choice of instruments may be questioned, the degree of flexibility in the monetary policy governed by the European Central Bank appears to be appropriate.

Summary:

- The natural interest rate in the euro area, which prevails to stabilize inflation and ensure full utilization of productive capacity, is undergoing a structuraldecline and is now in negative territory.

- Monetary conditions have been eased substantially through unconventional channels, with key interest rates reaching their lower bound.

- While monetary policy in the euro area can indeed be described as accommodative, its degree of flexibility seems appropriate in a situation where the natural interest rate is persistently depressed.

.jpg)

The influence of central banks on the economy has grown steadily over the past 40 years. Sometimes accused of pursuing overly aggressive policies to the point of influencing a large number of market prices through money creation (as was still the case until early 2020), or sometimes criticized for their lack of commitment, which would result in overly rigid and suboptimal monetary conditions (European sovereign debt crisis in 2011), central banks are perceived as both the cure and the poison for the ills that afflict us.

Shedding light on the direction of monetary policy, i.e., whether it is restrictive or accommodative, provides insight into whether the European Central Bank is doing too much or should be doing more.

1) The Wicksellian approach to monetary policy

There are different approaches to determining whether monetary policies are expansionary or restrictive. Recent literature has revived a key concept that is of particular concern to proponents of « secular stagnation »[1] , namely the natural interest rate, theorized by economist Knut Wicksell in 1898. This equilibrium rate is the rate that prevails to balance savings and investment and stabilize inflation (in positive territory without the emergence of inflationary pressures) when the economy is operating at its growth potential. The natural interest rate, which is unobservable by design, depends on cyclical factors when these factors cause a lasting imbalance in macroeconomic variables such as savings and investment, but above all on long-term trends such as demographic aging or the downward trend in total factor productivity.

The concept of the natural interest rate can thus be used to assess the stance of monetary policy. The latter is considered neutral when the central bank’s intervention rate is equal to the natural interest rate. Monetary authorities can thus stimulate/cool the economy by lowering/raising short-term rates below/above the natural interest rate. While it is a theoretically extremely powerful instrument, its conceptual complexity lies in its unobservable nature, which requires the use of modeling. However, there are as many estimates as there are methods for measuring it.

2) From the difficulty to the necessity of estimating the natural interest rate

While economists continue to disagree on the level of the natural interest rate, there is broad consensus that it has been in structural decline for several decades in advanced economies (Laubach and Williams 2016, Holston et al. 2017, Del Negro et al., 2018, Arena et al., 2020). There are many reasons for this: demographic aging (Eggertsson et al. 2017), weaker long-term growth (Gordon 2015), an overabundance of savings and a lack of investment (Summers 2014), an increased preference for safe assets[2](Farhi et al. 2015), and rising inequality[3](Arena et al., 2020).

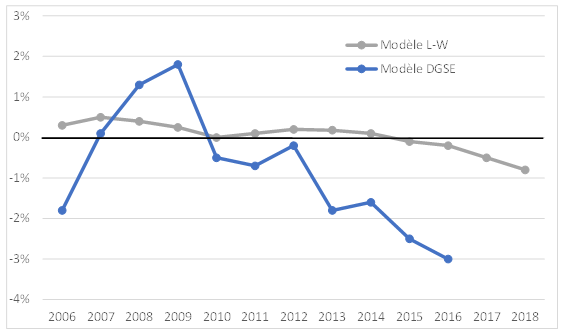

The vast majority of estimates are based on the seminal model developed by Laubach and Williams (2003), whichis considered the benchmark. Very recently, IMF economists (Arena et al., 2020) used this method to estimate the natural interest rate for the euro area between 2000 and 2018. In addition, DSGE models have also been used in recent years (Hristov 2016). While there are still differences between estimates, economists agree that the natural rate in the euro area has been negative for several years and that the Covid-19 crisis is causing a negative shock that is contributing to this decline beyond its structural trend.

Figure 1: Estimates of the natural interest rate in the eurozone

Source: Hristov (2016), Arena et al. (2020), BSI Economics

In this view, monetary policy in the eurozone is no longer the cause of zero or even negative interest rates, but rather the consequence of underlying trends that are pulling the natural interest rate downwards.

