Summary:

– The creation of the Eurozone contributed to the rapid development of trade between its members.

– Germany is the driving force behind the boom in intra-zone exports; it occupies a dominant position in a network of trade relations that is strongly influenced by geographical proximity.

– After rapid growth in the early years of the Eurozone, this boom in intra-zone trade has been held back for several years by powerful macroeconomic adjustments within the Economic and Monetary Union.

– Despite the power of these adjustments, sector dynamics remain decisive.

A country’s economic relations are greatly influenced by its geography and are therefore generally dominated by its trade with its neighbors. This proximity effect has been reinforced by the establishment of economic unions, such as the Eurozone, which has provided its members with a common currency and facilitated their economic and financial exchanges. This phenomenon is less pronounced among the three major leaders (China, the United States, and Germany) in terms of global trade volume, which have more geographically diversified trade relations than their continental partners. However, they play a leading role in the dynamics of trade in their regions, as is the case with Germany in the Eurozone.

After participating in the global trend towards denser trade, the Economic and Monetary Union (EMU) is now undergoing significant changes. While the eurozone, and Germany in particular, is recording record trade surpluses with other countries, intra-zone flows are evolving in a very chaotic manner. We will discuss the drivers of these changes, which involve macroeconomic and sectoral mechanisms within an area that has become fragmented during the crisis.

1 – The establishment of the Eurozone, a catalyst in a region in step with the intensification of international economic exchanges

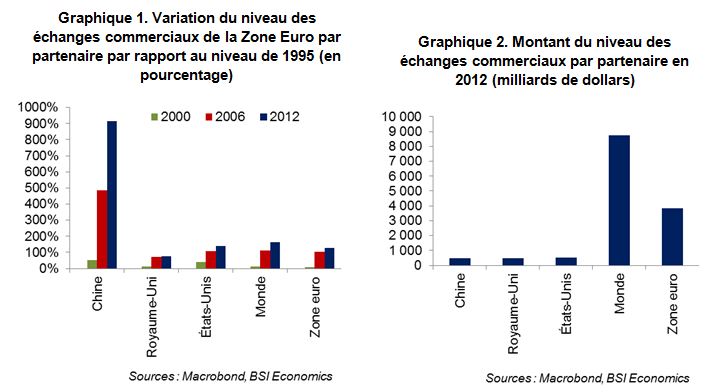

Trade relations between Eurozone countries have undergone profound changes over the past two decades. First, in terms of volume, they have increased. From 1995 to 2012, trade between EMU member countries increased 2.3-fold. This growth was not linear and was particularly concentrated in the early years after the creation of the eurozone; intra-zone trade doubled during this period, after a phase of slow growth in the late 1990s.

However, this phenomenon is not unique to the eurozone: global trade increased more than 2.5-fold between 1995 and 2012. Most eurozone countries have also seen greater growth in their relations with countries outside the eurozone than with their EMU partners. This is largely due to the growing importance of emerging countries, led by China, in the global export market, which started from a relatively low level. In terms of value, intra-zone trade remains predominant: in 2012, 44% of Eurozone countries’ trade was with their partners, compared with 51% in 1995.

Since the onset of the financial crisis, followed by the sovereign debt crisis, trade between eurozone countries has become more heterogeneous. This was not the case in previous periods, when trade growth rates, although not equal, showed the same phases of slowdown or acceleration. Thus, if we analyze import-export data by country, we see that all Eurozone members have experienced a significant increase in trade with their monetary partners since the mid-1990s.

This was particularly true at the beginning of the 2000s, when the creation of the eurozone boosted trade growth among its members. To see this, we need only look at the growth in trade between eurozone countries and compare it with the growth in trade with countries such as the United States or the United Kingdom. Since 2000, the figures show that intra-zone trade has grown more rapidly, which was not the case in previous years. Over the period 2000-2006, intra-zone trade grew by 88%, while trade between the eurozone and the United Kingdom (+55%) and the United States (+49%) was less vigorous. The removal of exchange barriers has therefore made a real contribution to intra-zone trade development.

2 – German exports: the driving force and transmission belt in the euro zone

It has been said that countries naturally tend to forge economic ties with their neighbors. This is the case in Europe. Portugal’s main trading partner is Spain. Spain’s main trading partner is France. And France’s main trading partner is Germany, which is also the main trading partner of Italy and the Netherlands. At the crossroads of Europe’s major continental and maritime trade routes, Belgium has close ties with its German, Dutch, French, and British neighbors. As for Ireland, the United Kingdom is its leading partner.

Due to its geographical position, although it did not join the Eurozone, the United Kingdom remains an important partner in the foreign trade of its EU partners, including its neighbors France, the Netherlands, Belgium, Ireland, and Germany.

