Abstract:

· Eurobonds would be bonds issued at the European level at a single rate and would allow risk to be pooled among states, which would guarantee the debt service of other members.

· First proposed in the 2000s, the concept has seen a resurgence of interest during the sovereign debt crisis in an effort to stem the contagion of rate hikes;

· On a practical level, debate remains lively on a few key points: the seniority of these bonds, the nature of the guarantees, and the issuing entity;

· Two conditions appear necessary for the success of such an undertaking: increased economic and political cooperation at the European level and a rate lower than or equal to that applied in Germany.

Revived at the end of September by Mr. Villeroy de Galhau, Governor of the Banque de France, in an effort to decouple banking risk from sovereign risk, and more recently by the European Systemic Risk Board (ESRB)in order to facilitate the unwinding of the ECB’s quantitative easing program, Eurobonds are returning to the forefront. But what are they? What form would they take in practice?

While the stated objectives are laudable (reducing the risk of contagion, discouraging speculation, pooling risk, and improving financing conditions), there are obstacles to their implementation. What are they?

What are Eurobonds?

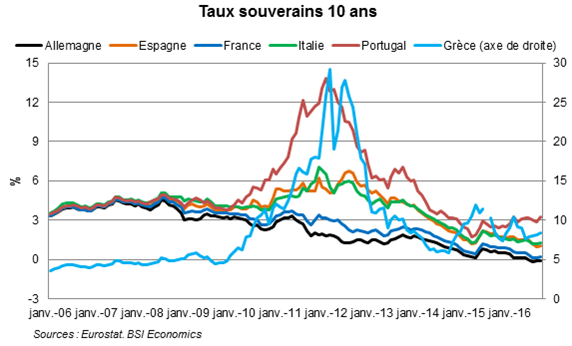

First mentioned in the Giovannini Groupreport in 2000, the topic of Eurobonds has been a recurring theme for many years. The idea was revived in the midst of the crisis in 2009 by the European Parliament’s Special Committee on the Financial, Economic and Social Crisis. The idea was to facilitate access to financial markets for countries in difficulty, while improving their financing conditions. Indeed, the financial distress of certain peripheral countries at that time led to a sharp rise in bond interest rates, with the risk premium demanded by investors increasing significantly, to the point of raising the specter of default, particularly in Greece. Eurobonds would therefore discourage speculation on the debt of the most troubled countries by pooling sovereign risks and, ultimately, significantly reducing the associated risk premium.

It was therefore with a view to stability and crisis prevention that the idea of mutualizing debt (and therefore risk) emerged. This principle of solidarity, which is intrinsic to Eurobonds, would then lead to a single rate, in stark contrast to the stylized facts currently observed on the bond markets. Indeed, although the creation of the Economic and Monetary Union (EMU) in 1992 gave rise to a relatively harmonized sovereign bond market thanks to the common currency, thereby narrowing yield spreads across the board, these spreads remain substantial. the situations of the countries are indeed different, particularly in terms of debt, wealth creation, and economic and fiscal policies. By way of illustration, we find Germany and Greece at opposite ends of the spectrum. However, since the creation of the Economic and Monetary Union (EMU), it has been generally accepted that rate differentials reflect the risk of sovereign default.

The introduction of a single rate, alongside the rates previously applied at the national level, would create a dichotomy within member countries: some would see their rates increase (e.g., the core eurozone countries) and others decrease (e.g., the peripheral countries), depending on their relative solvency within the zone. More specifically, rates could rise through the following two mechanisms:

· First, if the yield on national bonds is lower than that on Eurobonds, then the cost of borrowing via such instruments would increase;

· Second, the mutualization of debt could lead to an increase in liabilities for member countries, deteriorating their creditworthiness, which would ultimately also imply an increase in their financing costs.

Beyond the uniformity of rates, Eurobonds would reduce their default risk by acting on two levers. First, the risk of contagion to healthier countries could be reduced by limiting potential spillovers in the event of a deterioration in an issuer’s credit quality. Isolating a country in difficulty would thus guarantee the sustainability of the other members’ debt. Indeed, banking interdependence, cross-border assets, and trade links are all channels that can accelerate contagion. In addition, Eurobonds would limit the loss of confidence in the markets in the event of a shock, as the most creditworthy countries would provide guarantees for the mechanism.

Finally, functional Eurobonds would attract investors and enable competition with traditional US Treasury bonds, strengthening the euro’s role as a fully-fledged reserve currency. Furthermore, a liquidity effect could play a marginal role, as some small issuers are currently facing liquidity problems: Eurobonds could then have a beneficial effect on their borrowing costs by eliminating a large part of this liquidity premium.

From theory to practice

While the debate remains lively regarding the technical form of Eurobonds, the main points to be clarified include the type of guarantee provided by the eurozone, the seniority associated with the issue, and the issuing entity.

However,the choice of joint and several guarantees seems to dominate the debate. Thus, a single debt would be issued jointly by the member states, with joint and several guarantees: each issuer would then guarantee the entire debt. If one issuer were unable to service its debt [1](determined on the basis of the share of fundsgranted once the bond has been issued), then all the others would be liable. This type of guarantee appears to be a prerequisite for the success of a Eurobond project. Indeed, with guarantees specific to each country, the quality of a pan-European bond would only be the weighted sum of the countries’ commitments to this instrument. The establishment of a redistribution system to compensate states affected by an increase in the rates required by investors would be counterproductive because it would be anticipated by the market and would run counter to the very principle of issuing joint debt.

