Abstract:

- Information asymmetries have a negative impact on the functioning of markets, particularly in insurance markets.

- Many characteristics of the contracts offered can be explained by the existence of information asymmetries.

- Recent empirical research has made significant progress in assessing the importance of asymmetries in specific insurance markets.

- While they have a minor impact on certain types of insurance, such as auto insurance, they cause significant malfunctions in other markets, such as long-term care insurance. On their own, they can explain the (almost) total absence of certain markets, such as private unemployment insurance.

Keywords : insurance, information asymmetries, public intervention, market imperfections, adverse selection, moral hazard

In 1970, in an article entitled « The Market for Lemons, » George Akerlof (winner of the 2001 Nobel Prize in Economics) revolutionized economic theory by highlighting the negative consequences that information asymmetries can have on the functioning of markets.[1] Information asymmetry, as its name suggests, refers to a situation in which two agents have different information. More specifically, in the field of economics, information asymmetries occur in a trading situation when some agents have more information than others about certain elements relating to the potential trade.[2]

Information asymmetries affect the functioning of many markets and can justify public intervention in many areas. This is particularly the case in insurance markets. For example, many features of insurance contracts can be explained by the presence of information asymmetries: deductibles, bonus-malus systems, different coverage rates, etc. Furthermore, as we shall see, information asymmetries explain why insurance companies refuse to offer certain types of insurance to certain types of people, as in the case of private long-term care insurance. Finally, they alone can explain the absence of certain markets, such as private unemployment insurance.

Information asymmetries, functioning and characteristics of insurance markets: an illustrative example

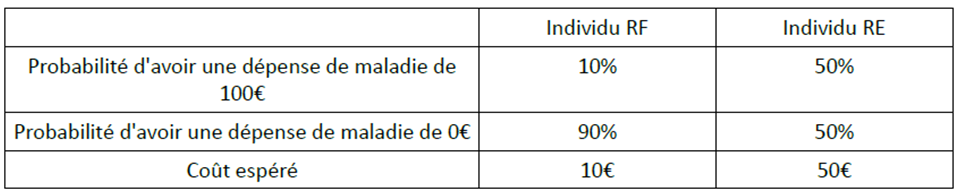

Let’s start with an example illustrating the negative effect of information asymmetries on an insurance market.[3] Let’s imagine a situation, summarized in the table below, where there are two types of individuals. The « low-risk » individual or LR has a 10% probability of incurring a healthcare expense of €100 and a 90% probability of incurring a healthcare expense of €0. The « high-risk » individual or HR has a 50% probability (>10%) of incurring a healthcare expense of €100 and a 50% probability of incurring a healthcare expense of €0. We are therefore in a situation where the LR individual has less risk of incurring a healthcare expense than the HR individual. The expected cost of healthcare expenses is 10%*€100 = €10 (respectively 50%*€100 = €50) for the LR individual (resp. HR). If they are aware of their characteristics and are risk-averse, i.e., if they want to insure themselves against risk, they will be willing to pay an insurance premium of more than €10 (or €50) to have access to insurance that fully covers them in the event that they incur €100 in healthcare expenses. Of course, above a certain insurance premium threshold, they will not want to be covered. For example, it is reasonable to assume that in the above case, the RF individual will not want to take out insurance if the premium offered is €30, i.e., three times more than their expected healthcare expenses.

The case without information asymmetries. If an insurance company can observe who is RF-type and who is RE-type, then it can offer two different contracts for each type. In the absence of administrative costs and margins[4], the insurance company will offer the RF type individual a contract for which the premium will be equal to 0.1*€100 = €10 and which will cover him up to €100 in the event that he falls ill. For the RE-type individual, it will offer a contract with a premium of 0.5*€100 = €50, which will cover them up to €100 in the event that they fall ill. Each individual will benefit from having access to these insurance policies: indeed, RF (or RE) individuals are willing to pay more than $10 (or $50) for insurance.[5] Ultimately, this situation is characterized by the existence of contracts covering all the risks faced by individuals but sold at different prices depending on the risk of the individuals (which is observed by the insurance company).

