Summary:

– In its October 17 press release, the ECB clarified the information that banks must provide to it in view of the use of ELA.

– The prolonged use of ELA during the eurozone crisis highlighted the need to establish a broader and more transparent automatic mechanism to support bank liquidity in times of stress.

– At the same time, the second pillar of the Banking Union (SRM) seems set to take over from ELA in its « misused » function as an exceptional bank rescue fund.

In a normal situation, the ECB ensures the liquidity of the interbank market by setting key interest rates (refinancing rate, marginal lending facility rate, and deposit facility rate) at which banks can obtain (or deposit) liquidity, while ensuring price stability. Banks refinance themselves directly with the ECB mainly throughopen market operationsand standing facilities. Both of these operations are granted to banks in exchange for collateral. The ECB assesses the quality of the assets deposited as collateral and applies haircuts. However, despite the relaxation of collateral rules in response to the eurozone crisis, the collateral provided by banks in peripheral countries was no longer accepted by the ECB, making it impossible for them to obtain refinancing from the ECB. As a result, national central banks intervened as lenders of last resort throughEmergency Liquidity Assistance (ELA), which allows them to temporarily provide liquidity to banks that no longer have access to financial markets and can no longer obtain financing from the ECB. However, given the poor quality of collateral, the significant increase in non-performing loans in banks’ assets, and overall tensions in the money markets, interest rates on ELA operations are penalizing, at around 100 to 200 basis points above the ECB’s refinancing and marginal lending facility rates.

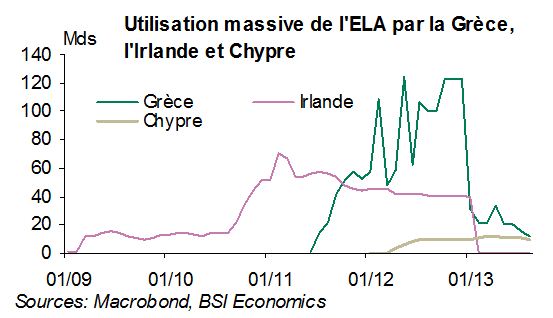

Until now, the functioning of ELA has been opaque. The ECB explained that its use was limited to « exceptional circumstances » and concerned « institutions or markets that were temporarily illiquid but not insolvent. »However, the ELA mechanism was widely used as an additional bank rescue fund during the eurozone crisis, where negotiations with the European Commission and the IMF were insufficient, particularly in Greece, Ireland, and Cyprus. The amounts of ELA operations reached €123 billion in Greece (September 2012), €70 billion in Ireland (February 2011) and €11.7 billion in Cyprus (March 2013), which means that without this contribution, the situation of banks in these countries could have been very different. The massive use of ELA during the eurozone crisis calls into question its definition, particularly its « temporary » nature, the solvency of the credit institutions that benefited from it, and above all the « sole » responsibility of states. For example, the Central Bank of Ireland used ELA for several months before the ECB allowed it to end after reaching an agreement with the Irish government last February to exchangepromissory notes for long-term government bonds to refinance the banks.

The ECB’s publication on Friday, October 17, of details on the regulation ofEmergency Liquidity Assistance ( ELA) reflects the ECB’s supervision of ELA.In order to use ELA, banks must provide the ECB with: the characteristics of the transaction (maturity, amount, currency, interest rate, name of the counterparty), a description of the collateral backing the transaction, the reasons for the transaction, and also the criteria for analyzing solvency and an analysis of the potential systemic risk. But what about the creditworthiness of the governments guaranteeing their central banks’ ELA operations? The ECB has stated that the risk of default associated with collateral deposited and held by national central banks is the sole responsibility of governments. But if the government were unable to meet the financing needs of local banks, would the ECB allow them to go bankrupt at the risk of destabilizing the entire European banking system? This possibility seems to contradict Mario Draghi’s insistence on the « irreversibility of the euro » and the ECB’s asset purchase program (OMT), suggesting that the « sole » responsibility of governments could be reconsidered.

A more credible solution could be provided by the banking union. Starting in November 2013, the ECB will conduct a Comprehensive Assessment, including a review of bank balance sheets (AQR) and stress tests on the 130 largest banks in the eurozone. In addition, the European Banking Authority (EBA) will develop « single rules » for the banking system aimed at ensuring convergence and consistency in supervisory practices. Ultimately, the Single Supervisory Mechanism (SSM) announced for November 2014, prior to the introduction of the SRM, should prevent stress situations on the interbank market (see article The single supervisory mechanism has arrived).In addition, the Single Resolution Mechanism (SRM), the second pillar of the banking union, should include the establishment of national and European resolution funds to limit risk pooling in the event of bank failures. These resolution funds would enable the refinancing of illiquid banks without running the risk of increasing and deteriorating the balance sheets of national central banks, which are the responsibility of the states.The SRM could become the benchmark mechanism for managing banking crises, allowing for greater responsiveness and transparency on the one hand, and providing a legal framework validated by all Member States on the other. In the event that this mechanism is not sufficient to avoid a situation of extreme stress, the SRM and ELA could be complementary.

However, the terms and conditions for implementing the SRM and the firepower of these national resolution funds are not yet known. Negotiations on their implementation are likely to be relatively lengthy despite the urgency, due to the political dimension of the issue of financial and banking integration in the eurozone. If European negotiations stall and the SRM never sees the light of day, then the ECB’s efforts to achieve financial stability and banking integration will be undermined and the banking union will be in vain.