The second point of doubt concerns seniority: in the event of default, how should the new Eurobonds be ranked in relation to outstanding national bonds? If identical seniority is envisaged, the quality of Eurobonds would depend on the solvency of the member states guaranteeing the bonds, regardless of whether they themselves use the funds raised or not. If the risk premium on Eurobonds were higher than that of the most creditworthy country, the latter would bear the additional risk attributable to Eurobonds, which could lead to an increase in its default risk and, ultimately, its interest rate. Conversely, the least creditworthy countries would benefit from Eurobonds in the same way. Seniority greater than or equal to that of outstanding domestic securities is not feasible, as this would violate the contracts established with creditors for these funds.

The Bruegel think tank proposes an intelligent mix of these options: joint and several guarantees, junior and senior securities. More specifically, Delpha and von Weizsacker(2011) juxtapose blue bonds and red bonds. Blue bonds would consist of member countries’ debts, less than 60% of their respective GDP, and would benefit from joint and several guarantees. The authors argue that these instruments would be extremely liquid and on a par with, or even below, German rates. The non-mandatory nature of the choice of whether or not to participate in the issuance of new debt from one year to the next would be offset by the implementation of entry conditions relating to fiscal credibility. Red bonds, on the other hand, would consist of debt portions exceeding 60% and would be the sole responsibility of the issuing countries. Issued by national agencies and not guaranteed by European mechanisms, this portion would bear almost all of the default risk and attract investors seeking returns, which could also make it possible to keep this tranche out of the banking system.

Thus, if equal seniority is envisaged, the solvency of the countries participating in the issuance of Eurobonds would depend on the total volume of debt issued and their ability to repay that debt. The yield on Eurobonds could be lower than or equal to the weighted average (based on outstanding debt amounts) of countries’ rates, if the budget surpluses of the most creditworthy states were used to cover the debts of the least creditworthy. As for the issuing entity, the question remains open: should it be a private or public institution? The European Union seems unlikely, as all members would then be guarantors of debt issued in euros. The European Central Bank would seem more suitable, but its independence would then be called into question. A good compromise would therefore seem to be an independent European debt agency.

Eurobonds face strong political opposition from the most creditworthy countries, which would lose out by mutualizing risk and fear an increase in interest rates if Eurobonds fail to reduce the gap with Germany. The impact on borrowing costs will depend on two factors: the actual quality of the Eurobonds created, but also the change in the perceived quality of national bonds following the introduction of these pan-European bonds.

Eurobonds: a utopia?

The success of potential Eurobonds therefore lies in the harmonization of budgetary situations at the European level, as envisaged by the Maastricht Treaty and the golden rule, as well as greater political union: fiscal reforms and adjustments appear to be necessary. Nevertheless, the debate remains lively as to whether these reforms should be ex-post or ex-ante when European bonds are launched.

Furthermore, this plurality of issuing entities seems to be an obstacle to competing with US Treasury bonds, which are based on national debt, which is intrinsically more homogeneous than a European bond. As for the form these bonds would take, a simple version with only joint guarantees is unlikely to work, as it would simply produce a potential « band-aid » effect: the least creditworthy countries would continue to be dependent on debt and would have no incentive to improve their fiscal situation. Furthermore, the markets would no longer be able to « punish » budgetary slippage and would thus no longer be able to exercise their disciplinary power. While Bruegel’s proposal for Blue/Red bonds seems to fill this gap, the differentiation of seniority introduces a certain complexity into the creation of such bonds.

While these conditions are real obstacles, the introduction of Eurobonds would nevertheless send a strong signal in terms of credibility, signaling to the markets a genuine desire for European fiscal and political cooperation. Reducing the risk of contagion between countries in the event of a crisis and creating higher-quality debt that is potentially more resilient to market sentiment are compelling arguments at the European level. Finally, Eurobonds would be likely to attract investors, who would see them as an alternative to German securities in particular, which have become scarce on the secondary market, partly due to the ECB’s quantitative easing program.

Conclusion

The sovereign debt crisis in Europe has led politicians to consider the creation of Eurobonds guaranteed by member states in order to curb speculation and contagion within the eurozone. However, this idea is not new and dates back to the Maastricht Treaty (1992). Nevertheless, on a technical level, there are many uncertainties, particularly regarding seniority, the nature of the guarantees, and the issuing entity. Recent proposals on this subject clarify the framework and may point to imminent implementation. Nevertheless, a structural overhaul of economic and political cooperation within Europe, and more specifically within the eurozone, appears to be a prerequisite for the creation of these Eurobonds. Furthermore, in order to encourage the most creditworthy countries to take part in this project and to ensure that there is no moral hazard, the rate at which they would be remunerated would have to be lower than or equal to that of Germany, which would be made possible by the introduction of Blue/Red bonds.

[1] Debt service: repayment of principal (the amount borrowed) and interest.

[2] Seniority: order of repayment to security holders in the event of default. Senior instruments take priority over subordinated securities.