In addition to this proximity factor, there is another constant in the external relations of the Eurozone countries: Germany. In addition to the size of its economy and its central position in Europe, its high openness rate (the openness rate is half the sum of exports and imports relative to gross domestic product) and its export capacity make it a privileged partner for most members of the eurozone. Germany is thus the leading intra-zone trading partner for several EMU members (France, Italy, the Netherlands, Austria, Greece, Luxembourg, Slovakia, and Slovenia). Its exports account for more than a quarter of the intra-zone total (compared to only 12% for France, or less than half).

With its dominant position in intra-zone trade, Germany is also the driving force behind the Eurozone’s external trade. In 2012, nearly 37% (compared with 12% for France, or less than a third) of the eurozone’s exports to other regions came from Germany, making it the primary recipient of slowdowns or accelerations in global demand, just as the United States and China are in their respective regions.

3 – Intra-zone rebalancing: constrained in the short term by the crisis, perpetuated in the medium term by reindustrialization?

We have seen that the first part of the 2000s was marked by a significant increase in trade between Eurozone members, driven by domestic demand in several countries with strong nominal growth and by the unsustainable debt dynamics of their private agents. While this period saw a general and massive increase in intra-zone import and export flows, some countries benefited from the establishment of economic and monetary union to gain market share (Germany and the Netherlands in particular) and improve their trade balance with their partners.

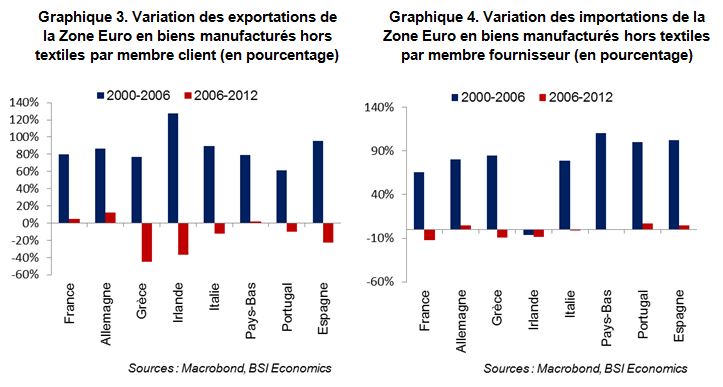

Others, however, saw their external accounts deteriorate (France, Italy, Spain, Greece, Portugal, and Ireland). with the exception of Ireland (whose current accounts were impacted by income from foreign assets but which had retained a significant export capacity), this was due to their low level of industrialization and the substitution of imported goods for domestic production.

Despite this substitution effect, the euro and its impact on the cost competitiveness of European countries under a fixed exchange rate regime cannot be held solely responsible for the deindustrialization of countries with large trade deficits, which began before the introduction of EMU. On the contrary, the integration of certain economies into the euro area has enabled them to be present in a large market. For example, Greece’s exports of manufactured goods to other euro area member countries doubled between 2000 and 2006, whereas they had been declining between 1995 and 2000. If we look at the corresponding figures for Austria (which has a similar GDP but is not experiencing any particular problems today), we see that growth was roughly the same over these two periods. The differences in the production of exportable goods (in the case of manufactured goods, this difference is a multiple of between 7 and 8 between the two countries) therefore predate this.

Since 2007, the eurozone has been plunged into a multifaceted crisis that has had a brutal impact on economic and financial exchanges between its member economies. Despite this, intra-zone trade continued to grow between 2006 and 2012, albeit at a moderate pace (+12%, compared with 88% between 2000 and 2006). In addition to this slowdown, there are several differences compared to previous periods: there is significant heterogeneity between countries and, for some countries, divergences between the evolution of their imports and exports, which was not the case before. These divergences stem from differences in economic growth, unemployment, and wage growth.

From 2006 to 2012, four countries saw a decline in their imports from the euro area: Spain, Greece, Portugal, and Ireland. These are the four countries that had accumulated the largest current account deficits as a proportion of their GDP in the years leading up to the crisis. These are also the four countries whose economies have experienced a significant decline in unit labor costs in recent years. Their recent import surpluses have therefore undergone rapid adjustment in a context of deleveraging by their public and private economic agents, which is dampening domestic demand. Financed at low cost in the early 2000s by capital from their partners, companies and households benefited from very low real interest rates in countries with high inflation, thanks to the emergence of a European money market that allowed the trade surpluses of certain countries to be recycled into financial flows to peripheral countries and facilitated the use of debt by their private agents.

On the export side, the recovery is slow; opportunities are relatively limited in a European economy that is struggling to rebound, and the transformation of price competitiveness gains into exportable production capacity is gradual. The recent recovery in Spanish exports and their very positive contribution to economic growth are helping to rebalance intra-zone trade, although this has not yet been achieved. Indeed, the return to balance in the external accounts of several eurozone countries has required the support of global demand outside the eurozone (as well as a slowdown in their imports, as we saw above); in terms of intra-zone trade, imbalances remain. This benefits Germany in particular, which plays a central role in the issue of rebalancing trade in Europe.

