Usefulness of the topic: This article aims to understand the role of inheritance and gifts in determining the distribution of wealth, to identify which French households are currently affected by inheritance and gift tax, to assess how France compares to other OECD countries in terms of inheritance and gift taxation, and to analyze several possible changes to the current tax system.

Summary:

- The wealth of French households is very unevenly distributed across the population: in 2018, half of households held 92% of gross wealth. These wealth inequalities have increased significantly over the past 20 years.

- There is a distortion in the distribution of household wealth in favor of the elderly, which is likely to contribute to a significant increase in transfers in the medium to long term. Transfers will therefore continue to play a key role in determining the distribution of household wealth over the coming decades.

- While the marginal tax rate[1] on gifts and inheritances appears high, the effective tax rate actually shows that allowances and exemptions lead to a sharp reduction in the rate actually paid. However, there is a significant difference in taxation between direct (parents, grandparents) and indirect transfers.

- In international comparisons, France stands out for its high maximum marginal tax rates. This is largely due to the continued significant differentiation in taxation between direct and indirect lines. Nevertheless, the French taxation system, which is progressive in its scale, is characterized by significant exemption or exemption mechanisms.

- While inheritance and gift tax is justified economically, both from the point of view of fairness and efficiency, the current system needs to be rethought in order to move closer to optimal taxation.

The reform of inheritance tax has become a key issue in the presidential campaign: while candidates on the right of the political spectrum are proposing to reduce the tax burden on inheritance, candidates on the left want to make the system more redistributive.

Inheritance tax is one of the least popular taxes in France: 87% of French people would be in favor of reducing it. This unpopularity could be explained by an overestimation of the burden of inheritance and gift tax.

According to the same study, French people estimate on average that transfers between two married or civil union partners are taxed at 22%, even though they have not been taxed since 2007. Inheritance tax is also often criticized as constituting double taxation. This may be the case from the point of view of the person giving or transferring the assets, who may already have been subject to income tax. However, this is not the case from the point of view of the individual receiving or inheriting the assets. Furthermore, in many situations, inheritance tax allows income that has never been taxed[3] to be taxed, in particular unrealized capital gains[4].

This article aims to understand the role of inheritance and gifts in determining the distribution of wealth, to identify which French households are currently affected by inheritance and gift tax, to assess how France compares to its neighbors in terms of gift and inheritance taxation, and to analyze possible developments in inheritance and gift taxation in France.

1. Changes in French household wealth and the role of inheritance in the distribution of wealth

a. Uneven distribution of wealth within the population

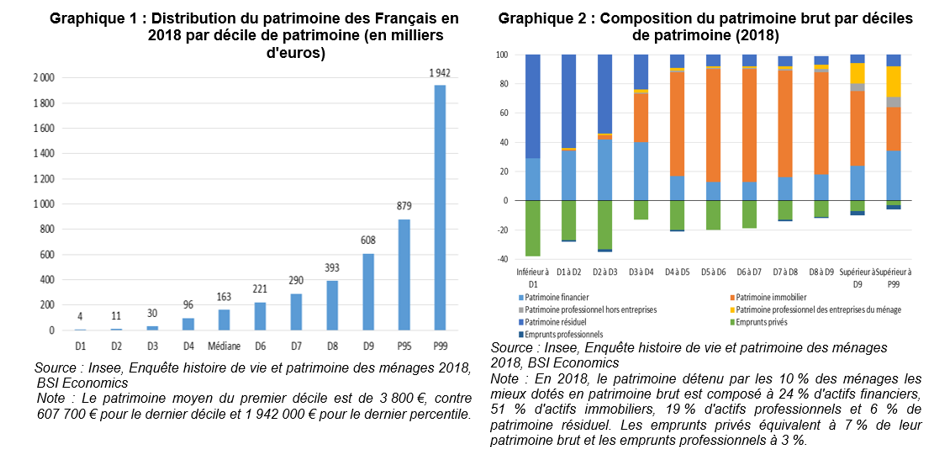

In 2018, French household wealth averaged €276,000, but was very unevenly distributed among the population: half of households held 92% of gross wealth[5]. The average wealth of households in the first decile is €3,800 and the median wealth is €163,100, compared with €607,700 for the last decile and €1,942,000 for the last percentile (Figure 1).

