ECB monetary policy and exchange rates

Summary:

· A weak euro has several advantages for the eurozone: it improves the price competitiveness of exports, increases the margins of exporting companies, and generates imported inflation.

· By contributing to the creation of a low interest rate environment through its negative interest rate policy and quantitative easing, the ECB is pursuing the objective of maintaining downward pressure on the exchange rate.

· Announcements by the major central banks also play a significant role in the level of the euro, particularly by influencing financial market expectations.

For severalyears now, the European Central Bank (ECB) has played a central and decisive role in the eurozone. Although it always acts within the scope of its mandate, which is to ensure price stability in the eurozone, the ECB continues to redouble its inventiveness and efforts to bring the eurozone out of its current economic stagnation once and for all.

The conventional tools at its disposal (interest rates) and the unconventional tools it has launched are currently raising questions among the general public and even, in some cases, among financial professionals. In this article, we aim to explain the main mechanisms and ideas behind these tools, to understand how they complement and/or interact with each other in order to respond to the economic challenges facing the euro.

Why would anyone want a weak euro?

In a previous article on BSI Economics, we presented the reasons for having a weak euro. A continuous and sustained depreciation of the euro would improve the price competitiveness of exports outside the euro zone (55% of exports on average in France according to INSEE) and enable exporting companies to gain market share internationally and see their margins increase. However, a weak euro tends to increase the cost of imports, but in the current context where commodity prices, especially oil, remain low, a positive exchange rate effect for companies could be expected in the event of a depreciation of the euro. Furthermore, a depreciation of the euro, by increasing the cost of imports, would stimulate inflation (which returned to negative territory in February 2016 at -0.2%) via imported inflation.

What is the impact of unconventional monetary policies?

The main channel for monetary policy in the eurozone is currently the exchange rate. An expansionary monetary policy has a direct impact on the value of the currency. By injecting liquidity, the ECB is therefore maintaining downward pressure on the euro through a relatively simple mechanism: the stock of liquidity (denominated in euros) in circulation increases and its value therefore tends to fall. This basic mechanism is at the heart of both conventional and unconventional monetary policies.

Quantitative easing (QE ), one of the tools launched by the ECB in March 2015, does not have the direct objective of lowering the value of the euro, but the massive asset purchases (€80 billion of monthly financial asset purchases) on the secondary market constitute a large-scale injection of liquidity, which ultimately leads to a depreciation of the euro. More indirectly, by promoting lower sovereign bond yields in the eurozone over increasingly longer maturities, QE helps to maintain downward pressure on the exchange rate by promoting the emergence of a low interest rate environment.

With a low refinancing rate (0% since March 2016), eurozone banks can refinance themselves at low cost in the short term with the ECB during its weekly open market operations. A low refinancing rate thus facilitates access to central liquidity for banks in need of liquidity and increases (at least in theory) the amount of euros in circulation, putting downward pressure on the euro exchange rate. However, the refinancing rate has only a very marginal effect[2] in the current context of excess liquidity.

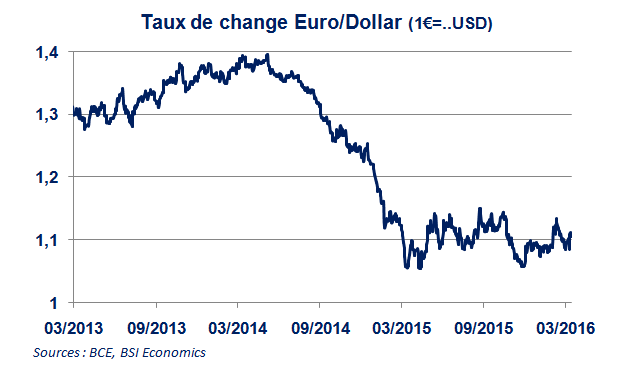

A negative deposit rate has a decisive impact on the exchange rate. Currently, the deposit rate is -0.40%, following the ECB’s last meeting on March 10, 2016. A low refinancing rate combined with an equally low or even negative deposit rate favors the creation of a low » interest rate environment. » These two interest rates serve as benchmarks, so when they are extremely low, they maintain downward pressure on all interest rates within the eurozone. Thus, a low « interest rate environment » makes the eurozone less attractive to foreign capital. International capital flows are often guided by the search for high returns and therefore by high interest rates. Countries experiencing significant capital inflows automatically see their exchange rates appreciate. But in the opposite case, low interest rates (especially when they are below or equal to 0) seem less attractive and therefore attract less international capital, so the exchange rate does not appreciate. In a context where the United States and the United Kingdom are entering a phase of monetary policy normalization with a (very) gradual rise in interest rates, the capital outflows that have been occurring for several years in emerging countries could be redirected towards these economies rather than the eurozone. This divergence in monetary policy choices could lead to a depreciation of the euro against the dollar.

How do ECB announcements affect the euro?

Communication remains one of the key tools used by central banks to assert their credibility and guide financial markets on the conduct of monetary policy. Depending on the vocabulary used by the ECB (where every word is carefully weighed) and the economic situation in the eurozone (even if this does not fall directly within the ECB’s mandate), financial markets anticipate the ECB’s next announcements and actions. These expectations « trigger » strategic decisions made even before the announcements (hence the expression » the market has already priced it in « ) and after the announcements. These decisions have a decisive impact on the level of the euro: directly through the flows generated by financial transactions (across the entire range of financial assets: bonds, equities, currencies, interest rate swaps, etc.) and somewhat less directly through the confidence inspired by the ECB’s actions.

This reasoning is valid in absolute terms and is equally valid in view of the ECB’s announcements and actions relative to those of other major central banks (the Fed or the BoJ, for example). For example, uncertainties surrounding economic growth in the United States prompted the Fed to postpone raising the fed funds rate several times in 2015, contributing to the stability of the euro-dollar exchange rate, whereas parity (one dollar to one euro) had been expected by the end of 2015 and is still hovering around 1.10 at present. To move towards euro-dollar parity, the schedule of US rate hikes for 2016 will therefore be as important to watch as the ECB’s announcements.

Conclusion

A combination of different monetary policy tools is needed in order to pull all possible levers and move towards euro-dollar parity. The mechanisms described above are the basis for fluctuations in the value of the euro. According to the MacroNetwork Consensus, 56% of economists surveyed believe that euro-dollar parity will be reached in 2016. The symmetrical behavior of the major central banks will play a decisive role in determining the level of the euro, and the ECB will also have to be particularly attentive to the « moods » of the financial markets in order to reconcile its mandate with its objectives.

[1] For the sake of simplicity, we will not address the need for export specialization in goods with high price elasticity of demand in order to benefit from a positive exchange rate effect in the event of a depreciation of the euro.

[2] The recent cut in the refinancing rate is more of a signal effect, and its usefulness is to be found more in the launch of new TLTROs (four-year long-term loans granted by the ECB to banks).

[3] However, it should be noted here that the stability of the exchange rate in the short term or its appreciation in certain cases is favored by investors (so as not to suffer a negative exchange rate effect on their transactions), which is why when the ECB’s announcements do not live up to their expectations (or their own interests), they tend to « sell » the euro, thereby driving down its price.