Summary:

· Economic growth in Europe is still recovering, but remains too slow due to persistent obstacles inherited from the crisis. The deterioration of the international environment requires Europe to strengthen its internal growth drivers in order to combat rising income inequality.

· The European Commission has slightly revised downwards its growth forecasts for Europe in 2016. However, growth remains stable, supported by domestic demand, and is contributing to a decline in unemployment, while investment is slow to pick up and inflation remains very low;

· International and European political and economic risks are casting a shadow of uncertainty over European growth, which nevertheless remains solid.

The Commission has revised downwards its growth forecasts for the EU for 2016 and 2017. Against a backdrop of a deteriorating international environment, European growth is relying more on domestic demand, while rising income inequality is tending to have a negative impact on consumption and investment. Nevertheless, growth remains robust and is contributing to the continued decline in unemployment in Europe. However, these forecasts are subject to increasing uncertainty, linked in particular to international geopolitical issues, but also to the various internal obstacles facing the EU.

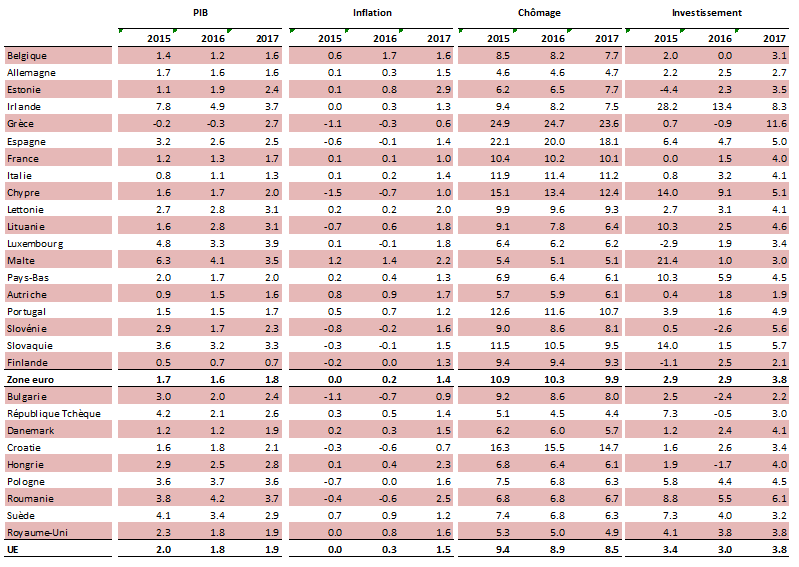

Table 1. European Commission macroeconomic forecasts

Source: DG ECFIN

A slow recovery in a deteriorating global environment

As the European economy enters its fourth year of recovery, it is clear that the pace of growth has remained very moderate for several years, particularly in comparison with the United States. Per capita GDP in the eurozone remains below its pre-crisis level, while the United States has caught up since 2014. Several reasons have been put forward to explain these differences:

- Cyclical reasons, notably more restrictive fiscal policies in Europe, which have had a negative impact on growth, and very high levels of debt in the banking sector, which are limiting the recovery in investment

- Structural reasons, such as less responsive labor markets, lower productivity growth, and more complex economic policy decision-making processes

The financial crisis in Europe has led to significant deleveraging needs on the part of households, banks, and governments, which has hampered the recovery of public and private investment, in a context where incomplete financial market integration makes European economic activity dependent on the health of its banking sector.

In addition, the moderate recovery in economic activity in Europe has been accompanied by growing income inequality. Increased international competition, technological innovation, rising unemployment, and labor market flexibility policies have had a negative impact on the incomes of the least skilled. This has resulted in a decline in the share of income of the poorest households in the total income of all households. In particular, in the euro area, the incomes of households living on less than 40% of the median wage have fallen sharply since 2008, while they have remained stable for the population as a whole. The share of income of the top quintile has also increased in recent years at the expense of the bottom quintile. Due to the lower marginal propensity to consume of the wealthiest households, the growth in inequality also has negative consequences for private consumption, the main driver of growth in Europe.

