Summary:

· At the end of 2015, the election of President Mauricio Macri marked a turning point in Argentina’s economic policy;

· The new government’s reforms have improved national competitiveness and created a business climate that is more favorable to domestic and foreign investors;

· Combating inflation is now the Central Bank’s priority. The goal is to achieve an inflation rate of between 12% and 17% in 2017, moving towards 5% by 2019, compared with around 40% in 2016.

· Nevertheless, the country fell back into recession in 2016 with real GDP growth of around -2.4% and a primary fiscal deficit that widened to -4.6% of GDP. The economic transition is having negative short-term impacts that require the implementation of measures to protect the most vulnerable.

Since the election of President Mauricio Macri in November 2015, Argentina has entered a phase of profound economic restructuring. Fighting inflation, rebalancing public accounts, restoring competitiveness… the challenges are many. However, it is clear that, initially, the reforms designed to turn the country around are having a negative impact on the economy (J-curve). The government is therefore faced with the following problem: « How can economic adjustment be achieved while minimizing the recessionary effect and short-term social costs? »

1. Review of the economic situation from 2002 to 2015

After being hit by a severe financial crisis in 2002, Argentina experienced a period of very sustained growth. From 2003 to 2012, real GDP grew by an average of 7.2% per year, leading to a significant reduction in the poverty rate (27.3% at the end of 2015 compared to 60.3% at the end of 2003). The surge in food prices from 2003 onwards contributed significantly to Argentina’s economic takeoff, given that raw and processed agricultural products account for around 60% of domestic exports.

However, economic distortions accumulated and food prices fell from 2012 onwards. As a result, in 2015, the Argentine economy suffered from numerous imbalances characterized by high consumption, underinvestment, rising inflation, and high tax pressure (see Figure 1). The federal budget deficit rose from 2.6% in 2011 to 6.6% in 2015. Over the same period, Argentina experienced two years of recession. Between 2009 and 2014, the average annual growth rate in real terms did not exceed 1.5%.

Figure 1: Structural imbalances in the Argentine economy in 2015

*Average investment rate in Latin America in 2013

Source: IMF – CEPAL / Prepared by: BSI Economics

At the same time, the state was omnipresent due to the introduction of price controls, export and import taxes, and capital controls. Exchange controls led to the overvaluation of the Argentine peso and the emergence of a parallel market where the exchange rate was higher than the official rate (around +50%). It is also worth noting the loss of credibility of institutions such as INDEC[1].

The country did not have access to international capital markets, mainly because of disputes with « vulture funds, » i.e., creditors who did not accept the restructuring of Argentina’s debt between 2005 and 2010. The vulture funds then took legal action and referred the matter to ICSID[2] to obtain repayment of their claims as well as interest and compensation. President Cristina Kirchner refused to « compensate » the vulture funds even though Argentina had been found liable. With the blocking of restructured creditor repayments following the US Supreme Court’s decision, Argentina found itself in a situation of partial default on its sovereign debt.

This dispute prompted Argentina to resort to monetizing its debt. The Central Bank bought government-issued securities by printing money. This is known as the « money printing » mechanism, which led to an increase in the money supply and , ultimately, higher inflation.

We have witnessed a decline in Argentina’s competitiveness, which now ranks104thand 116th in the Global Competitiveness Report and Ease of Doing Business rankings, respectively. As a result, exports accounted for only 12% of GDP in 2015, compared with an average of 24% for Latin America (see Figure 1).

2. Structural reforms

In order to rebalance public accounts in the medium term, the government has decided to cut public spending, which is among the highest in Latin America (see Figure 1). According to the IMF, federal debt is expected to gradually decline from 52% of GDP in 2015 to 50% in 2019 thanks to the reforms undertaken by the new government. Upon taking office, Mauricio Macri canceled the hiring of 10,000 civil servants, whose numbers had steadily increased to 3.9 million (+1.6 million between 2001 and 2014). The reduction in subsidies that kept energy prices artificially low also helped to reduce spending. This is a major issue, as this public funding represented 4% of GDP in 2015.

In addition, restoring national competitiveness has become a priority objective. The elimination of export taxes and the 40% depreciation of the Argentine peso caused by the lifting of exchange controls have led to a resurgence in the price competitiveness of domestic exports (+1.7% in 2016). The 6.6% drop in industrial exports was more than offset by a 17.7% increase in sales of Argentine primary products abroad. As a result, in 2016, the trade balance returned to surplus (+USD 2.1 billion), despite the partial lifting of import restrictions.

At the same time, the new government is pursuing a pro-investment policy. In the first three quarters of 2016, tax cuts reduced the tax burden by 0.5% of GDP. Among the new measures are, for example, tax deductions of 10% for any new investment made by an SME. Capital controls have been relaxed, as they discouraged foreign investors by preventing them from freely repatriating capital from subsidiaries to their parent companies. More broadly, the government is attempting to regain the confidence of domestic and international investors by restoring the credibility of institutions and offering guarantees of fiscal stability, for example for investments by micro-enterprises and SMEs made between July1, 2016, and December 31, 2018.