In 2018, according to INSEE, 61% of French people’s gross wealth consisted of real estate, 20% of financial assets, 11% of business assets, and 8% of residual assets. However, the composition of wealth varies greatly depending on the level of wealth of individuals: households at the bottom of the distribution favor liquid savings vehicles, such as regulated savings accounts, hold little or no real estate assets, and are more indebted (Chart 2). Conversely, real estate accounts for more than 60% of assets for the top five deciles. At the top of the distribution, savings vehicles are more diversified: 54% of financial assets are held by the wealthiest 5% of households (compared with 28% for real estate).

Wealth inequality has increased significantly over the past 20 years: the 10% of households with the lowest level of wealth saw their gross wealth decline by 48% between 1998 and 2018, while that of the top decile increased by 119% in current euros. This increase in wealth inequality is mainly due to the sharp rise in the value of real estate assets (+141%), particularly in the early 2000s, which benefited the wealthiest households.

Thus, in 2018, 62% of wealth inequality as measured by the Gini index[6] was due to real estate wealth, compared with 55% in 1998. This is explained by the increase in the share of real estate wealth in total wealth for households in the middle and upper parts of the distribution. At the same time, 23% of wealth inequality is attributable to financial wealth (26% in 1998).

b. A distortion in the distribution of wealth in favor of the elderly

The increase in wealth observed over the last twenty years has benefited individuals over the age of 60 more than others. Seniors have benefited from the economic boom of the 1950s to 1970s to accumulate wealth. In addition, most of them became homeowners before 2000 and benefited from the real estate boom of the 2000s. Furthermore, a quarter of households living in France own several properties and hold two-thirds of the homes owned by private individuals.

According to France Stratégie[7], inheritance is being received later and later—around age 50 today—due to increased life expectancy. However, this trend is offset by an increase in donations.

This distortion in the distribution of household wealth in favor of the elderly, combined with the aging of the baby boomer population, is expected to contribute to a significant increase in transfers in the medium to long term. According to France Stratégie, these transfers accounted for 19% of net disposable income in 2017, compared with only 8.5% in the early 1980s, and this share could reach 31% in 2050. According to the Economic Analysis Council, inherited wealth now accounts for 60% of total assets in France, compared with 35% in the early 1970s.

Transfers will therefore continue to play a key role in determining the distribution of household wealth over the coming decades. If the significant contribution of transfers to household disposable income persists, inheritances could contribute to maintaining wealth inequality in the medium term.

2. What is the tax treatment of inheritances and gifts in France?

The flow of transfers has risen sharply in recent decades: it amounted to €250 billion in 2015, compared with €60 billion in 1980.

While 43% of French households report having received at least one inheritance during their lifetime, this proportion rises to 37% for the top two income deciles, compared with 55% for the bottom two deciles[8]. The average amount of inheritance received by the top two deciles is €70,000, compared with €140,000 for the bottom two deciles.

a. What tax regime applies to inheritances and gifts in France?

The existence of inheritance and gift taxes (known as transfer duties on gifts – DMTG) contributes to the redistributive function of the tax system. Transfer duties on gifts (DMTG) brought in €18.7 billion to the State in 2021, including €14.8 billion for inheritance tax and €3.9 billion for duties on « inter vivos transfers , » which is a historic high, due in particular to a post-crisis catch-up phenomenon on gifts and excess mortality linked to the Covid crisis on inheritances.

While the marginal tax rate on gifts and inheritances appears high (see details of the scale in Appendix 1), the effective tax rate actually shows that allowances and exemptions lead to a significant reduction in the rate actually paid.

