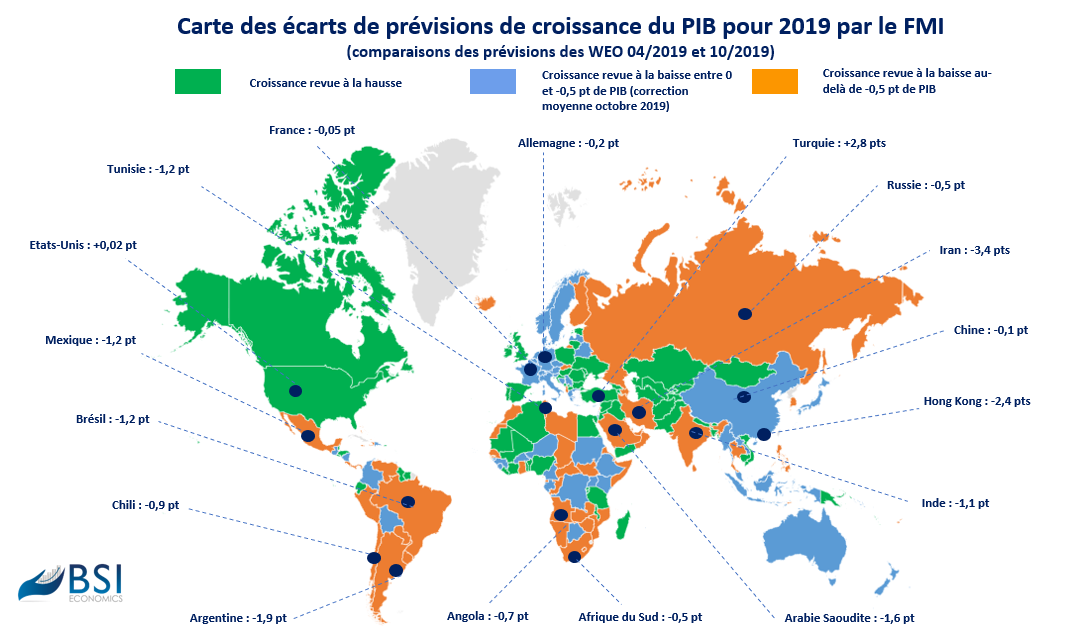

Revised downward in April 2019 compared to October 2018, the global growth forecast for 2019 was once again lowered by the International Monetary Fund (IMF) in its October 2019 World Economic Outlook (WEO). In fact, 60% of the economies studied have been revised downward by the IMF. Global growth is therefore expected to fall from 3.3% (April 2019 forecast) to nearly 3.0%, its lowest level since 2008-2009; with advanced economies (1.7%) and emerging and developing economies (3.9%) seeing their growth forecasts cut by an average of 0.1 and 0.5 percentage points, respectively.

In advanced economies, this situation can be explained in part by the slowdown in global trade, which is weighing on the manufacturing sector (notably a decline in demand for capital goods and a wait-and-see attitude that is weighing on private investment). In Europe, excluding the United Kingdom (+0.06 points), the overall trend is toward downward revisions (Germany: -0.2 points, France: -0.05 points), which remain limited due to lower dependence on external demand. The United States recorded a slight improvement (+0.02 points), in line with consumption that remains robust. In Asia, growth in Japan has been revised slightly downward (-0.09 points), South Korea (-0.6 points) is suffering from the slowdown in international trade, while the deterioration of the situation in Hong Kong justifies a sharp adjustment (-2.4 points), which could even lead the independent territory into a technical recession.

In emerging and developing economies, the changes in forecasts are varied. China is stepping up measures (fiscal and monetary support) to limit the effects of the structural slowdown in activity, exacerbated by the trade war with the United States. This situation has led the IMF to revise its forecast for the country (-0.1 points) and for Asia as a whole (-0.4 points). Latin America has seen a significant adjustment to its growth figure (-1.2 points), with the recession in Argentina and disappointing growth figures in the first half of the year (Brazil, Mexico). In Africa and the Middle East, low oil prices (Saudi Arabia, Angola), significant political/geopolitical risk (Iran, Libya) and structural weaknesses (South Africa, Tunisia) have led to downward adjustments. A situation that is ultimately less dire than expected has prompted the IMF to revise its forecast for Turkey upward (+2.8 points).