The case with information asymmetries. Now , let’s consider the case where individuals always know their type but where the insurance company cannot observe who is RF or RE. Let’s make an additional assumption that the insurance company knows that 50% of the population is RF and 50% is RE.[6] This is a case of information asymmetry: a potential policyholder knows exactly whether they are RE or RF, while the insurance company only knows that this person is just as likely to be RE as RF. The potential policyholder therefore has more information than the insurance company. What happens then? One might think that the insurance company would start by offering each customer a policy with €100 coverage in the event of illness for a premium of 50%*(€10) + 50%*(€50) = 5 + 25 = €30 in order to cover its costs. However, a premium of €30 may be considered too high by RF-type individuals (for whom the « fair » premium is €10), and they are likely to decide not to purchase the insurance. In this case, the only people who will want to insure themselves at this price are RE-type individuals. If this is the case, the insurance company will ultimately have to offer a single contract with a premium of €50, as it would make a loss by covering only these individuals with a premium of €30. This is a case of » adverse selection, » where information asymmetry creates a situation where only high-risk individuals decide to purchase the insurance contract that is offered.

Information asymmetries and inefficiency. Herewe see that individuals (those of the RF type) who would like to insure themselves for €100 at a « fair » price (i.e., equivalent to the average cost of their healthcare expenses) and above (but up to a certain point) are no longer insured. At the same time, others (those of type RE) have the same insurance as in the case without information asymmetries. The situation of individuals of type RE is therefore identical to that without information asymmetries, while the situation of individuals of type RF has worsened. Here we see the negative effects of information asymmetry on the functioning of markets.

Until now, we have (implicitly) assumed that the insurance company only adjusts the insurance premium (its price) and not the level of reimbursement in the event of medical expenses (its quantity) in the event of information asymmetries. In reality, it can change both parameters simultaneously. It can be shown that, in this case, a contract that would be attractive to the RF-type agent will always offer incomplete coverage at equilibrium. This is because a contract with full coverage sold at an attractive price to an RF individual would also be attractive to an RE agent. As shown above, this would increase the insurance premium by €30, ultimately making it unattractive to RF agents.[7] We can therefore see that the existence of information asymmetries can explain the existence of incomplete insurance policies. Furthermore, they can explain why, in some cases, the unit price of insurance, i.e., the amount of the premium per euro covered, is higher when the insurance has more « generous » coverage. In the example above, the market can ultimately be characterized by two contracts: one that fully covers the risk of illness and has a premium of €50, or €0.50 per euro covered, and one with incomplete coverage that costs €0.10 per euro covered. The coverage of the second contract must be low enough to be unattractive to RE agents.

Moral hazard. In the example above, we assumed that an individual’s level of health care expenditure was determined purely exogenously: the individual had no control over it. In reality, if a person is insured, they will probably be more inclined to go to the doctor when they are sick. This is partly why a person will decide to buy insurance, and so it is actually a positive thing. On the other hand, being insured can also lead to « overuse » of insurance. For example, if my doctor prescribes three boxes of Doliprane when I know that I will only use one at most, I will have less incentive to tell the pharmacist that I only need one if I am insured than if I am not insured. This problem, known as moral hazard, and its extent are recurring themes in public debates, for example, with regard to unemployment insurance. In general, to combat this problem, insurance companies, or the state when it is the insurer, can limit certain uses of insurance by setting ceilings and/or deductibles. The bonus-malus system in auto insurance is , in principle, a means of combating both moral hazard and adverse selection: it allows for discrimination between good and bad drivers and encourages drivers to be more careful because their insurance premiums may increase in the event of an accident.

Empirically testing the importance of information asymmetries in insurance markets

Due to the dysfunctions they can cause, information asymmetries can justify public intervention and the public provision of insurance. But in order to determine whether such intervention is necessary, it is essential to know for which insurance markets information asymmetries are significant and cause major market malfunction, and for which markets these problems have a minor impact.

Since the early 2000s, significant progress has been made in this area. Initially, empirical studies developed econometric techniques to detect the presence or absence of adverse selection. This is the case, for example, with Chiappori and Salanié (2000), who studied car insurance for young drivers and found no evidence of information asymmetries. Their test is based on the fact that, in the presence of information asymmetries, the probability of having an accident should be correlated with the level of insurance coverage (see the example above), once the variables observed by the insurance company and used to determine the contracts to which a person is entitled and the premiums relating to them have been taken into account. This last point is important. Insurance companies use certain variables such as age or gender to determine the contracts to which a person is entitled. As a result, they classify the population into different risk categories. However, within these categories, there may still be heterogeneity of risk and information asymmetry. Chiappori and Salanié examine whether, among people who are offered the same contracts, those who purchase more insurance have, on average, more accidents, which corresponds to the case of information asymmetry analyzed above.