Under current legislation, parents can give or transfer up to €131,865 tax-free to a child every fifteen years. The exemption associated with gifts of money to children, amounting to €31,865, is cumulative with the €100,000 allowance on gifts from parents to children. Similarly, the tax-exempt amounts reach €63,730 every 15 years for a gift or transfer to grandchildren (see details of existing allowances in Appendix 1).

In addition to allowances based on family ties, there is a specific scale applicable to life insurance, namely an allowance of €152,500, regardless of family ties, with a marginal tax rate of 20% up to €700,000 and 31.25% above that amount. A 75% allowance is applied to the transfer of business assets (Pacte Dutreil) and certain assets (forests, farmland). Finally, bequests to recognized public interest organizations benefit from a special regime and may be exempt from inheritance tax under certain conditions.

b. Which households are actually affected by inheritance tax in France?

Ultimately, the average inheritance tax rate is 10%, with a notable difference between direct and indirect inheritances, whose average rates are 8% and 32% respectively[9].This difference can be explained by the differences in allowances, which vary from €100,000 for direct line heirs to €1,594 for non-relatives, as well as by differences in tax scales. In 2019, the proportion of estates subject to tax was 24% for direct line heirs and 59% for indirect line heirs.

In addition, the effective progressivity of inheritance tax is limited for indirect lines, with a stable average tax rate of around 33% for amounts above €200,000. For direct lines, progressivity is more pronounced, with an average tax rate increasing up to €1 million, where it stands at 15%.

This low progressivity of inheritance tax is explained in particular by the use of assets benefiting from allowances, particularly life insurance and professional assets (Charts 3 and 4), which represent 19% and 8% of the inheritance tax base, respectively. In fact, the share of assets benefiting from exemptions is 10 points higher in the top decile of estates than the average for all estates.

c. France stands out for its high marginal tax rates in international comparisons

In 2018, France ranked third in the OECD in terms of inheritance and gift tax revenue as a percentage of total revenue, behind Belgium and South Korea.

Within the OECD, 24 out of 36 countries tax transfers of wealth between individuals. However, over the past 20 years, many countries have abolished or significantly reduced inheritance taxation. Since 1965, within OECD countries, revenue from inheritance and gift taxes—which are based on property transfers following a gift or inheritance—as a percentage of GDP has fallen fourfold, from 1.1% to 0.4% (0.6% in France today).

This downward trend does not extend to France, where the share of DMTG revenues has tended to increase over the long term as a percentage of GDP: DMTG revenues reached 0.6 percentage points of GDP in 2019, compared with 0.15 percentage points of GDP in 1960[10]. This increase in revenue as a percentage of GDP can be explained in particular by the growth in inheritance flows over the period and by the progressivity of the DMTG scale. Compared to other OECD countries, French households are more likely to receive an inheritance (through inheritance or donation). This can be explained in particular by a more rapid increase in the wealth held by French people: between 1995 and 2019, per capita wealth almost tripled in France. The rise in asset prices (housing and shares) is an important factor in this growth. In 2014, 43% of households reported having received at least one inheritance during their lifetime, 10 points above the OECD average. The average transfer received by a French household is €135,400, which is in line with the OECD average.

While France has high levels of taxation compared to its neighbors, this is largely due to the continued significant differentiation between direct and indirect taxation. In addition, the French tax system, which is progressive in terms of its scale, remains characterized by significant exemptions and exemptions (life insurance, dismemberment of property, transfer of family businesses, etc.), which reduce the effective level of taxation (see section b).

3. What are the possible avenues for change in inheritance and gift tax?

a. Taxation that is desirable from the point of view of fairness and economic efficiency…

From an equity perspective, inheritance tax is a policy that promotes equal opportunities, reducing differences in living standards and wealth linked to birth. Several studies highlight the effectiveness of inheritance tax in limiting wealth inequality in the long term[11]. From an efficiency standpoint, inheritance taxes can have behavioral effects that reduce the tax base and ultimately lead to costs for public finances. Nevertheless, inheritance taxation is often favored by economists for its low behavioral effects:

- The impact of taxation on taxpayer mobility is thought to be low[12]. Several empirical studies based on Swiss and US tax data show that an increase in inheritance tax has a positive but limited impact on mobility[13]. Nevertheless, the impact on mobility would be significant for billionaires. However, these studies only look at mobility within the same country (US states or Swiss cantons) and at small variations in tax rates. This migratory constraint can, however, be controlled by specific measures, such as a system based on citizenship or long-term residence.

