Usefulness: this article aims to understand how the Federal Reserve conducts monetary policy in the United States in a climate of uncertainty linked to trade policy, particularly since Donald Trump’s election. It attempts to explain why the Fed’s independence is now under threat, and why this issue is important from a macroeconomic and financial stability perspective.

Summary :

- At the end of October 2019, the Federal Reserve (Fed) lowered its key interest rate for the third consecutive time in 2019.

- While the US economy is at full employment and inflation is in line with its target, this expansionary monetary policy appears to be a response to weak growth forecasts, which are closely linked to trade tensions with China.

- Accusing the Fed of undermining the competitiveness of the US economy with overly restrictive monetary policy, President Donald Trump has repeatedly criticized the institution and its Chairman, Jerome Powell, since 2018.

- Despite a firm commitment to stick to its dual mandate of full employment and price stability until the summer of 2019, the Fed may have succumbed to growing pressure from the White House by immediately easing its monetary policy, thereby threatening its independence and, ultimately, its role in macroeconomic and financial stabilization.

It is widely accepted that the Federal Reserve plays an important role in the cyclical fluctuations of the US economy. Sometimes adored (for fighting high inflation under Paul Volcker in the late 1970s), sometimes criticized (for Alan Greenspan’s probably overly expansionary monetary policy in the 2000s), the Fed seems to have always conducted its monetary policy in response to changes in inflation and economic activity, in accordance with its mandate. However, the gradual decline in its key interest rate in 2019 came at a time when President Donald Trump was increasing pressure on the institution, even though the macroeconomic environment in the United States was fairly favorable.

In this article, we ask whether the recent implementation of an expansionary monetary policy in the United States stems from political pressure exerted by Donald Trump on the Fed, or simply from poor prospects for the US economy. In this sense, the central question is that of the Fed’s independence: did it act for political or strictly macroeconomic reasons?

Monetary policy in the United States: an overview

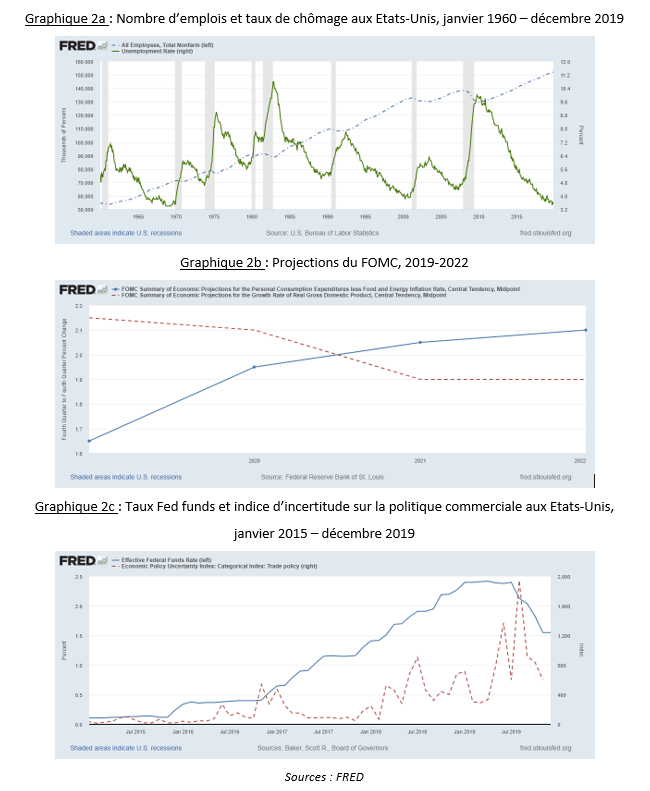

On October 30, 2019, the Federal Reserve (Fed) initiated a third consecutive 0.25 percentage point cut in its key interest rate, which now stands in a range of 1.50% to 1.75%. This cut in the key interest rate comes at the end of a year marked by the continued easing of US monetary policy: an initial cut of 0.25 percentage points in July (from 2.25-2.50% to 2-2.25%), followed by another in September, bringing the rate to between 1.75% and 2%. The year 2019 therefore marked a reversal of monetary policy in the United States, contrasting with the normalization phase observed since December 2015 and the end of the zero interest rate period (the famous » zero lower bound « ) (Chart 1).

Despite a dynamic labor market characterized by strong job creation and the lowest unemployment rate in nearly fifty years (3.5% in December 2019, Chart 2a), the Fed justified its monetary policy easing by citing a slowdown in inflation against a backdrop of disappointing growth prospects (Chart 2b), weighed down by escalating trade tensions between China and the United States. Furthermore, Chart 2c shows that the Fed lowered its key interest rate at a time when the indicator of uncertainty about trade policy[1] in the United States skyrocketed.

While the macroeconomic indicators traditionally targeted[2] by the Federal Reserve show no real signs of weakness, the high level of uncertainty surrounding trade policy and Donald Trump’s pressure on the Fed may have played a role in its decision to ease monetary policy.

Is the Fed’s independence under threat?

