Usefulness of the article: This article reviews the ECB’s quantitative easing reinvestments. It presents the various rules put in place and the role of the capital key in the institution.

Summary :

- The ECB ended its quantitative easing (QE) program in December 2018 but will reinvest the proceeds from its program to maintain the size of its balance sheet unchanged.

- The aim of this extension is to achieve 2% inflation in the eurozone and to maintain downward pressure on eurozone government bond yields.

- Reinvestments follow clearly defined rules. The rules put in place during the purchases also continue to apply.

- Compliance with the allocation key is also an important factor, as it is the source of this program’s legitimacy.

The European Central Bank (ECB) has a single objective: inflation slightly below 2% in the eurozone. In the wake of the 2008 crisis, the ECB sharply lowered its key interest rates to stimulate the economy. When key interest rates fall, businesses invest more and households borrow at lower cost, which stimulates investment and consumption and, therefore, growth.

However, once the key interest rate reaches 0%, it is in principle impossible to lower it further. To prolong this rate cut despite this, the ECB has used an unconventional monetary policy tool: quantitative easing (QE), officially known as the Asset Purchase Program (APP).

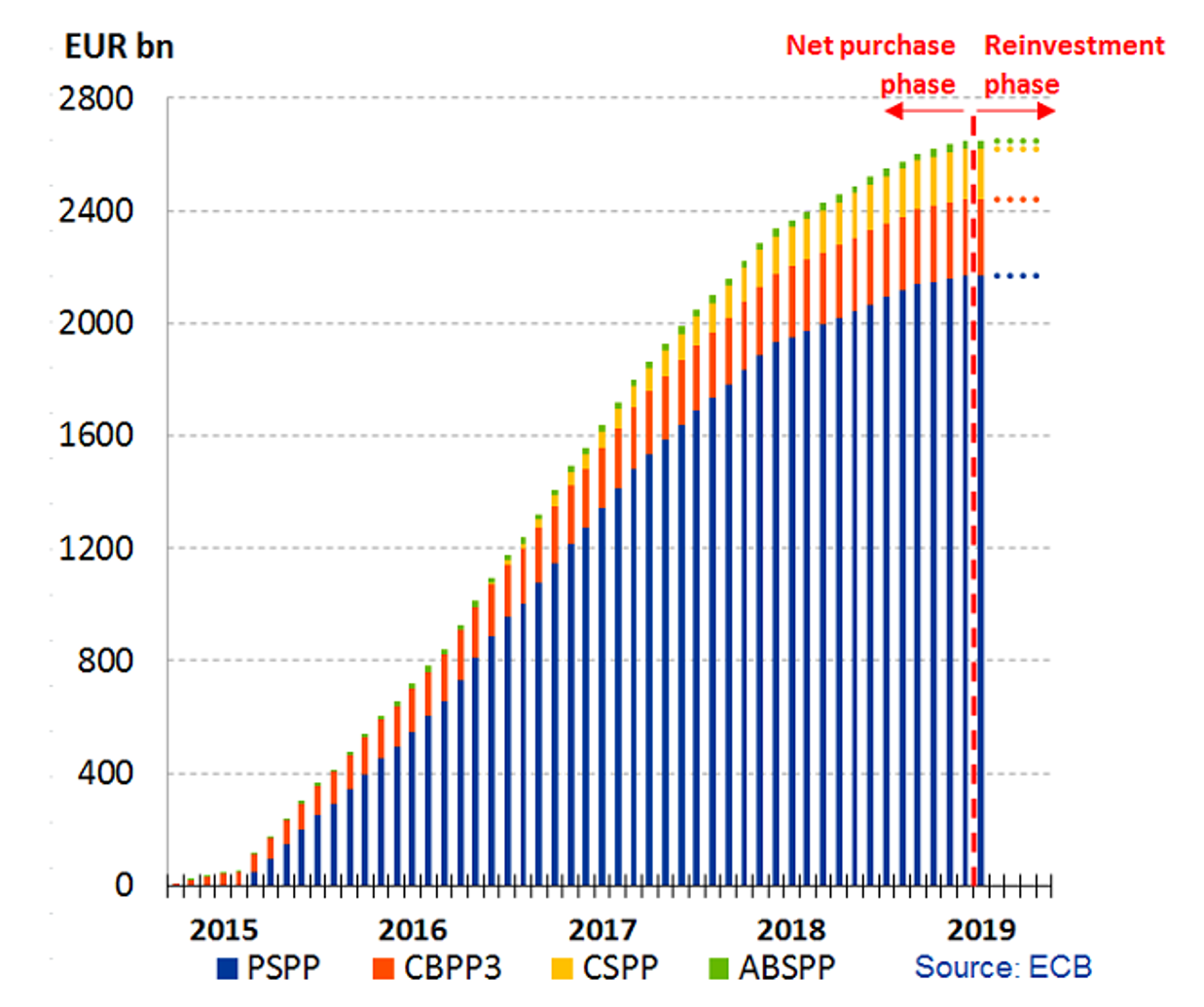

Launched in March 2015, the APP is a measure under which the ECB has purchased various types of financial assets through a number of dedicated programs: the Public Sector Purchase Program (PSPP), the Asset-Backed Securities Purchase Program (ABSPP), the third covered bond purchase program (CBPP3), and the corporate securities purchase program (CSPP). The most significant of these purchases is that of government bonds and bonds issued by supranational and public agencies, known as the PSPP (Public Sector Purchase Program). Between March 2015 and December 2018, the ECB purchased these securities every month on the financial markets for a total of €2.6 trillion.

