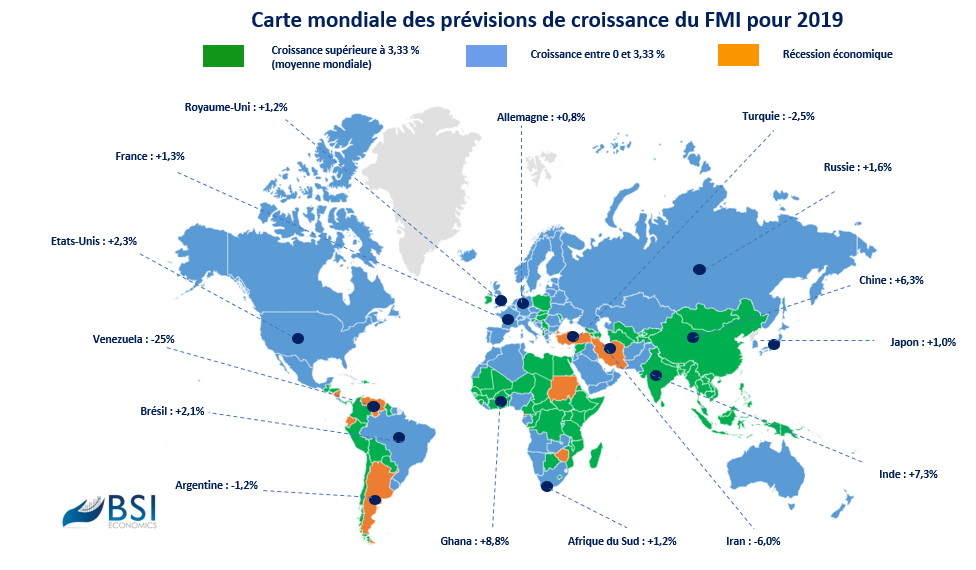

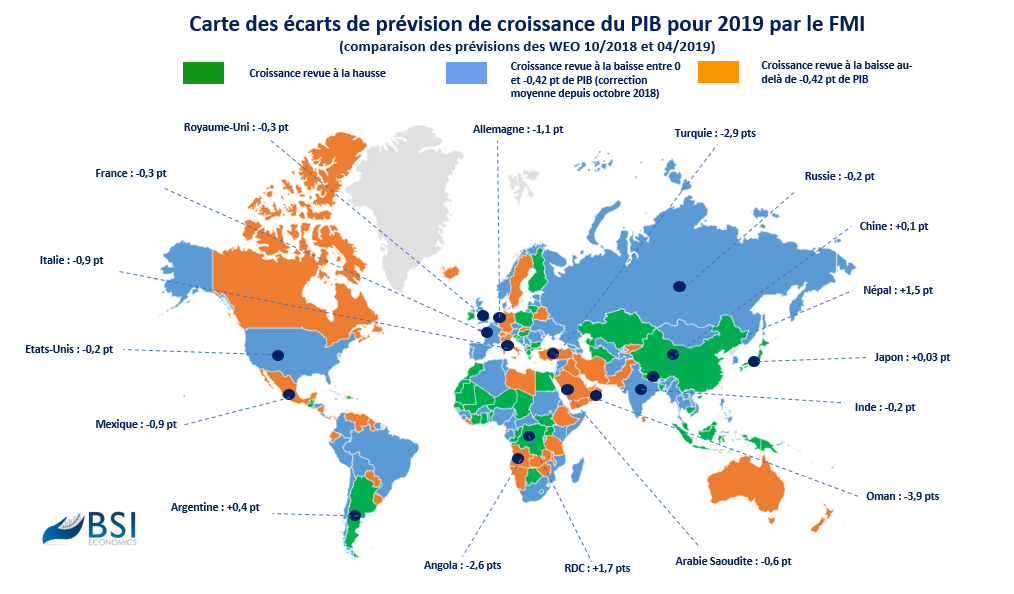

Expected to reach 3.9% in 2019, the global growth forecast has been revised down to 3.3% by the International Monetary Fund (IMF) in its April 2019 World Economic Outlook (WEO) report. Global growth will be driven mainly by emerging countries (4.4% growth on average in 2019, after 4.6% in 2018), while growth in developed countries is expected to be only 2.2% (down from 2.6% in 2018). While Asia remains the most dynamic region (6.3%), an African country is expected to record the strongest GDP growth in 2019: Ghana, with 8.8%. Sixty percent of the economies studied are expected to experience a slowdown in 2019, following the revision of global growth for 2018 (3.6% compared to 3.9% forecast in the IMF’s previous exercise in October 2018). Thirteen countries are expected to be in recession this year: Argentina, Barbados, Ecuador, Eswatini (formerly Swaziland), Equatorial Guinea, Iran, Nauru, Nicaragua, Puerto Rico, Sudan, Turkey, Venezuela, and Zimbabwe.

In developed countries, economies are close to or even above their potential growth. As a result, their position in the cycle does not give rise to hopes of a sharp acceleration in economic activity in 2019. Furthermore, confidence and production indicators for Q1 2019 have not been particularly favorable. In the eurozone, German growth is expected to slow significantly (0.8%), suffering from a decline in external demand and sluggish private growth. In France, growth is expected to remain moderate (1.3%), with social unrest having a negative impact, while Italy will face significant debt servicing costs and a considerable banking risk (0.1%). Uncertainty surrounding Brexit will also continue to pose a threat to growth in Europe, especially in the event of a no-deal exit, which remains a likely scenario.

In Japan, fiscal stimulus would only allow for a very slight rebound in growth (1.0%). In the United States, growth would remain high (2.3%) compared to other developed countries, but the effects of the fiscal stimulus in 2018 are expected to gradually fade and the partial closure of tax offices in response to the shutdown would weigh on activity.

