Summary:

· In theory, deregulation unlocks growth potential by lowering costs and enabling better risk management, whereas regulation allows risks to be internalized.

· Few gains are to be expected from easier financing, while the risks are high.

· The current environment is not conducive to deregulation due to a high financial cycle, potentially exacerbated inequalities, and a structural lack of demand.

· There is a risk of contagion linked to deregulation, and the question that should be asked at present is rather how to regulate better.

Donald Trump’s promiseto repeal the Dodd Frank Act[1], the UK’s concern for the City’s competitiveness after the Brexit referendum result, but also the opposition of many European governments to a change in risk weighting rules, and the return to favor of securitization with the European capital markets project[2], have brought the issue of financial regulation back to the forefront.

Financial groups have often opposed new regulations, but for the first time in almost 20 years, governments themselves are beginning to take up the deregulation argument. The reforms implemented after the crisis are being called into question and new deregulation is regularly discussed.

The potential gains from deregulation are well identified. Deregulation would allow for better allocation of resources by removing barriers that hinder arbitrage opportunities and, thanks to greater diversification, reduce risks. By creating competition among agents and opening up access to new markets, deregulation can also help lower financing costs , thereby enabling greater financial efficiency and unlocking growth potential.

The wave of deregulation in the 1980s and 1990s, with, for example, the removal of barriers to banking activities between states in the United States or, to a lesser extent, in Europe with the single banking license, has enabled agents to diversify their positions and thus reduce their risks. Concentration and modernization through the computerization of stock exchanges has led to economies of scale and, in particular, easier borrowing for governments. Are there still potential gains that financial deregulation could unlock today?

1. Deregulate for better risk management?

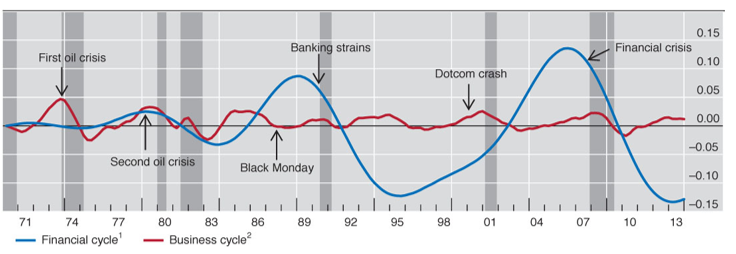

Deregulation does not always correlate with lower risks, as demonstrated by the increase in financial instability that followed the wave of deregulation in the 1980s and 1990s, through the amplification of the financial cycle and its increasingly pronounced disconnect from the real economy.

Chart 1: Financial and real economic cycles in the United States

Source: BIS

In addition, the individual risk-taking of each bank or financial entity also poses a systemic risk to the sector itself, but also to the rest of the economy. Thus, while a bank covers its potential losses when it takes a position, it does not cover the associated systemic risk that results from the aggregation of the behavior of all actors in the system. For example, buying an asset during a bubble feeds the bubble and increases the risk of it bursting. Regulation therefore corrects this blind spot by requiring financial players to hold more capital than they would without taking this systemic risk into account (Korinek and Kreamer, 2014). The recent Basel III regulations, for example, include an additional capital buffer for very large banks, known as « systemic » banks, because their failure poses a risk to the entire system. This is a risk that they do not take into account in their individual risk-taking.

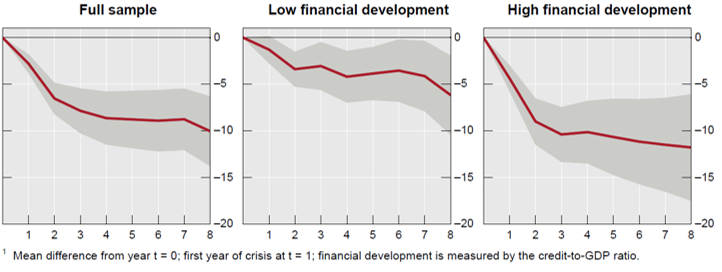

This additional capital comes at a cost to banks and the economy, but in return, the probability of a crisis is reduced. Crises involving the banking sector are the most « destructive » and, in addition to causing a deep recession, they permanently reduce growth potential (Figure 2).

