Abstract:

· Despite sustained growth rates in the early 2000s, Greek economic activity has collapsed and does not appear to be recovering in the short term;

· The country’s economic structure faces a glaring lack of economic diversity, dominated by low value-added sectors;

· Lower labor costs could enable the country to attract foreign investment to diversify its economy;

· Greece’s natural resources (gas and oil) could be the salvation that lifts the country out of its torpor.

After a month of negotiations with its creditors, Greece finally obtained a new tranche of €1.1 billion (compared with the €2.8 billion it had hoped for) from the third bailout plan decided in 2015. This €86 billion plan covers the period 2015-2018, and each tranche is conditional on the progress of Greek reforms (particularly privatization). Creditors have also set specific targets that Greece must meet: a primary surplus of 3.5% of GDP by 2018 and a public debt-to-GDP ratio of 120% in 2022. When considering the feasibility of these targets, we can see how important economic growth is to achieving a public debt ratio of 120% of GDP. This ratio depends on three variables: the primary balance, the implicit interest rate, and nominal growth. A simple calculation, assuming that the interest rate remains at its current level (2.1%), shows that average annual nominal growth of 5.5% would be needed until 2022 to meet these targets.

This approach highlights two conclusions: the Troika’s targets seem disconnected from the Greek economic situation (the OECD forecasts growth of -0.6% for 2016) and appear to be based more on political than economic logic, and growth is essential to resolving the country’s solvency problem. However, this last point is often overlooked in public debate. So how can we assess the country’s growth prospects?

I) The collapse of Greek growth

Before the 2008 crisis, Greece experienced growth rates above the European Union average. The country initially benefited from European redistribution mechanisms and the effects of convergence following its entry into the EEC in 1981. Subsequently, its entry into the eurozone in 2001 boosted domestic demand through lower interest rates. The 2008 financial crisis brought the country’s momentum to a screeching halt. And in 2010, the sovereign debt crisis plunged the country into recession: austerity measures eroded domestic demand, unemployment skyrocketed (reaching 27.9% in July 2013) and bank interest rates soared.

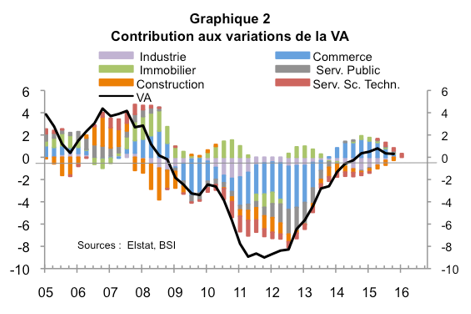

To analyze Greek growth, we start with the method of calculating GDP as the sum of value added. We thus study the Greek economy by sector of activity. The country’s economic structure makes it one of the least diversified in the European Union: three sectors account for more than 60% of GDP (trade, public services, and real estate (Figure 1)).

A poorly diversified structure

The Greek economy specializes in sectors with low added value:

· The service sector dominates, boosted in particular by dynamic tourism. According to The World Travel & Tourism Council, tourism contributed 17% of GDP in 2015 and accounted for 19% of the workforce. As tourism was not significantly impacted, real estate activities were able to weather the crisis. While domestic trade collapsed as a result of falling purchasing power (the main contributor to the Greek recession (Figure 2)), tourist consumption remains high. Nevertheless, Greece is unable to capture the full value added generated by the tourism sector, as the presence of foreign players remains strong and is increasing. Furthermore, dependence on a low value-added sector such as tourism highlights the vulnerability of the Greek economy.

Greece’s other area of specialization is the merchant navy. Its geographical position (close to the Suez Canal) and low tax rates are key assets for the country. Greece is therefore an important transit hub and has become a stronghold for oil refining.

The secondary sector remains weak: Greek industry accounts for only 10% of GDP, thethird lowest rate in the European Union, behind Luxembourg and Cyprus. Two-thirds of industrial production is focused on agri-food, oil refining, and base metal processing. The level of sophistication is low, and the low level of investment in R&D (0.8% of GDP in 2015) does not bode well for an increase in sophistication.

The primary sector is not very productive: it contributes 5% to growth and employs 13% of the working population. The country is Europe’s leading tobacco producer and the world’s fifth largest cotton producer. Aquaculture production is also growing.

Beyond this sectoral breakdown, Greece is characterized by an extremely high weight of public services compared to other OECD countries. It is interesting to note that despite austerity, the share of public services has increased since 2000 (from 20% in 2000 to 22% in 2014).

As shown in Figure 2, the tertiary sector has logically contributed most to the collapse in growth. Under the effect of declining resources, linked to the economic crisis and austerity, trade has fallen sharply, but is experiencing a slight recovery, thanks in particular to the decline in unit labor costs. Construction and public services have also been severely affected. Real estate appears to be the only sector to have truly weathered the storm.

II) Outlook: the end of a tragedy?