While the figures currently point to a difficult first half of 2019, a slight rebound is expected in the second half of 2019 in developed countries, in line with monetary policies that are ultimately more accommodative than anticipated (postponement of interest rate hikes by the Fed, reinvestment of QE and TLTRO by the ECB) and cautious, particularly in Japan and the United Kingdom.

The slowdown in the Chinese economy has been evident for several years, with GDP growth expected to fall from 6.6% in 2018 to 6.3% in 2019. However, this slowdown remains under control at this stage, especially since the authorities announced monetary support (lowering of reserve requirements) and, above all, fiscal support (local government investment in infrastructure, fiscal support for purchasing power and corporate margins). Negotiations during the trade truce with the United States in Q1 2019 suggest that an agreement may be reached. A positive outcome would ease trade tensions between China and the United States and prevent a further decline in global trade, which remains the IMF’s central scenario. Nevertheless, the growth outlook remains favorable in emerging Asia, where Indian growth is expected to reach 7.3%.

In sub-Saharan Africa, growth is expected to rebound to 3.5%, compared with 3% in 2018. However, growth in Africa’s main oil-producing countries (Nigeria and Angola) has been revised downwards from 2018 estimates and is expected to remain weak in South Africa (1.2%). Despite four economies in recession (Ecuador, Argentina, Nicaragua, and Venezuela), growth is expected to increase in Latin America (1.4%), linked in particular to more favorable prospects for Brazil since the arrival of the new president. Finally, the Near and Middle East region is expected to see a decline in growth (1.5%), in a still delicate geopolitical context (e.g., Iran, which will suffer the repercussions of US sanctions) and in line with oil price forecasts (no increase compared to 2018 according to the IMF), with global demand expected to remain below supply.

On a positive note for emerging countries, portfolio investment flows were positive in Q1 2019 and the Fed’s decision not to raise interest rates should lead to investor appetite for emerging market investments. Such a scenario should reduce the likelihood of a further fall in emerging market currencies, as was the case in 2018, and would provide relief to countries with high external financing needs such as Turkey, which will nevertheless be in recession in 2019.