Figure 2: GDP growth after a financial crisis according to the degree of development of the financial sector (as a percentage of the pre-crisis trend)

Source: IMF

Studies therefore show that the cost of additional capital is more than offset by the reduction in financial crises (BIS, 2010). Nevertheless, these estimates are complex and based on numerous assumptions.

2. Deregulate to facilitate financing?

Facilitating financing through deregulation can come either from lower costs or from easier access to financial markets through a reduction in non-price constraints.

Due to the low interest rate policy and liquidity injections implemented by the major central banks over the past several years, financing costs in developed countries are currently very low. This is evidenced by surveys on credit conditions conducted periodically in the euro area (ECB, 2016). Thus, further lowering financing costs is likely to benefit riskier activities, as suggested by the work of Minsky (1986), which shows that the further we advance in the credit cycle, the more profitable investments have already been financed. Investors are therefore gradually turning to riskier investments with uncertain outcomes, weakening the entire system. With the credit cycle at its peak, stronger regulation is needed to curb excessive risk-taking, such as the countercyclical buffers provided for in Basel III.

New forms of financing have developed in recent years, such as crowd funding (see: » The hypergrowth of crowdfunding , » BSI Economics), or the return of securitization (see: » Capital Markets Union: profitable but not without risk , » BSI Economics). The latter make it possible to bypass the banking sector, whose constraints (non-price, such as income requirements) have tightened since the crisis (ECB, 2016). They also facilitate access to capital markets for increasingly smaller companies and customers considered too risky by banks. With the exception of securitization, these new forms of financing are currently very lightly regulated, leaving little room for potential deregulation. On the contrary, these new financing methods need to be regulated, at least to protect consumers from possible abuse, as suggested by the regular warnings issued by the French Financial Markets Authority (AMF) and the Bank of France.

3. The current environment is not conducive to a new wave of deregulation

A high financial cycle, potentially exacerbated inequalities, and a structural lack of demand create a current environment that is not conducive to a new wave of deregulation.

Mainly due to the low interest rate policy and massive liquidity injections implemented by the major central banks over the past several years to counter the effects of the 2007 crisis, financial institutions have found themselves with large amounts of liquidity to invest and have embarked on a race for yield, leading them to invest in riskier assets such as equities. At the same time, liquidity injections (quantitative easing) have created a shortage of certain financial assets, such as sovereign bonds in Europe, forcing investors to turn to riskier assets.

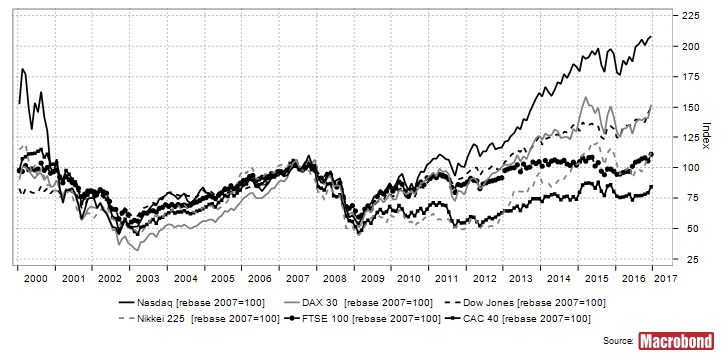

As a result, the major financial markets are now at high levels (Chart 3). The Dow Jones, Nasdaq, DAX 30, and FTSE are at historic highs. Only the CAC 40 and Nikkei have not yet reached this level. Deregulating today by repealing the Volcker Rule in the United States, which limits banks’ ability to speculate on their own account (see » In a nutshell, what is the Volcker Rule?« , BSI Economics), therefore risks fueling a potential bubble and precipitating a new financial crisis for which central banks will have very little room for maneuver.