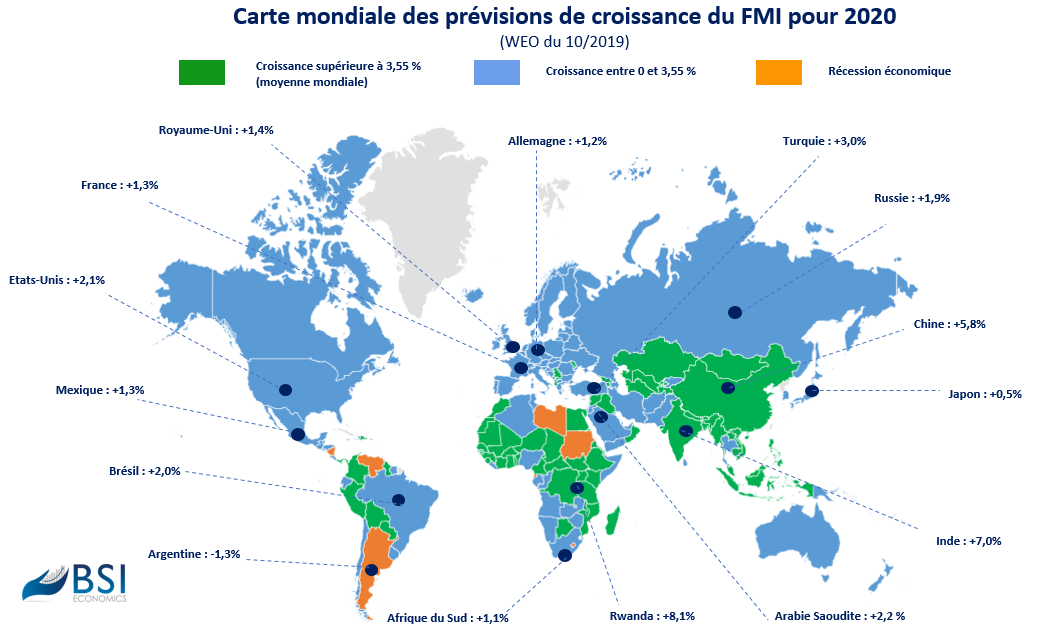

For 2020, the IMF is forecasting global growth of 3.4%, with emerging and developing economies rebounding (+4.6%) and growth in advanced economies standing at 1.7% (similar to 2019). The most dynamic regions will be Asia (+6.0%) and sub-Saharan Africa (+3.6%), but it is Latin America and the MENA region (from Mauritania to Iran) that are expected to see the strongest rebounds after disappointing figures in 2019: +1.8% and +3.2% respectively. 120 economies (62% of the total) are expected to see their activity accelerate in 2020 compared to 2019. Ten countries are expected to be in recession (Argentina, Bahamas, Equatorial Guinea, Lesotho, Libya, Macao, Nicaragua, Puerto Rico, Sudan, and Venezuela), four fewer than in 2019.

In the United States (+2.1%), a more accommodative monetary policy by the Fed and the biannual budget agreement would not only offset the negative effects of tariffs but also limit the risk of recession by prolonging the economic cycle. The presidential elections in November could be a source of uncertainty. Growth in the eurozone is expected to accelerate in 2020 (+1.4%), with a particular upturn expected in the German automotive sector (Germany: +1.2%). Despite a still very accommodative monetary policy, the lack of fiscal stimulus and persistent uncertainties surrounding Brexit do not give rise to hopes of a significant acceleration in activity (France: +1.2%, Italy: +0.5%, deceleration in Spain: +1.8%). In developed Asia, growth prospects remain heavily dependent on the evolution of external demand.

The Fed’s monetary policy easing is allowing emerging and developing economies to also opt for looser financing conditions, which is further justified by generally low and controlled inflation. These more accommodative monetary policies should stimulate economic activity and at least minimize potential losses linked to the slowdown in global trade, in the wake of the deceleration in China (+5.8% in 2020). Constraints linked to already high debt levels limit the possibilities for a less severe slowdown in China. While the extent of this slowdown will determine the performance of Asian countries, several countries are expected to be particularly dynamic in 2020, notably India (+7.0% thanks to recent economic measures: business climate, corporate taxation, support for rural consumption), Vietnam (+6.5%) and Bangladesh (+7.4%). In other major emerging economies, growth prospects remain moderate due to vulnerabilities: fiscal in Brazil (+2.0%) and Mexico (+1.3%), dependence on raw materials in Nigeria (+2.5%), Russia (+1.9%) and the Gulf countries, and multiple issues in South Africa (+1.1%).. Eastern European countries are expected to continue to post robust growth (Poland: 3.1%, Hungary: 3.3%, Romania: 3.5%), while the resilience of the Turkish economy should enable it to return to higher growth in 2020 (Turkey: +3.0%).