3) The use of unconventional policies to circumvent the « zero lower bond » problem

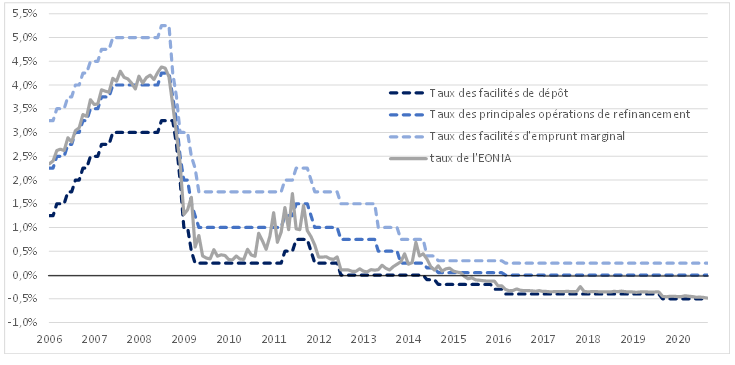

Before the Great Recession of 2008, the ECB’s key interest rate was the main lever for conducting monetary policy, as nominal rates were high enough in normal times to provide sufficient room for maneuver in the event of a negative shock.

The succession of shocks has therefore led to more frequent episodes at the zero lower bond, rendering conventional monetary policies ineffective. Indeed, monetary authorities cannot lower rates significantly below zero because economic agents would opt to hold fiat currency (liquidity trap), which would render a policy of very negative rates ineffective.

Chart 2: Changes in key interest rates and the euro area overnight interbank rate

Source: ECB, BSI Economics

To get around this problem, the ECB has turned to so-called unconventional policies to ease monetary conditions through channels other than interest rates (forward guidance, public and/or private asset purchase programs, targeted long-term refinancing operations).

4) The implicit rate (or shadow rate) as a true indicator of the ECB’s degree of accommodation

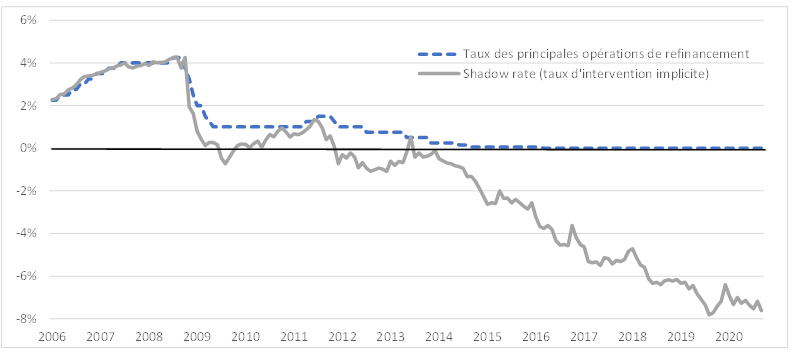

As the ECB uses a wider range of instruments than just the key interest rate, comparing the euro area short-term interest rate with the natural interest rate to assess the stance of monetary policy would lead to a significant bias. In fact, this would imply that unconventional instruments have no effect on the accommodative nature of monetary policy, which clearly does not seem to be the case. To overcome this limitation, an indicator known as the implicit rate (or shadow rate) has been developed. It quantifies the effect of unconventional monetary policies in terms of interest rates. In other words, it is the rate that measures the ECB’s true intervention rate when the policy rate is zero.

For the euro area, Wu and Xia’s (2016) model of the implicit rate is the most widely used. Figure 3 shows that unconventional policies played a significant role in easing monetary policy in the euro area after key rates reached their floor in 2015.

Figure 3: Evolution of the key interest rate and the implied rate in the euro area

Source: ECB, Wu and Xia (2016), BSI Economics

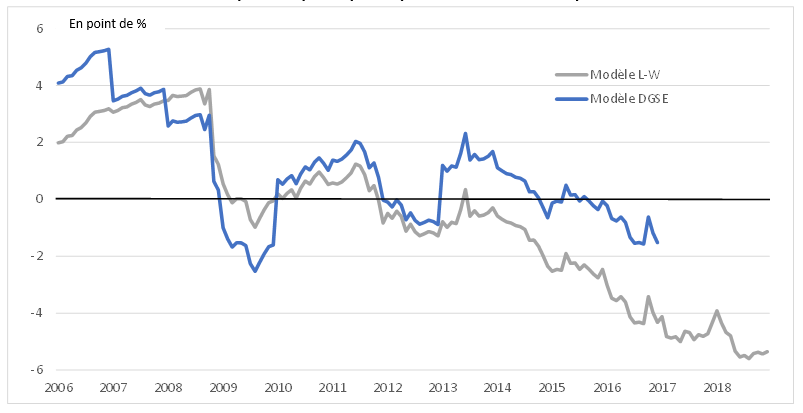

Finally, the implied rate must be compared with estimates of the natural interest rate in order to assess the stance of monetary policy. A positive spread between these two rates signals restrictive monetary conditions, while a negative spread indicates an accommodative monetary policy.