Maintaining the size of the balance sheet

Since January 2019, the ECB has not been buying back assets on the financial markets but has been « reinvesting maturities. » This means that when a bond held by the ECB matures, the Frankfurt-based institution will buy another bond on the market with the money received at the time of redemption. As a result, the central bank’s balance sheet will stop growing but will remain unchanged as long as the repayments of maturing bonds are used in full to purchase other securities. In doing so, the ECB is prolonging the positive effects of its program on inflation in the eurozone.

Inflation in the eurozone has risen but is still far from the 2% target: the European Commission forecasts inflation of 1.4% in 2019 and 1.5% in 2020. The ECB must therefore continue to support the eurozone economy and extend its accommodative policy. Reinvesting all of the repayments received also allows the ECB to stabilize demand on the sovereign debt market, in particular to avoid a rise in borrowing costs for heavily indebted eurozone countries.

The ECB will therefore reinvest €128 billion in sovereign bonds and €28 billion in bonds issued by supranational and European agencies (such as the European Investment Bank, for example). By way of comparison, the ECB purchased approximately €230 billion under the PSPP in 2018.

Reinvestments

Reinvestments follow clearly defined rules: first, the ECB is applying the same rules it imposed on itself when making QE purchases:

- purchases were made in proportion to each country’s share in the ECB’s capital;

- the ECB could not hold more than 33% of a country’s debt stock or more than 33% of the total amount of a bond;

- Purchases could be made on securities with a maturity of more than one year and less than 30 years.

In addition to extending these measures, the ECB has introduced new constraints that must be respected, in particular:

- Repayments are reinvested in the same jurisdictions, i.e., a maturing bond must be replaced by another bond from the same country. A maturing German bond cannot be replaced by a Spanish bond, for example.

- When an asset purchased under the APP matures, it must be reinvested within 12 months, compared with three months during the purchase phase. This extension eases the constraints on national central banks, which purchase securities on the financial markets on behalf of the ECB.

- The size of cumulative net purchases in each APP program will be maintained at their respective levels at the end of December 2018. In other words, a maturing sovereign bond (PSPP) cannot be reinvested to purchase corporate debt (CSPP), for example. In 2019, the PSPP will account for 83% of the APP, compared with 11% for the CBPP3 and only 3% for the CSPP.

Cumulative APP purchases, by program

However, the ECB has not provided any details on the average maturity of its reinvestments. It may therefore use repayments of short-term securities to purchase longer-term securities in order to maintain downward pressure on long-term rates, as the Fed did with its « Twist » operation*.

The ECB has also not indicated the duration of its reinvestments. However, this should depend on the progress of inflation in the eurozone towards the 2% target. By way of comparison, the US Federal Reserve (Fed) reinvested all securities redemptions for three years after the end of its purchase program. The Fed then partially reinvested the repayments to gradually reduce the size of its balance sheet, thereby avoiding excessive market volatility.

