Abstract :

- The US dollar (USD) has appreciated significantly since the beginning of the year against emerging market currencies. Since the beginning of the year, currencies have lost more than 10% of their value, including the Argentine peso (more than 50%) and the Turkish lira (around 40%). However, the trend has reversed for the Mexican peso, which has been appreciating since the middle of the year.

- The weakening of emerging market currencies comes amid the normalization of US monetary policy, but can also be explained by political (Turkey, Russia) and economic (Argentina, Brazil) factors specific to each country.

- In response, most central banks in emerging countries have tightened their monetary policy.

- This depreciation of emerging market currencies against the USD could generate inflationary pressures and therefore weigh on household consumption, but would be favorable for the price competitiveness of these countries’ exports.

- Furthermore, the depreciation of emerging market currencies automatically leads to an increase in the value of their outstanding USD-denominated debt.

- Against a backdrop of rising interest rates in the United States, trade tensions, rising oil prices, and geopolitical risks, the US dollar is likely to continue to appreciate against emerging market currencies.

International economic and monetary news in recent months has been marked by downward pressure on emerging market currencies—and more specifically on the Turkish lira and the Argentine peso—against a backdrop of renewed protectionist measures and the normalization of US monetary policy. This article seeks to analyze the underlying factors behind this trend and distinguishes between those related to the global monetary context and those that are more specifically domestic in nature.

.jpg)

Are we heading towards a crisis in emerging countries similar to that of 1997-98? The weakening of emerging currencies since the beginning of the year and the increase in the number of countries in serious financial difficulty suggest the worst, according to some analysts. However, the current situation must be put into perspective.

Firstly, apart from Argentina and Turkey, the movements observed in exchange rates are relatively minor. Risk aversion is also not widespread across all emerging countries, as some of them, such as Mexico, have so far been spared downward pressure on their currencies. Investors remain particularly attentive to the risks specific to each country, and it is mainly those countries considered to be the most fragile that are affected by the markets. Furthermore, the current situation is very different from that of 1997-98, when the crisis followed a period of overinvestment. Emerging countries also have greater foreign exchange reserves to cushion external shocks.

However, vigilance remains essential as these countries face an increasingly unfavorable international environment, with the resurgence of protectionist measures and the rise of the USD, largely supported by the Fed’s rate hikes. Beyond the risk of accelerated repatriation of capital to USD assets, investors fear that these countries will be unable to meet their financial commitments. Indeed, the depreciation of the currencies of certain emerging countries automatically leads to an increase in the value of their outstanding debt, which is often largely denominated in USD, further heightening market nervousness about emerging currencies. In other words, this currency crisis could turn into a debt crisis for some emerging countries. Argentina, Ukraine, Turkey, and Brazil are often cited as the most vulnerable countries in this regard.

1. Argentina: the peso falls despite Central Bank interventions

The Argentine peso has fallen by more than 50% against the USD since the beginning of the year, despite multiple interventions by the Central Bank on the foreign exchange market and interest rate hikes. The country requested support from the IMF, with which a three-year loan agreement was approved last June for USD 50 billion.

The Argentine peso has been depreciating against the USD since the beginning of the year due to a confluence of factors. A severe drought has led to a sharp decline in agricultural production (especially soybeans) and export revenues, global energy prices have risen, and financial conditions have tightened due to a rise in US interest rates. The IMF expects inflation of 22.7% for 2018. The Argentine Central Bank made a surprise move on August 30 to raise its key interest rate from 45% to 60% in an attempt to limit the peso’s depreciation, but this decision had the opposite effect to that intended, with the Argentine currency falling 20% against the USD in 48 hours. Markets were also unsettled by Argentine President Mauricio Macri’s request for an advance payment of IMF aid. Some investors doubt that the USD 50 billion program granted by the fund will be enough to pull the country out of its financial impasse.

Graph 1 Argentine peso (ARS) / US dollar (USD)

2. Turkey: Turkish lira falls due to a combination of factors

In Turkey, the lira has lost more than 40% of its value against the USD since the beginning of the year. The Turkish currency has been affected by fears associated with, among other things:

- rapid credit growth and inflation (16% year-on-year in July);

- a high current account deficit;

- monetary policy under pressure from the executive branch; and

- diplomatic tensions with Washington.

The downgrade of the sovereign rating by S&P in April, following Moody’s downgrade in March, also weighed on the Turkish currency. Finally, the lira has been particularly weak for many months due to the unorthodox monetary policy desired by President Erdogan, who advocates lower interest rates to support growth. The appointment of his son-in-law as finance minister in early July accelerated the lira’s decline. In response to the currency’s collapse, the Central Bank reacted vigorously with a 500 basis point hike since April, bringing the key rate to 17.75% in June, but the markets considered this reaction too late and the decision failed to halt the decline. Rates are reaching historic levels on the bond market, at over 20% for 10-year bonds.