However, these structural adjustments and disinflation (which we will return to later) resulted in an estimated 2.4% recession in real GDP in 2016 and a 6% loss in purchasing power, leading to the introduction of measures to protect consumers and the most vulnerable social classes. The authorities have introduced an increase in pensions and unemployment insurance. The government is also considering a comprehensive tax reform that would restore the progressivity of taxation. Prior to 2016, tax thresholds had not been adjusted in line with inflation, which led to an erosion of tax progressivity.

3. Changes in the monetary and financial system

One of the first measures adopted by Mr. Macri’s government was the removal of exchange controls. In mid-December 2016, the return to a quasi-floating exchange rate regime immediately resulted in a sharp depreciation of 40%.

Furthermore, the main objective of monetary policy is now to combat inflation, which necessarily involves gradually ending the monetization of debt. This meant that new sources of financing had to be found. The government decided to repay and compensate vulture funds in order to enable the country to return to the international financial markets. In fact, in 2016, Argentine treasury bill issues were very successful with international creditors.

In addition, monetary policy was modernized. The Central Bank set inflation targets and adopted a new instrument introduced in 2016 called the LEBAC rate. Each month, the monetary authorities issue debt[5] purchased by creditors and remunerated at the LEBAC rate. This mechanism allows money to be withdrawn from circulation in order to curb inflation.

Inflation in year t (TTt) depends on expected inflation (TTet). The higher TTe is, the more workers will demand significant wage increases and the more price makers will raise the prices of the products they sell. Suppose that the central bank sets an inflation target (TTt*) lower than the previous year’s inflation (TTt-1). TTet will therefore depend on the credibility of the central bank (see table below).

|

Credibility of the Central Bank |

Expected inflation |

|

Total |

TTet=TTt*(forward-looking expectations) |

|

Zero |

TTet=TTt-1 (retrospective expectations) |

Source: BSI Economics

We note that when monetary authorities are credible, TTet is lower because TT*<TTt-1. The success and cost of a disinflation program therefore depend on the credibility of monetary authorities and their ability to influence agents’ expectations. This is why the Argentine Central Bank is seeking to demonstrate its determination to fight inflation. The introduction of an inflation target, the creation of a key interest rate (the LEBAC rate), and the gradual phasing out of money printing seem to be bearing fruit at this stage. A growing number of economic agents are adopting « forward-looking expectations » as they gradually realize that the Central Bank will not deviate from its commitment.

Initially, the new president’s arrival in power led to a sharp rise in inflation. On the one hand, the removal of exchange controls led to a depreciation of the national currency, thereby increasing the cost of imported goods (imported inflation). On the other hand, the reduction in energy subsidies led to an increase in water, gas, and electricity prices (e.g., the price of electricity jumped 245% in February 2016 compared to September 2015).

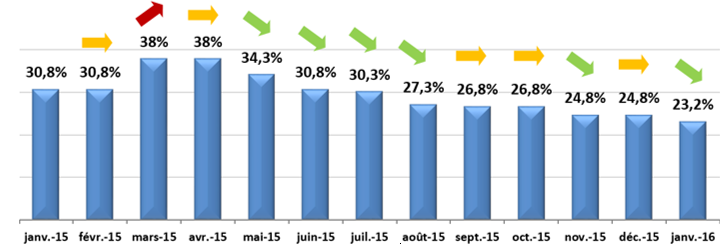

Nevertheless, monetary policy reforms have led to a gradual decline in the monthly inflation rate, which fell from 4.2% in May 2016 to 1.2% last December. In order to avoid a surge in real interest rates due to falling inflation, the Central Bank lowered its key interest rate in order to bring down nominal interest rates. As a result, the 35-day LEBAC interest rate fell from 38% at the end of February 2016 to 23.2% in January 2016 (see Figure 2).

Figure 2: Change in the key interest rate (35-day LEBAC rate[7])

Sources: Central Bank of Argentina, BSI Economics

In addition, the Fed has announced three Fed funds rate hikes in the United States for 2017. There is therefore a risk of seeing a net outflow of capital from Argentina, attracted by higher yields in the United States. The decline in demand for the Argentine peso would then lead to depreciation, which would fuel imported inflation.

Conclusion

The new government has inherited an economic situation marked by deep structural imbalances. It has undertaken a wide-ranging program of fiscal, regulatory, and monetary reforms. Since the end of 2015, the country has therefore been undergoing a process of economic transformation, the transition phase of which is generating negative short-term impacts that require protection for the most vulnerable social classes.

Nevertheless, these measures appear to be essential and have already significantly improved Argentina’s economic outlook, with long-term growth potential now standing at 3% according to the IMF.

[1] National Institute of Statistics

[2] International Centre for Settlement of Investment Disputes

[3]Except for soy products and leather.

[4]Example: Individual X’s income is EUR 1,000, a 10% increase over the previous year, while inflation has risen by 10% over the same period. X’s purchasing power has therefore not changed. However, if income tax thresholds have not been adjusted by 10%, individual X may move into a higher tax bracket simply because their nominal income has increased. The tax system then loses its progressivity.

[5]Debt issuance (LEBAC) has been monthly since February 2017. From January 2016 to January 2017, it was weekly.

[6]Real interest rate = nominal interest rate – inflation

[7]The rate shown in this graph is that of the last weekly issue of each month.