Since the summer of 2018, Donald Trump has often openly criticized the Fed’s monetary policy in the United States. In interviews and, above all, in tweets [3], the US president has not hesitated to blame the interest rate hike decided by Jerome Powell, the Fed chairman, even though he was appointed to the post a few months earlier by the White House itself.

According to Donald Trump, the restrictive monetary policy initiated by the Fed at the end of 2017 is a burden on the US economy, penalizing competitiveness and therefore exports through a stronger dollar, as shown in Figure 4.

But for Jerome Powell, the issue is quite different: with the Fed having begun to normalize its monetary policy and macroeconomic performance looking fairly favorable (see previous section), there would appear to be no obvious reason to lower the key interest rate, based on its dual mandate of full employment and price stability. However, this was the decision taken by the FOMC ( Federal Open Market Committee, the « enlarged » committee of Federal Reserve governors) in July 2019, justifying this cut in particular by trade disputes with certain partners (notably China) and weak growth forecasts for the coming years, accompanied by a lack of inflationary pressures on the economy.

A number of factors suggest that the Fed’s decision to ease its monetary policy was influenced by pressure from President Trump as a result of the uncertainty generated by the trade war [4]. If this is true, the Fed would have been politically influenced in its decision, deviating from the objectives stipulated in its mandate. Based on market data, a recent study by the National Bureau of Economic Research explains why the Fed’s independence is indeed considered to be under threat. Using statistical methods to identify high-frequency shocks, the authors find that Donald Trump’s tweets have a strong negative and significant effect on future rate expectations, showing that financial markets assign a high probability to the Fed succumbing to political pressure.

Why the independence of a central bank is essential

In conclusion, it is important to briefly recall why the issue of independence is crucial for a central bank such as the Fed.

Since the late 1980s, and in particular the work of Alberto Alesina ([6a], [6b], and [6c] for example), a large body of academic literature has developed on the macroeconomic impact of central bank independence. By remaining independent, the Fed can focus fully on its objective of price stability and growth, without pressure for expansionary (often inflationary) policies interfering with its decisions. There appears to be a negative correlation between the degree of central bank independence and inflation fluctuations. In other words, the more independent the central bank is, the more credible it will be perceived to be in achieving its price stability objective by anchoring the expectations of economic agents.

More recently, other studies have focused on the links between central bank independence and financial stability. The reasoning is the same: an independent central bank would be more responsive and effective in the face of financial turmoil than if it were politically constrained, for example through a weaker incentive to come to the aid of institutions in difficulty.

Although it is difficult to say for sure, it is likely that the Fed’s independence is being called into question today. However, this situation would be detrimental to macroeconomic and financial stability in the United States, which is undesirable given the global uncertainty threatening the US economy.

Notes and bibliography

[1] Scott R. Baker, Nicholas Bloom, Steven J. Davis, « Measuring Economic Policy Uncertainty, » The Quarterly Journal of Economics, Volume 131, Issue 4, November 2016, Pages 1593–1636, https://doi.org/10.1093/qje/qjw024.

[2] Traditionally, the Federal Reserve looks at three main macroeconomic aggregates when making its decisions: the price index (overall and underlying, i.e., excluding food and commodity prices, which are often highly volatile), real GDP (Gross Domestic Product) growth, and the unemployment rate. Other indicators may also be taken into account in decisions, such as the industrial production index, for example, or the interest rate curve, often considered to be leading indicators of an economic cycle reversal.

[3] On August 23, 2019, Donald Trump posted the following tweet: « As usual, the Fed did NOTHING! It’s incredible that they can ‘talk’ without knowing or asking what I’m doing, which will be announced very soon. We have a very strong dollar and a very weak Fed. I will work « brilliantly » with both, and the United States will be better off… » A few hours later, he posted: « My only question is, who is our biggest enemy, Jay Powell or President Xi? »

[4] Estimates of Taylor-type monetary policy rules augmented with a trade policy uncertainty variable are conducted on monthly U.S. data from January 1985 to November 2019. While the Fed does not appear to have responded significantly across the entire sample, the trade policy uncertainty variable has been significant and negative since Trump’s election, which would confirm that the Fed did indeed lower its key interest rate in response to uncertainty during the Donald Trump era. However, nothing can be said with certainty yet, given the weak robustness of the estimate based on the limited sample from the post-election period (January 2016 to November 2019, i.e., 47 observations), which is one of the main limitations of the empirical result.

The results of the estimates are available on request directly from the author at aymeric.ortmans@univ-evry.fr.

[5] Bianchi, F., Kung, H., & Kind, T. (2019). « Threats to Central Bank Independence: High-Frequency Identification with Twitter » (No. w26308). National Bureau of Economic Research.

[6a] Alesina, A. (1988). « Macroeconomics and politics. » NBER macroeconomics annual, 3, 13-52.

[6b] Alesina, A., & Summers, L. H. (1993). « Central Bank Independence and Macroeconomic Performance: some comparative evidence. » Journal of Money, Credit and Banking, 25(2), 151-162.

[6c] Alesina, A., & Gatti, R. (1995). « Independent Central Banks: Low Inflation at No Cost? » The American Economic Review, 85(2), 196-200.