Graph 2 Turkish lira (TRY) / US dollar (USD)

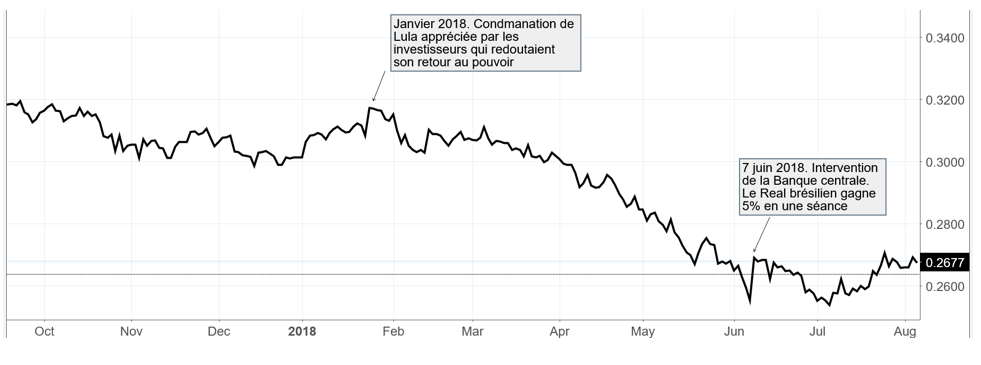

3. Brazil: Brazilian real falls sharply in pre-election context

Brazil has not been spared by investor withdrawals, with investors remaining concerned about the country’s fiscal situation and awaiting the presidential elections in October. The real has depreciated by more than 20% against the USD since the beginning of the year, leading the Central Bank to intervene more intensively in the foreign exchange market last June. The depreciation of the Brazilian real has led to a decline in the price of sugar, which is priced in dollars, with Brazil alone accounting for 45% of global exports. Brazil still has a solid external position with foreign exchange reserves estimated at USD 363 billion, covering 22 months of imports (BNP Paribas Research).

Graph 3 Brazilian real (BRL) / US dollar (USD)

4. South Africa: Rand falls again against the dollar

The appointment of C. Ramaphosa to succeed J. Zuma as head of state in February 2018 more than reassured the markets about the trajectory of public finances, allowing the rand to approach its best level against the dollar since mid-2015 in February 2018. However, the South African currency, which is highly prized by investors for carry trade strategies, has fallen again against the dollar since the publication in June 2018 of data showing a contraction of around 2.2% in South African GDP in the first quarter. The currency also fell again in early September when it was announced that the country had entered recession inthe second quarter for the first time since 2009. President C. Ramaphosa’s plan to expropriate agricultural land without compensation is causing concern among investors.

Graph 4 South AfricanRand(ZAR) / US Dollar (USD)

5. Russia: the ruble falls despite rising oil prices

Despite rising oil prices – the ruble is traditionally correlated with crude oil prices – the Russian currency continues to depreciate following the strengthening of US sanctions voted by Congress on April 6 and the news announcements in early August. The Russian currency is flirting with its lowest levels against the dollar, reached during the previous crises in December 2014 and January 2016.

After a year of successive cuts to its key interest rate until last March, the Central Bank has since kept it at 7.25% and has suggested that it intends to extend this pause, as inflationary risks have increased.

Graph 5 Russian ruble (RUB) / US dollar (USD)

6. China: Renminbi depreciation curbed by the Central Bank

The Chinese authorities allowed the renminbi to lose 10% of its value against the US dollar between early April and mid-August. The depreciation of the renminbi (RMB) has intensified since June 15, when the United States confirmed the increase in customs duties. The US President responded by accusing China of manipulating its currency to regain competitiveness in its exports and offset the effects of the US tariff increases. State-owned banks intervened in the foreign exchange market to limit the depreciation of the RMB. For its part, the Central Bank is maintaining its « 7-3 stability threshold » target: the currency must not rise above 7 yuan to the dollar, and foreign exchange reserves must remain above the $3 trillion threshold. According to many analysts, the decline of the renminbi should remain under control so as not to fuel capital outflows as in 2016.

Graph 6 Chinese renminbi (CNY) / US dollar (USD)

7. Mexico: reversal of the trend for the Mexican peso

While the Mexican peso was following a similar trend to other emerging currencies, which were severely weakened by the monetary situation in the United States and trade tensions over the revision of NAFTA agreements, the trend completely reversed following the victory of Andrés Manuel López Obrador. The left-wing candidate, who won the presidential election by a large margin, was quick to reassure the markets about the country’s economic policy during his term in office. Since the election results in early July, the peso has appreciated by more than 10% against the USD. The sharp rise in the peso has also been supported by the interventionism of the Mexican Central Bank, which has raised its key interest rate several times. The Mexican peso has recently benefited from the newly signed agreement with the United Stateson NAFTA.

Graph 7 Mexican peso (MXN) / US dollar (USD)