Sources: DG ECFIN, BSI Economics

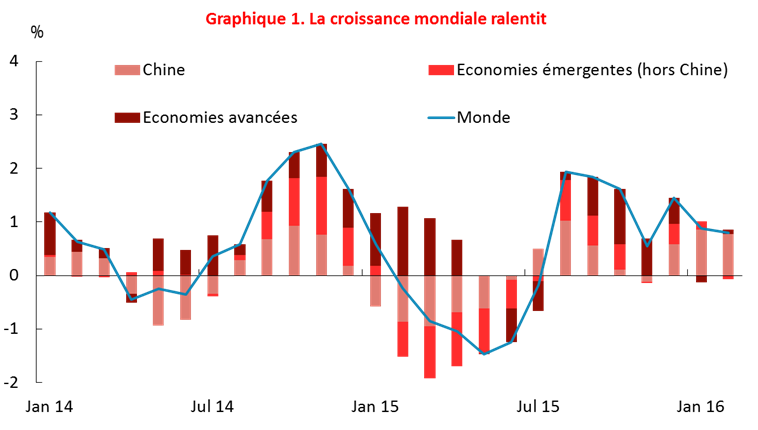

At the same time, the international economic situation has deteriorated since the end of 2015. With a rate of 3.2% in 2015, the global economy recorded its lowest growth rate since 2009. According to the European Commission, global growth is expected to rebound slightly to 3.3% this year before accelerating slightly in 2017 (3.7%). Low commodity prices continue to have a negative impact on exporting countries, while Russia and Brazil are expected to experience recession again in 2016. The slowdown in the Chinese economy is weighing negatively on international trade and European exports. Added to this are disappointing performances in advanced economies, where growth is not expected to exceed 2% in 2016 and 2017.

As the impact of positive factors such as falling commodity prices and the depreciation of the euro exchange rate tends to fade, this deterioration in the international environment accentuates the need for Europe to find internal drivers to support growth.

Modest growth and uncertainties

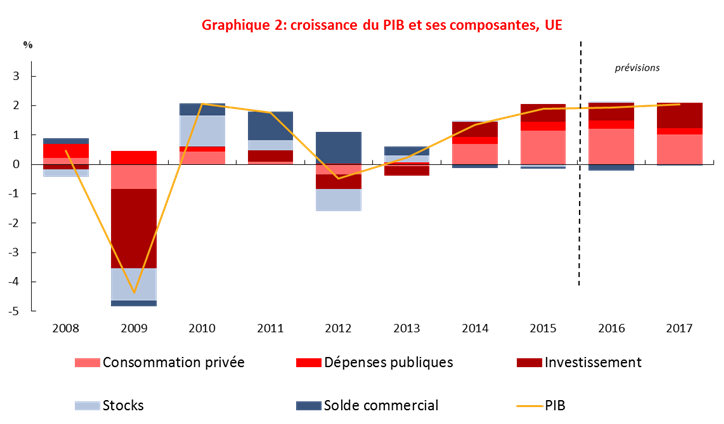

Sources: DG ECFIN, BSI Economics

Against this backdrop, the European Commission has revised its outlook for European growth in 2016 and 2017 slightly downwards compared with its February forecasts. GDP growth in the EU is expected to slow to 1.8% in 2016 from 2% in 2015, and to remain relatively stable at 1.9% in 2017.

In 2015, European growth was supported by domestic demand, particularly private consumption, which is expected to remain the main driver this year. The gradual decline in unemployment, combined with slight wage growth and low inflation, should continue to support consumption in 2016.

The conditions for a recovery in investment are in place. The ECB’s recent measures aim to support the recovery in investment by further reducing financing costs and facilitating access to credit. In addition, capacity utilization in the euro area is gradually returning to its 2011 level, while domestic demand continues to strengthen and offer better prospects for investors.