Empirical studies are now going further and seeking to quantify the welfare losses associated with information asymmetries. This is the case, for example, with Einav et al., who combine theoretical models and empirical data to study this issue in a specific insurance market. But perhaps the most glaring dysfunction in insurance markets is that some people simply cannot insure themselves against risk.

For example, in the United States (but also elsewhere), people with certain health problems simply cannot insure themselves against the risk of dependency because insurance companies refuse to cover them. Of course, they have a high (but far from 100%) risk of becoming dependent, but one might think that insurance companies could simply offer them contracts with higher-than-average premiums rather than simply refusing to insure them. Hendren (2013) shows that this phenomenon can be explained by the fact that the problem of information asymmetries is much greater among people in poor health than among those in good health. He also shows (Hendren, 2016) that information asymmetry issues alone can explain why there is no private unemployment insurance in the United States. These findings provide an important justification for the existence of public insurance systems against these risks. These systems play a redistributive role and also provide insurance to those who would not be able to obtain it within a private system.

Conclusion

Theoretical research, initiated in the 1970s, on the impact of information asymmetries on the functioning of insurance markets has shed light on some of the peculiarities of insurance contracts and markets. More recent empirical research now makes it possible to assess the importance of these information asymmetries in specific insurance markets and may be useful in informing the need for public intervention in the provision of certain types of insurance.

Bibliography

Akerlof George A., « The Market for ‘Lemons’: Quality Uncertainty and the Market Mechanism, » The Quarterly Journal of Economics, Vol. 84, No. 3., pp. 488-500, 1970

Chiappori P.-A. and Salanié Bernard, « Testing for Asymmetric Information in Insurance Markets, » Journal of Political Economy, 108 , 56-78, 2000

Einav Liran, Finkelstein Amy A., and Culler Mark R., « Estimating Welfare in Insurance Markets Using Variation in Prices, » Quarterly Journal of Economics, vol . 125 (3): 877-921, 2010

Einav Liran and Finkelstein Amy A., « Selection in Insurance Markets: Theory and Empirics in Pictures, » Journal of Economic Perspectives, Vol. 25 (1): 115-138, 2011

Hendren Nathaniel, « Private Information and Insurance Rejections, » Econometrica, 81 (5): 1713-1762, 2013

Hendren Nathaniel, « Knowledge of Future Job Loss and Implications for Unemployment Insurance, » forthcoming American Economic Review, 2016

Rothschild Michael and Stiglitz Joseph, « Equilibrium in Competitive Insurance Markets: An Essay on the Economics of Imperfect Information, » The Quarterly Journal of Economics, Vol. 90, No. 4, pp. 629-649, 1976

Wilson Charles, « A Model of Insurance Markets with Incomplete Information, » Journal of Economic Theory, 16, 167-207, 1977

[1] In his article, Akerlof used the example of a used car market to illustrate how information asymmetries can make a market inefficient and justify regulation or public intervention.

[2] This situation should be distinguished from the simple framework of imperfect but symmetric information, where the different parties involved in a transaction have incomplete but identical information.

[3] This example is inspired by the model developed by Rothschild and Stiglitz (1976). Einav et al. (2011) develop a graphical approach to understanding the effect of information asymmetries on insurance markets when firms only adjust the prices of insurance contracts (i.e., the premium), and not prices and quantities (the coverage rate).

[4] These assumptions are of course open to criticism because it is costly to provide insurance (it is necessary to hire administrative and financial staff) and because certain types of insurance are provided by a limited number of large insurance companies that have market power. However, these assumptions do not alter the logic of the negative effect of information asymmetries on insurance markets, and they are made here for the sake of simplicity.

[5] It can be shown, under standard assumptions, that both individuals should wish to cover themselves entirely against the risk of loss, given that the premium here is actuarially fair. Therefore, if insurance companies offer other actuarially fair contracts with lower coverage rates, these types of insurance should not be purchased.

[6] This assumption is not particularly restrictive in the medium term, as an insurance company can observe the reimbursements it must make to its policyholders.

[7] Two types of equilibrium can exist in this small model. A pooling equilibrium where a single contract with incomplete coverage is offered. Or a separation equilibrium where two contracts will be offered: one with full coverage and a premium of €50, and one with incomplete coverage and a lower premium that will be attractive to RF-type agents but not to RE-type agents. The definition of equilibrium by Rothschild and Stiglitz (1976) gives rise only to separation equilibrium. Wilson’s (1977) definition of equilibrium also allows for the existence of pooling equilibrium.