- Increasing inheritance tax has theoretically ambiguous effects on savings and labor supply. Economic literature highlights the positive impact of inheritance tax on incentives to participate in the labor market[14]. Furthermore, studies conducted in the French context[15] suggest that the effects on savings and consumption are, in principle, rather weak, but knowledge about the heterogeneity of these behavioral responses across the distribution of inherited resources is limited.

Thus, while uncertainties remain about the extent of certain behavioral responses, the results of studies on optimal taxation show that inheritance taxation is desirable.

b. … Which should be rethought?

To address the challenges of increasing inequality in access to inherited wealth and improve the efficiency of inheritance and gift taxation, several proposals have emerged in the public debate:

i. Base the taxation system on the total flow of transfers received by an individual throughout their life

Under the current system, each transfer is taxed separately, which allows individuals to benefit from certain allowances several times and optimize the timing of transfers, given that a tax recall occurs every 15 years. The introduction of a tax base based on the total amount of inheritance received by an individual throughout their life would make it possible to better assess the contributory capacity of heirs. In this system, the tax rate would depend solely on the value of the inheritance received, regardless of how and when the assets were transferred. The amount of allowances could then be rethought so that the reform would be socially acceptable and neutral for public finances, thus offering the opportunity to tax better without taxing more.

The introduction of a « lifetime tax recall » would allow all transfers received during an individual’s lifetime to be taken into account in the calculation of gift/inheritance tax, whereas the current 15-year tax recall primarily benefits large estates, which are encouraged to optimize their tax situation. Such a measure would promote equal opportunities. However, its impact on intergenerational inequalities would be ambiguous, as the effects of behavior are difficult to anticipate: it could encourage larger donations, as households would have less incentive to delay their donations in order to benefit from new allowances, but it would remove the incentive to donate every 15 years. The transition to a beneficiary-centered scale would strengthen equal treatment between beneficiaries, who are on average younger than donors.

In addition, such a system would have the advantage of being neutral in terms of the nature of the family ties between donors and heirs: inheritances received in direct and indirect lines would be treated identically, thereby eliminating the significant distortions in the current French system, the legitimacy of which may be called into question by changes in family structures.

ii. Abolish certain exemption mechanisms whose economic justification is limited, in order to strengthen the effective progressivity of inheritance taxation

The special tax scale for life insurance, which currently allows for an additional allowance of €152,500 regardless of family relationship, would be justified by (i) the objective of long-term asset holding to finance the economy and (ii) the desire to respond to changes in family composition and to make gifts and bequests outside the direct line under more favorable tax conditions.

Nevertheless, while the existence of such a mechanism mainly benefits the wealthiest taxpayers and undermines the progressivity of the effective tax rate[16], its economic justification can be questioned. Indeed, the existence of a special tax scale does not fully meet the objective of long-term asset holding, which is more conducive to financing the economy (80% of savings invested in euro-denominated funds, mainly in bonds rather than equity). The elimination of this tax advantage could thus make life insurance less attractive in favor of savings products that are better suited to contributing to the financing of the economy, but with effects that are diluted over time and difficult to predict. In addition, the introduction of a common tax scale for direct and indirect descendants would better respond to changes in family structures.

Furthermore, the economic justification for exemptions for business assets (Dutreil schemes) is also limited. The transfer of business assets is a major issue for family businesses, as the application of the common law regime may force heirs to sell the business to pay inheritance tax. However, the economic relevance of measures to promote the transfer of family businesses is a matter of debate. In particular, available studies conclude that when one of the heirs or donees takes on management functions, the performance of the businesses concerned declines[17], which may raise questions about this particular feature of the French system.