Chart 4: Changes in the monetary policy stance in the euro area:

R (implicit rate) – R* (natural interest rate)

Source: Wu and Xia (2016), Hristov (2016), Arena et al. (2020), BSI Economics

Although the estimates differ in terms of level, the trends remain similar. Monetary policy in the eurozone was accommodative at the height of the 2008 crisis, before fluctuating around the neutral rate over the following six years. At the end of 2014, to combat the deflationary risk that was materializing in the eurozone, the ECB significantly eased monetary conditions by stepping up the use of unconventional instruments (notably through large-scale asset purchases). Until then, it had maintained an expansionary policy to restore inflation expectations, which were considered too far from the target set by its mandate.

Conclusion

The Covid-19 crisis has led the ECB to provide massive support to governments by purchasing a very significant portion of the bonds issued by national governments to finance public support and stimulus measures. These measures are in line with the sharp fall in the natural interest rate[5], which can be explained by an increased imbalance between investment and savings, an unprecedented contraction in aggregate demand, and portfolio reallocations from risky assets to safe assets.

For all these reasons, it seems difficult to argue that the ECB is pursuing an overly expansionary monetary policy. With the natural interest rate likely to remain depressed for the foreseeable future, the ECB has no choice but to commit to maintaining accommodative monetary conditions for several years to come.

Bibliography:

Arena, M et al. (2020) « It is Only Natural: Europe’s Low Interest Rates (Trajectory and Drivers) » IMF, working paper, WP/20/116.

Del Negro, M, Giannone, D, Giannoni, M-P, and Tambalotti, A (2018) “Global trends in interest rates,” NBER working paper 25039.

Eggertsson, G-B, Mehrotra, N-R and Robbins, J-A (2017) “A model of secular stagnation: Theory and quantitative evaluation,” American Economic Journal: Macroeconomics.

Farhi, E and Caballero, R (2015), “The safety trap,” Review of Economic Studies.

Gordon, R-J (2015), “Secular stagnation: A supply-side view”, American Economic Review.

Holston, K., Laubach, T., and Williams, J. C. (2017) “Measuring the natural rate of interest: International trends and determinants,” Journal of International Economics.

Hristov, A (2016) “Measuring the Natural Rate of Interest in the Eurozone: A DSGE Perspective” CESifo Forum, ifo Institute – Leibniz Institute for Economic Research at the University of Munich.

Laubach, T, and Williams, J-C (2003) “Measuring the Natural Rate of Interest,” Review of Economics and Statistics.

Summers, L (2014), “US economic prospects: Secular stagnation, hysteresis, and the zero lower bound”, Business Economics.

Wu, J-C and Xia F-D (2016) “Measuring the Macroeconomic Impact of Monetary Policy at the Zero Lower Bound,” Journal of Money, Credit & Banking.

[1] Secular stagnation is defined by the presence of three macroeconomic characteristics that are simultaneously at work over several years, namely: a regime of low growth, low inflation, and low or zero interest rates (see: https://bsi-economics.org/images/articles/stagnasecuzepylf.pdf).

[2] An increased preference for risk-free assets, leading to a « safety trap » situation, can have a negative effect on the natural interest rate when this situation occurs at the zero lower bound. « The interest rate, which is supposed to bring about the adjustment, can no longer do the job. Instead of having virtuous balancing mechanisms through lower interest rates, a perverse balancing mechanism comes into play, as the adjustment is achieved through a more or less lasting reduction in production. »

[3] Rising inequality concentrates resources within deciles with a very high propensity to save and creates an overabundance of savings.

[4] Increased by Bayesian-type estimates.

[5] The first available results (estimated by the Holston-Laubach-Williams model (2017)) suggest that the natural interest rate fell by 0.7 percentage points in the United States and 0.3 percentage points in the euro area in the first quarter of 2020 alone.