Abstract:

- In France, savings are « superabundant » but not particularly geared towards financing companies’ equity capital.

- Two factors may explain the underinvestment in equities: on the part of savers, a lack of financial education and caution; on the part of institutional investors, such as insurers, restrictive prudential regulations (Solvency II).

- The Pacte law aims to encourage long-term savings—but care must be taken not to steer French people toward overly risky investments and expose them to economic downturns.

This article outlines the basis for the Pacte law, which will soon be discussed by the Council of Ministers: French financial savings do not provide sufficient financing for businesses. To address this shortfall, there are two possible solutions: increase French people’s savings in equities, or encourage institutional investors to invest in equities.

According to a report by France Stratégie[1], only 11% of French financial savings are allocated to financing corporate equity. While this figure is significantly underestimated, particularly due to the difficulty in ensuring transparency among collective investment undertakings (CIUs) that hold securities (for example, in the insurance sector alone, equity investments are estimated to account for 18.7% of the sector’s investments in mid-2017), it nevertheless illustrates the insufficient allocation of French financial savings to domestic companies.

Yet French people have abundant, even excessive, savings, representing 14% of gross disposable income in 2016 (compared with 17% in Germany, 6.1% in the United Kingdom, and 10.1% in the European Union); financial savings represent 6% of gross disposable income, which is above the eurozone average (5%).

As part of the Pacte law (Action Plan for Business Growth and Transformation) presented to the Council of Ministers on May 22, several proposals will be evaluated with a view to improving business financing. Are the proposed solutions appropriate for France?

1. Is equity financing (really) insufficient in France?

First, we need to look at the financing structure of non-financial companies. The main sources of corporate financing are capitalization, bond market debt financing, and intermediated bank financing.

In 2017, corporate capitalization accounted for 62% of financing sources in France, compared with 54% in the eurozone and 57% in the United States (see Chart 1). However, access to the market via bond issues is much more developed in the United States. Since 2007, capitalization has increased by €1.4 trillion in France, compared with €4 trillion in the euro area and $10 trillion in the United States.

In terms of equity structure, French companies are relatively well endowed compared with the rest of the eurozone and the United States. At the end of 2015, equity holdings were divided between 29% listed shares, 53% unlisted shares and 18% other holdings.

Chart 1 – Financing structure of non-financial corporations, in value terms

Sources: ECB, BSI Economics

However, summarizing the allocation of savings to equity capital by the percentage of shares is simplistic. For example, holding listed shares (as illustrated above) does not necessarily mean financing domestic companies. The stock of shares represents the capitalization of the company and is worth 100% at its creation; the financing of a company is therefore measured more by the net issuance of securities, and in particular the net issuance of shares, debt securities, and bank loans. In 2017, net share issuance in the euro area amounted to only €28 billion, or 25% of net securities issuance. Net debt securities issuance amounted to €87 billion.

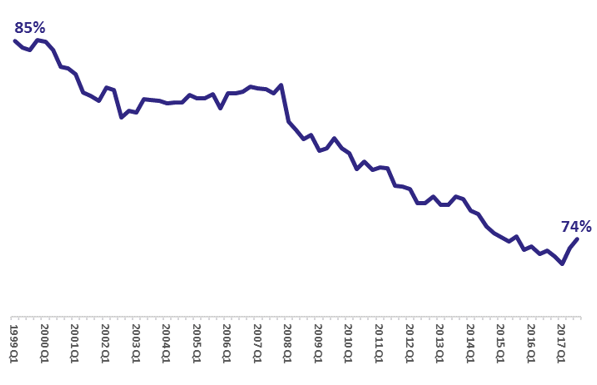

Chart 2 – European share ownership by euro area residents

Sources: ECB, BSI Economics

Furthermore, the share of eurozone shares held by residents has been falling steadily since the 2000s, reaching 74% in 2017 (see Figure 2). Foreign investors are by far the largest group of shareholders in listed companies in France; the increase in their relative weight is the most striking change in the capital structure of French listed companies in recent decades. However, this European (or national) equity capital is necessary to support growth. To return to 2000 levels, eurozone residents would need to increase their shareholdings by €4.5 trillion (excluding new issues): this could be achieved either by increasing investment in shares by individuals or by encouraging institutional investors to invest in shares.

2. Increasing productive investment by promoting savings in equities: a dead end in France?

France stands out from its European neighbors in that direct holdings[2] of listed and unlisted shares are below average (nearly 20% of assets). However, resident individuals remain the largest group of shareholders after non-residents, holding nearly one-third of French listed shares (held directly or indirectly). However, incentives for direct share ownership seem to have little effect on French savers.

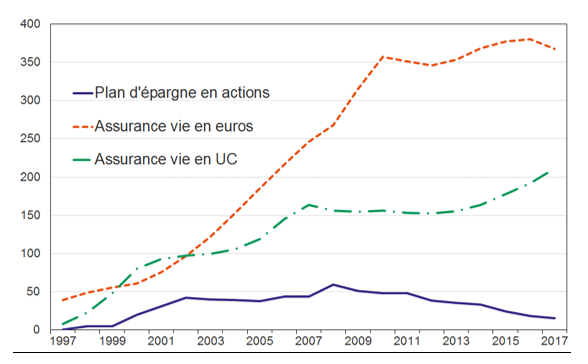

Indeed, observation of French savings behavior over the past 30 years illustrates their low appetite for risky investments. Let’s compare the evolution of three types of investments that benefit from tax advantages: PEA (share savings plans), unit-linked products, and euro-denominated life insurance funds. PEAs are mainly invested in one asset class, equities, and reflect stock market performance each year. Unit-linked products also reflect market performance each year, but offer greater diversification across asset classes, as do euro funds, which offer capital protection at all times but are still 10% invested in equities by insurers.