However, the combination of disappointing global growth, slowing international trade, persistently high private debt levels, and heightened uncertainty related to the international geopolitical environment is weighing negatively on investment, which is slow to recover. Overall, the European Commission forecasts investment growth of 3% in the EU in 2016, accelerating to 3.7% in 2017.

In 2016, economic growth, more favorable tax measures, and a moderate increase in wages should support net job creation and contribute to a decline in the unemployment rate in Europe. Performance varies greatly between Member States, but it is worth noting the strong performance of countries with the highest unemployment rates, particularly Spain, Portugal, and Ireland. However, unemployment remains very high in Greece and is slow to fall significantly in France and Italy. Overall, the European Commission estimates that the unemployment rate in the EU will fall from 9.4% in 2015 to 8.9% in 2016 and then to 8.5% in 2017.

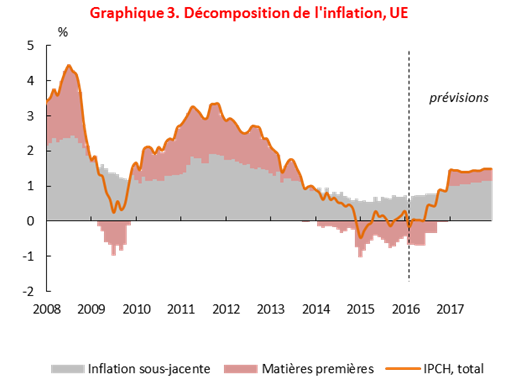

Sources: DG ECFIN, BSI Economics

The first figures for inflation in 2016 show a slightly downward trend. Weak commodity prices continue to weigh negatively on the HICP, while core inflation is not yet showing signs of acceleration due to moderate economic growth and low wage increases. Inflation is therefore expected to remain low this year, with the European Commission now forecasting 0.2% for 2016. The anticipated rebound in commodity prices and the gradual closing of the output gap in Europe are expected to exert inflationary pressure from 2017 onwards, reaching 1.4% according to the Commission.

Risks for 2016-2017

The downside risks that could undermine the forecasts appear to have increased, both internationally and within Europe itself. Among the external risks, the slowdown in the Chinese economy is casting enormous uncertainty over global growth. A further deterioration in Chinese growth could have contagion effects on emerging economies and Europe via international trade and financial markets.

The pace of US monetary policy normalization could also have a significant impact on capital flows. The Fed’s interest rate hikes could lead to significant capital flight from emerging countries and pose a sustainability risk for dollar-denominated debt.

The European financial sector continues to suffer from the legacy of the crisis. Low interest rates and persistently high non-performing loan ratios in some countries are eroding the profitability of the banking sector, while low inflation is making deleveraging more difficult.

At the European Union level, political risks are high and their potential impact on growth is highly uncertain. Uncertainty surrounding the UK referendum is weighing negatively on investment, but the consequences could be much greater for European growth if the UK leaves the EU. The large influx of asylum seekers since 2015 is creating uncertainty about the impact on the public finances of host countries, as well as on the absorption capacity of their labor markets.

Conclusion

Despite new measures announced in March, the ECB’s monetary policy is showing its limits, inflation remains low and growth is slow to pick up in Europe. The growth of inequality in favor of the wealthiest households is shifting the balance between savings and investment to the detriment of consumption and innovation, which is also weighing negatively on medium-term growth. Against a backdrop of very limited fiscal room for maneuver, these obstacles pose a risk of a significant slowdown in Europe’s long-term growth.

However, European growth remains robust. It is weathering the gradual disappearance of the positive impact of external factors that benefited it in 2015 (falling oil prices, depreciation of the euro) and is supported by dynamic private consumption. Unemployment continues to fall and the conditions are in place for investment to contribute more significantly to growth. Add to this a fiscal policy that is expected to become slightly expansionary in 2016, and Europe is strengthening the endogenous drivers of its growth.

Bibliography

– European Commission (DG ECFIN), European economic forecast – Spring 2016, May 2016, Institutional paper 25, Brussels

– European Commission (DG ECFIN), European economic forecast – Winter 2016, February 2016, Institutional paper 20, Brussels