Conclusion

While wealth inequality has increased significantly over the past 20 years and French household wealth is very unevenly distributed, transfers will continue to play a key role in determining the distribution of household wealth over the coming decades, even though France is the second lowest-ranked OECD country in terms of intergenerational mobility[18], behind Hungary: it takes more than six generations in France for a person at the bottom of the income distribution to reach the average (compared to 4.5 generations on average in OECD countries).

Inheritance and gift tax, which contributes to the redistributive function of the tax system, results in high marginal tax rates, particularly when compared internationally. The existence of significant allowances and exemptions nevertheless leads to a sharp reduction in the rate actually paid by taxpayers, but there is a significant divergence between the taxation of direct and indirect transfers. Several avenues for reform deserve to be explored in order to enhance the fairness and efficiency of gift and inheritance taxation, including (i) a thorough overhaul of the current system, proposing to tax the total flow of transfers received by an individual throughout their lifetime, and (ii) the elimination of exemptions with limited economic justification.

Appendix 1

Bibliography

« Household income and wealth, » 2018 edition, INSEE References collection, INSEE.

« Tax trends in the European Union, 2020 edition, » European Commission.

« Inheritance Taxation in OECD Countries, » OECD (2021)

« Rethinking inheritance: additional analyses, » Focus No. 77-2021, Economic Analysis Council

Akgun, O., B. Cournède and J. Fournier (2017), « The effects of the tax mix on inequality and growth,« OECD Economics Department Working Papers, No. 1447.

BachL. (2009), « Are hereditary business transfers less effective? The case of France between 1997 and 2002, » Revue Économique, 60 (3), 787-796.

Balestra C. and R. Tonkin (2018), “Inequalities in household wealth across OECD countries: Evidence from the OECD Wealth Distribution Database,” OECD Statistics Working Papers, No. 2018/01, OECD, Paris.

Laurence Boone (2019), « France, inequality, and social mobility, » OECD

Boadway R., Chamberlain E. and C. Emmerson (2010), “Taxation of Wealth and Wealth Transfers,” in Dimensions of Tax Design.

Brülhart M. and R. Parchet (2014), “Alleged tax competition: The mysterious death of bequest taxes in Switzerland,” Journal of Public Economics, Vol. 111, pp. 63-78.

Brülhart M., Gruber J., Krapf M., K. Schmidheiny (2019), “Behavioral Responses to Wealth Taxes: Evidence from Switzerland,” CESifo Working Paper Series 7908, CESifo.

Cowell, F., D. Van De Gaer and C. He (2017),“Inheritance Taxation: Redistribution and Predistribution”

Dherbécourt C. (2019), “The long-term evolution of wealth transfers and their taxation in France,” Revue de l’OFCE, 161.

Dherbécourt C. (2017a) “Can we avoid a society of heirs?”, France Stratégie Analysis Note, No. 51.

Elinder, M., O. Erixson and D. Waldenström (2018), “Inheritance and wealth inequality: Evidence from population registers,” Journal of Public Economics, Vol. 165, pp. 17-30

Gale W. and J. Slemrod (2001), “Rethinking Estate and Gift Taxation,” NBER Working Paper No. 8205, p. 532

Goupille-Lebret J. and J. Infante (2018): « Behavioral Responses to Inheritance Tax: Evidence from Notches in France, » Journal of Public Economics, No. 168, pp. 21-34.

Kindermann, F., L. Mayr and D. Sachs (2020), “Inheritance taxation and wealth effects on the labor supply of heirs,” Journal of Public Economics, pp. 104-127.

Kleven H., C. Landais, M. Muñoz and S. Stantcheva (2020): « Taxation and Migration: Evidence and Policy Implications, » Journal of Economic Perspectives, vol. 34, no. 2, pp. 119-42.

Grégoire Marchand P. (2017), « La fiscalité des héritages : connaissances et opinions des Français » (Inheritance taxation: knowledge and opinions of the French), Working Paper, France Stratégie.