Graph 3 – Cumulative flows of PEA and life insurance

Notes: Net inflows into PEA savings plans are reconstructed using the SBF 250 index as a valuation indicator.

Sources: Banque de France, FFA, BSI Economics.

The consequences in terms of attractiveness for savers are immediately apparent (see Chart 3): investments are all the more attractive when savers are assured of the stability of their assets. Thus, the PEA, created in 1992, showed positive inflows until 2002, virtually zero inflows until 2008, and then negative inflows over the last eight years. Cumulatively over the last twenty years, net inflows into the PEA are virtually zero. UC-based vehicles have experienced much more continuous and even growing growth in recent years, recording cumulative net inflows of just over €200 billion. Finally, euro-based vehicles far exceed the two previous inflows, at nearly €370 billion.

Furthermore, the argument that « on average, equities offer a better return, so invest in equities » has no real basis: average equity returns only make sense in the long term, and the volatility of returns discourages cautious savers from exposing their savings. L. Arrondel and Masson (2017)[3] empirically demonstrate this behavior and explain the decline in risky asset holdings during the crisis by lower expected returns and shocks to current resources.

3. Increase productive investment by encouraging institutional investors to invest in equities

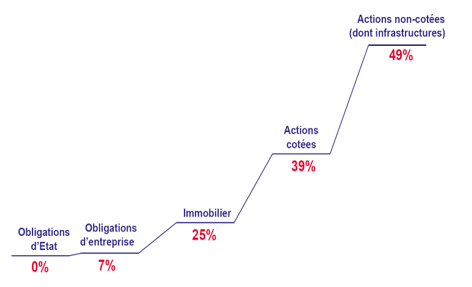

Another channel for increasing equity financing for companies is to increase investment in equities by institutional investors, namely banks, insurance companies, and investment funds. Bank investment in equities has been in steady decline since the 1980s; while insurance companies’ investment in unlisted companies is growing, it is constrained in particular by Solvency II (see Chart 4).

Chart 4 – Capital requirements for investments under Solvency II

Notes: as a percentage of the market value of the security

Sources: EIOPA, FFA, BSI Economics

One solution is to encourage agents to save for the long term, which would increase equity investments by the institutions in charge. In the case of very long-term savings, the additional duration allows for greater investment in the productive economy (see, for example, Bardaji and Frezal[4]). Lyonnet (2018)[5]shows that, when representing longer liabilities, insurers do indeed have the capacity to invest in riskier assets that contribute more to the financing of the productive economy. Given that the tax burden on returns on investment decreases with the age of the contract (in the case of life insurance contracts), investors with relatively longer contracts should favor redeeming their contracts later than investors with younger contracts. Consequently, coupled contracts should have little exposure to surrender risk. This theoretical result is confirmed by the author: a one-standard deviation increase in surrender risk:

- decreases the maturity of insurers’ bond purchases (sovereign and corporate) by 1.2 years on average;

- increases the share of their equity acquisitions by 25 basis points.

The Pacte law aims to increase retirement savings, which represent more than €200 billion in assets, most of which are currently invested in assets that are not well suited to long-term investment (sovereign debt and large corporate debt). The widespread adoption of managed accounts for these savings will enable them to be directed towards the productive economy, offering better returns for future retirees.

However, increasing investment in equities by liberalizing high-equity, non-guaranteed products could pose a real risk to savers: the widespread use of non-guaranteed retirement savings vehicles would transfer significant financial risks to policyholders due to the absence of a financial guarantee on the capital. During the 2008 financial crisis, pension funds as a whole lost nearly 23% of the real value of their investments, equivalent to USD 5.4 trillion, which represents 21% of the OECD’s GDP[6]. Countries with high rates of funded pensions and massive exposure to non-guaranteed pension schemes with a strong focus on equities suffered losses as a result: in the United States, 45% of 55-65 year olds hold more than 70% of their retirement savings in equities, compared with 50% of those under 55; In Australia, more than 60% of savers stick to the default investments for their retirement savings, in which equities account for more than 60%.

Conclusion

France suffers from abundant savings that are poorly directed towards the productive economy. The Pacte law aims to address this shortcoming and massively encourage long-term savings and direct share ownership. However, it is necessary to take into account the preferences of the French, their behavioral biases, and to favor the institutional route of productive investment. It should be remembered that one of the axioms of public policy theory is that a single instrument should not be used to achieve multiple objectives (for example, Tinbergen’s rule states that for any economic policy with set objectives, the number of instruments must be equal to the number of objectives). The danger is that a single instrument may achieve contradictory objectives. Retirement savings should therefore not be used for other purposes (e.g., financing the productive economy, purchasing a home, etc.), as the economic mechanisms at work could be counterproductive.

[1]Taxation of financial savings and investment orientation, April 2017

[2] Households can hold shares directly, for example in a share savings plan (PEA), or indirectly, i.e. via composite investment instruments (UCITS securities, life insurance) managed by institutional investors.

[3]Luc Arrondel and André Masson, » Why is demand for shares falling during the crisis? The case of France, » 2017.

[4] » What is the optimal contractual model for funded pensions? « , Revue Risques No. 111, Sept. 2017.

[5]V. Lyonnet (forthcoming), « Asset-liability management in life insurance: Evidence from France, » WP to be presented at the11th Financial Risks International Forum on « Emerging Extra-Financial Risks in Finance and Insurance, » March 26 & 27, 2018.

[6]E. Whitehouse (2009), “Pensions during the crisis: impact on retirement-income systems and policy responses,” OECD, Geneva Papers on Risk and Insurance – Issues and Practice 34(4):536-547

[7]Figures from theEmployee Benefit Research Institute, 2008