The ECB’s capital key

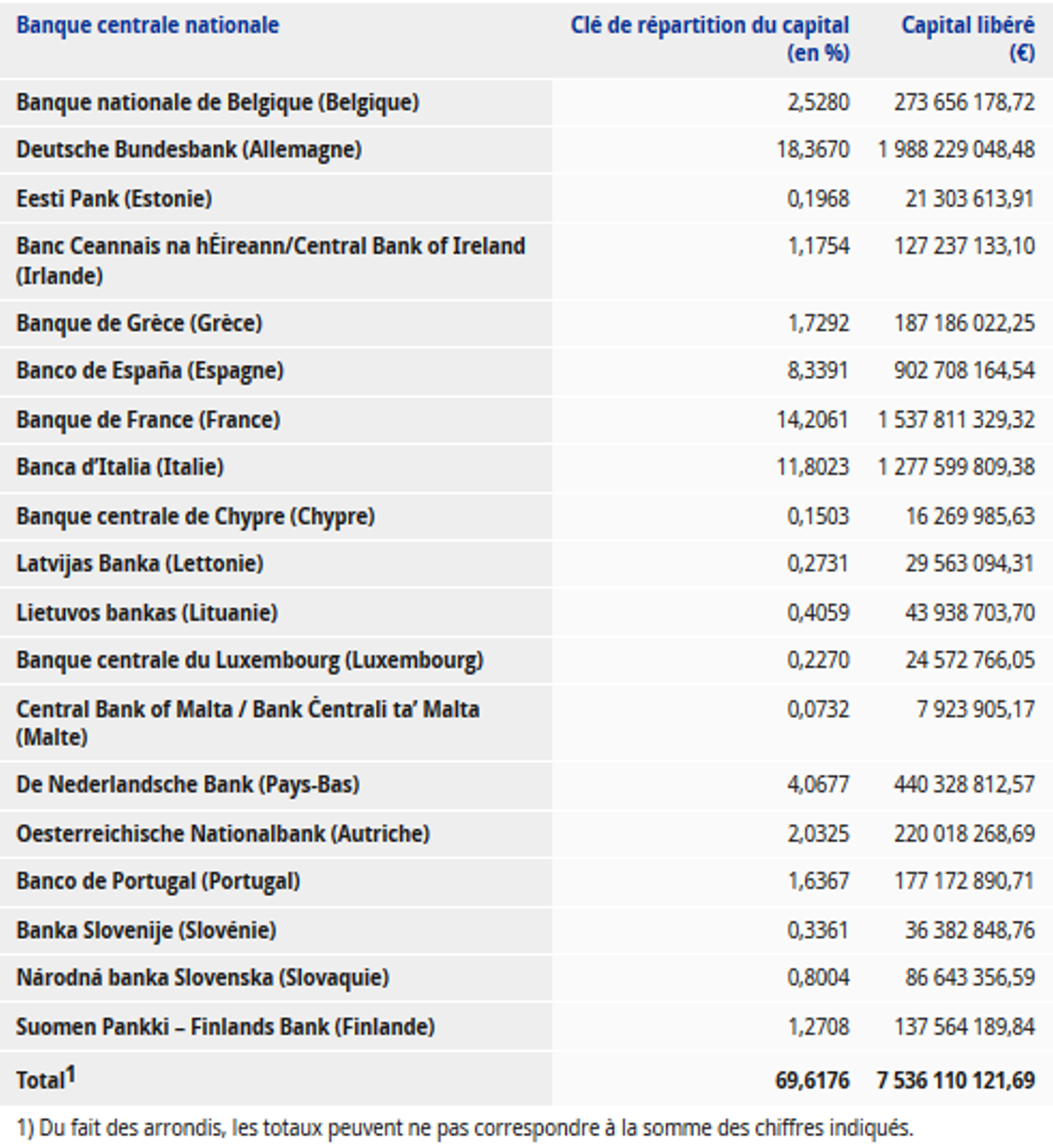

The ECB’s capital key is a key legal element of the ECB’s quantitative easing program and reinvestments. The Court of Justice of the European Union (CJEU) confirmed the legitimacy of the APP, in particular because the distribution of securities purchases respected the capital key. This key also governs the distribution of profits that the institution pays to national central banks.

Contributions of euro area NCBs to the ECB’s capital:

Source: European Central Bank

Contributions of non-euro area NCBs to the ECB’s capital:

Source: European Central Bank

The national central banks’ shares in the ECB’s capital are calculated on the basis of a key reflecting the share of the different countries in the population and GDP of the European Union. These two data are weighted equally. The ECB revises these shares every five years and when a new country joins the European Union.

It may seem surprising that countries outside the euro area participate in the ECB’s capital. In fact, the nine national central banks of non-member countries contribute to the ECB’s operating costs because of their participation in the European System of Central Banks. They do not receive a share of the profits and did not benefit from the APP.

The distribution was revised last December to take into account changes in the relative economic and demographic weight of each country: France and Germany gained slightly in importance, while Italy lost ground. Proportionally, reinvestments will therefore be higher in German securities and lower in Italian bonds, which could put upward pressure on Italian yields.

The ECB has strongly emphasized compliance with the allocation key when reinvesting. However, redemptions must be reinvested in the same jurisdiction. Given the current gap between the ECB’s portfolio and the capital allocation, it therefore seems impossible for the institution to follow both rules at the same time. The solution may lie in the debt of supranational institutions such as the European Stability Mechanism (ESM) or the European Investment Bank (EIB): as they do not belong to any country by definition, the ECB could reinvest their repayments in sovereign securities (under the same program, the PSPP) so that the securities portfolio effectively complies with the distribution key.

Conclusion

Faced with slowing growth and insufficient inflation in the eurozone, the ECB has decided to end its quantitative easing program while extending its effects. On Thursday, March 7, ECB President Mario Draghi even postponed a potential rise in key interest rates and announced new measures to support eurozone banks, known as TLTRO III**.

*Fed’s Operation Twist: the Fed replaced short-term securities in its portfolio with long-term securities in order to lower long-term interest rates, causing the yield curve to flatten. This allowed the Fed to increase the effects of its monetary policy without further increasing the size of its balance sheet.

**TLTRO III (Targeted longer-term refinancing operations): the ECB’s third wave of loans to eurozone banks on very favorable terms (i.e., at very low rates). These operations will take place every quarter between September 2019 and March 2021 and will have a maturity of two years. Their aim is to ensure the effective transmission of monetary policy to the real economy.

Source:

https://www.ecb.europa.eu/mopo/implement/omt/html/index.en.html

https://www.ecb.europa.eu/mopo/implement/omt/html/pspp.en.html