Moretti E. et al. (2020), “Taxing Billionaires: Estate Taxes and the Geographical Location of the Ultra-Wealthy,” IZA Discussion Paper No. 12699.

Piketty T. (2010), « On the Long-Run Evolution of Inheritance: France 1820–2050, » PSE Working Paper.

Piketty T. and E. Saez (2013), “A Theory of Optimal Inheritance Taxation,” Econometrica, Vol. 81/5, pp. 1851-1886.

Veillon P. (2021), “Microsimulation models of taxes on household wealth, DG Trésor,” Working paper from the French Treasury.

[1]Rate at which the last tranche of transferred income is taxed.

[2]Grégoire Marchand (2017), « La fiscalité des héritages : connaissances et opinions des Français » (Inheritance taxation: knowledge and opinions of the French), Working paper, France Stratégie

[3]Gale and Slemord (2001), Boadway (2010).

[4]The unrealized capital gain corresponds to the capital gain realized between the purchase of an asset and the death of the individual.

[5]Gross wealth is the total amount of assets held by a household, i.e., all the assets that will provide it with future resources. It includes financial assets, real estate, and professional assets, as well as durable goods (cars, household equipment, etc.), jewelry, works of art, and other valuables.

[6]The Gini index measures the degree of inequality in a distribution (of income, wealth, etc.) for a given population. It varies between 0 and 1, with 0 corresponding to perfect equality (all households have the same income) and 1 to extreme inequality (one household has all the income, while the others have nothing).

[7]Dherbécourt Clément (2017) « Can we avoid a society of heirs? », France Stratégie analysis note, no. 51

[8]Balestra and Tonkin, 2018, OECD: Inequalities in household wealth across OECD countries: Evidence from the OECD Wealth Distribution Database

[9]« Microsimulation models of taxes linked to household wealth, » DG Trésor working paper, December 2021

[10]They have increased by 0.24 percentage points of GDP since 2010, as a result of successive reforms in 2011 and 2012. However, they fell sharply between 2007 and 2010 following the introduction of the TEPA law, which increased the direct line allowance to €150,000 and reduced the tax recall period on gifts to six years.

[11]Elinder, M., O. Erixson and D. Waldenström (2018), « Inheritance and wealth inequality: Evidence from population registers, » Journal of Public Economics, Vol. 165, pp. 17-30 / Cowell, F., D. Van De Gaer and C. He (2017), Inheritance Taxation: Redistribution and Predistribution / Akgun, O., B. Cournède and J. Fournier (2017), « The effects of the tax mix on inequality and growth,« OECD Economics Department Working Papers, No. 1447.

[12]Kleven H., C. Landais, M. Muñoz and S. Stantcheva (2020): « Taxation and Migration: Evidence and Policy Implications, » Journal of Economic Perspectives, vol. 34, no. 2, pp. 119-42.

[13]Brülhart and Parchet (2014) and Moretti et al. (2020).

[14]For Germany, Kindermann, Mayr, and Sachs (2020) estimate that for every €1 collected in inheritance tax, there is €0.09 in income tax revenue.

Kindermann, F., L. Mayr, and D. Sachs (2020), « Inheritance taxation and wealth effects on the labor supply of heirs, » Journal of Public Economics, pp. 104-127.

[15]Goupille-Lebret J. and J. Infante (2018): « Behavioral Responses to Inheritance Tax: Evidence from Notches in France, » Journal of Public Economics, No. 168, pp. 21-34.

[16]« Microsimulation models of household wealth taxes, » DG Trésor working paper, December 2021

[17]Bach L. (2009), « Are hereditary business transfers less effective? The case of France between 1997 and 2002, » Revue Économique, 60 (3), 787-796.

[18] Laurence Boone (2019), « France, inequality, and social mobility. »

Usefulness of the subject: This article aims to understand the role of inheritance and gifts in determining the distribution of wealth, to identify which French households are currently affected by inheritance and gift tax, to assess how France compares to other OECD countries in terms of inheritance and gift taxation, and to analyze several possible changes to the current tax system.