Chart 3: Main stock market indices, 2000-2017

Sources: Macrobond, BSI Economics

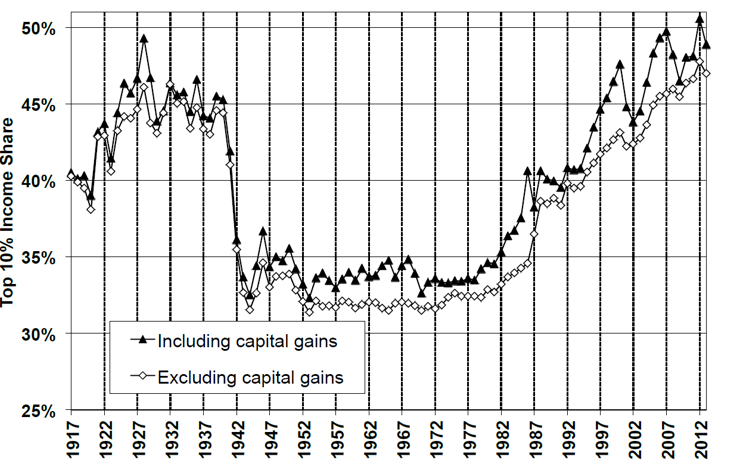

Deregulation today risks amplifying one of the major challenges of this decade: inequality. Korinek and Kreamer (2014) show that deregulation favors the banking system in the distribution of wealth, thanks to greater risk-taking and therefore higher returns, coupled with losses that are mutualized through public intervention. Deregulation therefore risks benefiting above all the wealthiest, whose incomes have for the most part already returned to their pre-crisis levels, while those of the poorest remain stagnant (Figure 4).

Figure 4: Share of total income earned by the top 10%

Source: Saez, 2013

Inequality may even be fertile ground for the outbreak of a financial crisis, as suggested by Moss’s (2010) work on the United States and the correlation he highlights between the level of inequality and bank failures.

Today, many institutions attribute the low growth in most developed countries not to a supply problem, through restricted access to credit or its prohibitive cost, but rather to insufficient demand. The IMF and the OECD, as well as the OFCE, have repeatedly called for stimulus plans based on their recent work on public infrastructure investment (IMF, 2014). Seeking to facilitate financing today is therefore likely to have little effect due to a lack of demand.

Conclusion

Deregulation today would above all risk amplifying the risks of future financial crises without necessarily bringing substantial gains in terms of growth potential. Today, the issue is not so much one of deregulation, but rather of better regulation, as many new regulations have been put in place since the crisis. The issue of deregulation may reflect a need for greater visibility of the priorities on the regulatory agenda and simplification of the multi-layered regulatory framework.

Furthermore, any deregulation today is likely to be contagious, as many countries want to defend their banking systems and do not want them to be disadvantaged in the face of international competition. Deregulation today would therefore pose a major risk to financial stability, which is fragile overall, in a context where central banks have almost no room for maneuver. Nevertheless, the institutional framework allows for a certain degree of resilience. The various international organizations working on financial regulation, such as the G20, the Financial Stability Board, the Bank for International Settlements, and central banks, have gained a certain degree of independence from political power.

Bibliography:

BIS, 2010, “An assessment of the long-term economic impact of stronger capital and liquidity requirements”

BSI-Economics, « Capital Markets Union: profitable but not without risk »

BSI-Economics, “In a nutshell, what is the Volcker Rule?”

ECB, 2016, “The euro area bank lending survey, Third quarter of 2016”

IMF, 2014, “Legacies, Clouds, Uncertainties,” World Economic Outlook October 2014

Korinek A. and Kreamer J., 2014, « The redistributive effects of financial deregulation, » Volume 68, Supplement, December 2014, Pages S55–S67

Minsky H., 1986, “Stabilizing an Unstable Economy,”

Moss, D., 2010, “Bank failures, regulation, and inequality in the United States,” Cambridge: Harvard Business School

Saez, E., “Striking it Richer: The Evolution of Top Incomes in the United States”, updated version of “Striking It Richer: The Evolution of Top Incomes in the United States”, Pathways Magazine, Stanford Center for the Study of Poverty and Inequality, Winter 2008, 6-7

[1] The Dodd Frank Act is a framework law that addresses, in 2,300 pages, the main issues raised by the banking and financial crisis that began in the US. See “In a nutshell, what is the Volcker Rule?” or “What can we expect from the regulation of derivatives?” (BSI Economics)

[2]See: » Capital Markets Union: profitable but not without risk , » BSI Economics

[3] Two directives in particular (December 12, 1977, and December 15, 1989) organize the freedom of establishment and provision of banking services by introducing a single authorization.