Its openness makes it sensitive to external demand cycles and shocks (in Europe and the rest of the world). While the eurozone is going through a period of economic slowdown, Germany has been able to generate new sources of growth by finding outlets for its exports outside the eurozone and by boosting domestic demand in recent quarters, which had been growing very slowly since the early 2000s. The process of deleveraging by public and private entities currently underway in Europe is a major obstacle to economic recovery, so German demand is also an important source of growth for its neighbors.

4 – Beyond the consequences of the crisis, the evolution of each sectoral component has its own determinants.

In addition to macroeconomic factors, the evolution of intra-zone trade flows also responds to sectoral dynamics. In this respect, while the crisis does not appear to have disrupted the main underlying trends of the past two decades, it has not been without consequences.

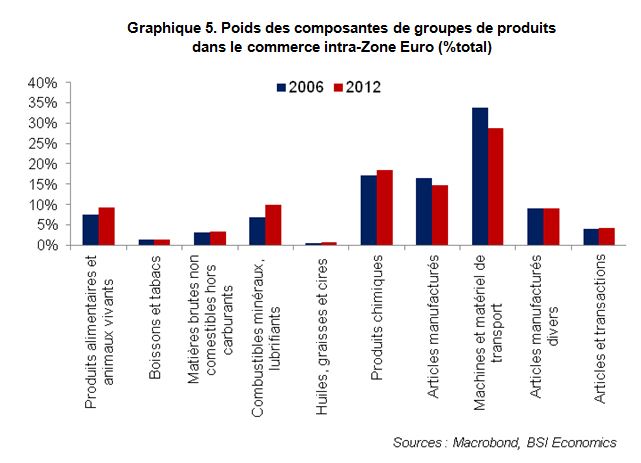

Faced with the emergence of new, rapidly expanding markets, the gradual decline in the share of manufactured goods in intra-zone trade continued after 2006, in line with the previous decade. However, this component remains very important in most eurozone countries. This is particularly the case in Finland (more than 45% of its exports go to its partners) as well as in Italy, Austria, and Portugal.

Among these new intra-zone export markets, there has been a rise in the importance of mineral fuels and related products (oil and oil products, natural and manufactured gas, electrical energy), which now account for 10% of intra-zone trade, thanks in particular to significant price effects. The Netherlands, Belgium, Greece, and Finland are among the best-positioned countries in this regard.

Similarly, the increase in the weight of chemical products (medical and pharmaceutical products, plastics, fertilizers, etc.) has been notable in recent years (+6.5 points, from 13% to 18.5% of intra-zone trade between 1995 and 2012). This item is predominant in Ireland’s accounts (it accounts for 63% of imports from Ireland to Eurozone countries) and has become significant in most Eurozone countries.

Certain segments of the export market are more or less elastic in terms of prices and/or agents’ incomes, which seems to have caused certain items to deviate from their natural weight in the trade accounts of Eurozone countries. For example, the share of food products has increased in the exports of several countries positioned in this segment, thanks to this component’s resistance to economic cycle variations: this is particularly the case in France, Spain, Belgium, Greece, and the Netherlands.

Conversely, the export markets for machinery and transport equipment are experiencing unprecedented weakness (albeit relative, since they still account for more than a quarter of intra-zone trade) in terms of volume. In terms of their weight in foreign trade with the eurozone by country, there has been a decline among all the main players in intra-zone trade: Germany (-2.4 points from 2006 to 2012), France (-5.9 points), Italy (-5.1 points), Spain (-8.8 points), and the Netherlands (-5.8 points). Sensitivity to cyclical movements in investment purchases of equipment and machinery partly explains this significant decline.

Countries are not equal when it comes to variations in production costs and exchange rates. The resilience of German exports stems in part from its positioning at the high end of the market, which gives Germany strong non-price competitiveness, which is not the case for peripheral economies and France in particular. Conversely, Spain’s gains in export market share are now mainly due to an improvement in its price competitiveness, which is benefiting from the readjustment of wage costs.

Conclusion

The current slowdown in economic exchanges between Eurozone countries after rapid growth in the early 2000s is the result of powerful macroeconomic adjustments. In the short term, the determinants of these adjustments (wages, private debt reduction, etc.) are a tool for rebalancing intra-zone flows. In the medium term, the continuation of this rebalancing depends on the positioning of each economy in segments of the European export market. The size of this export market (more than €2 trillion per year in intra-zone trade) and its diversity offer vast opportunities for Eurozone members.