This analysis of the Greek economic structure paints a bleak picture: the economy is dominated by low value-added activities, and weak investment and R&D are preventing it from moving upmarket, against a backdrop of unsustainable austerity that is undermining domestic demand. However, there are several reasons to hope for a return to sustained growth and stronger integration into the European value chain in the long term.

Improved price competitiveness

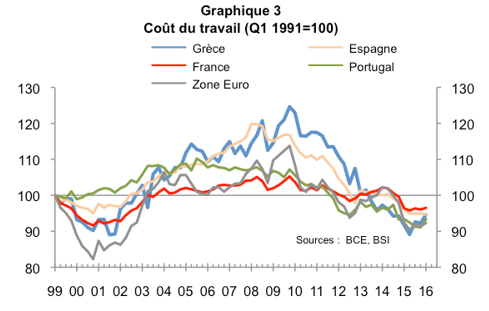

Firstly, while austerity appears to be an economic and social disaster for Greek households and businesses, it has, on balance, led to a reduction in labor costs (Figure 3) and thus to greater price competitiveness. The country has historically been characterized by low inward FDI (9.1% of GDP in 2015), as a result of high labor costs, bureaucratic red tape, and a lack of infrastructure. However, Greece appears to have made progress on these last two points, according to the World Bank’s 2016 Doing Business study. Thus, while these gains in price competitiveness, combined with improved trading conditions, do not currently translate into increased attractiveness, this trend could reverse.

Indeed, the decline in labor costs has been relatively sharp in the manufacturing sector (an 18% drop in unit labor costs between 2010 and 2016 in industry). At the same time, the privatization of Greek public monopolies by foreign companies is creating competition in certain sectors (ports, real estate, airports) and should make it possible to modernize infrastructure and, above all, attract foreign firms back to the country. Like Portugal and Eastern European countries, Greece could take advantage of the decline in its unit labor costs to attract investors in low value-added sectors, particularly in industry. Greece’s geographical position (close to the Suez Canal, the gateway to trade with Asia) gives it an interesting comparative advantage, which is combined with the country’s maritime power.

Hydrocarbons as an Eldorado

Another growth opportunity lies in the hydrocarbon sector, in two ways. First, Greece experienced an explosion in its hydrocarbon trade after 2008 (exports increased more than fivefold between 2008 and 2012). The country imports crude oil, refines it, and then exports it. Hydrocarbon trade accounted for around 40% of the country’s imports and exports. Half of these hydrocarbon imports come from Russia and a quarter are then exported to Turkey. In addition, the Turkish Stream gas pipeline project between Russia and Turkey is expected to be extended to Greece, thereby strengthening energy ties with these two countries. Greece is also seeking to diversify by turning to the Middle East, particularly Iran. Before 2012, Iran was an important partner for Greece and is expected to become the gateway for Iranian oil to Europe with the end of the embargo, as evidenced by diplomatic meetings between the political leaders of the two countries. The geographical proximity of the Suez Canal could make Greece the platform between these countries and the rest of Europe.

Secondly, Greece could benefit directly from hydrocarbon production. The country appears to be sitting on a veritable treasure trove: oil and gas deposits in the Mediterranean. A 2012 study estimated that the subsoil off the Greek coast (south of Greece and towards Lebanon) could bring in €464 billion over the next 25 years for the country in gas alone. In addition, in 2014, the country signed three agreements with Greek and foreign companies for the exploration and exploitation of oil deposits in the Ionian Sea. The country hopes to generate €150 billion in tax revenue over 30 years. If these gas and oil exploration efforts prove successful (the initial results are optimistic), Greece could generate a trade surplus and significant tax revenue, potentially triggering a cycle of growth.

Conclusion

So, while Greece may have to wait a while before returning to sustainable, robust growth and regaining its pre-crisis economic momentum, it still has significant growth potential. Under the yoke of austerity, the lack of diversity in the Greek economy has been fatal for many companies. One of the few « positive » consequences of this austerity is certainly the reduction in labor costs, which could, in the long term, lead to a return of foreign investment. Above all, if the prospects for exploiting its subsoil resources prove to be true, Greece could be sitting on a gold mine. But as with any producing country, the objective will be to impose national companies in order to capture the maximum revenue from these activities, despite the sharp increase in the buyout of entire sections of the Greek economy by foreign economic players.

Bibliography

« 10 things you need to know about the Greek economy, » 2015, ERBD

« Greece: is a favorable outcome to the negotiations possible in the short term? », 2016, J. Castillo, V. Guiet – Natixis

« Greece: Economic Outlook 2016, » 2016, OECD

« Travel & Tourism: economic impact Greece 2015, » 2015, World Travel and Tourism Council

« Is Greece the Norway of tomorrow? », 2012, La Tribune

« Greece’s foreign trade in 2015, » 2016, Public Treasury

« Greece soon to be the queen of oil, » 2014, La Tribune

« What is the Greek economy based on? », 2014, Le Figaro