Purpose of the article: The purpose of this article is to show that, given the economic slowdown in the eurozone and the risks of secular stagnation, the scope for monetary policy is more limited than before and that only fiscal policy can take over.

Summary:

- The new European economic environment is characterized by weak economic growth, persistently low interest rates, and underemployment. These three factors are preventing inflation from rising to a level close to 2%, the target set by the European Central Bank (ECB).

- In addition, the IMF and the OECD have revised downwards their economic growth forecasts for the euro area in 2019 and 2020. Against this backdrop of economic slowdown, mainly due to external factors, some countries with economies that are more based on domestic demand are more resilient than others.

- The ECB’s capacity to counter this slowdown would be more limited than before, given the current debate on the « liquidity trap » situation. Consequently, the only option remaining is fiscal policy, which could in itself reinforce the effectiveness of monetary policy.

- Supported by economists and institutions (ECB, OECD, IMF), fiscal policy would be an effective lever to (1) counter this economic slowdown and (2) emerge from secular stagnation. However, there remain several obstacles of a political nature and relating to the evolution of fiscal rules.

1. The structural and cyclical challenges facing the eurozone economy could justify fiscal stimulus.

1.a) A new economic landscape: low interest rates and weak growth, underemployment, low inflation

Macroeconomic changes are widely discussed among economists, and new frontiers seem to have been crossed on many fronts. Three major trends can be identified: sustained low growth ( potential growth in the eurozone is estimated at 1.4% in 2018 according to the European Commission), persistently low or negative interest rates (Chart 1) and, finally, rising underemployment[1] despite low or falling unemployment (7.4% in August 2019 according to Eurostat). These three trends are not conducive to a rise in inflation (0.8% for headline inflation and 1.2% for core inflation[2] in September 2019 according to Eurostat) to the level targeted by the ECB. In this context, the measures taken by the monetary and fiscal authorities appear to be insufficiently coordinated in the eurozone.

With regard to public debt, the debate surrounding the unsustainability of government debt, supported by many economists after the 2008 crisis, seems to be waning: the snowball effect[3] that would penalize future generations. And despite the rise in public debt in advanced countries, interest rates are at historically low levels (at 10-year maturity on December 3 , France: 0%; Germany: -0.31%; Spain: 0.45%; Italy: 1.44%), implyinginterest costs that have never been so low for governments.

Chart 1: 10-year sovereign interest rates (in %)

Sources: Bloomberg, BSI Economics

The decline in long-term rates is the result of (1) a structural global savings glut, (2) a monetary policy that remains highly accommodative, and (3) a climate of slowing global growth andhigh risk aversion, translating into strong demand for risk-free assets (flight-to-quality phenomenon on sovereign bonds). As a result, Agence France Trésor is currently borrowing at negative rates up to a maturity of 10 years, and a large portion of German debt is trading below 0%.

Furthermore, with key interest rates at rock bottom (and even in negative territory for the deposit rate), the macroeconomic effectiveness of unconventional monetary policies may prove limited due to overuse.We note that since the launch of quantitative easing in 2015, the monetary base[4] has increased by 166% (from €1.2 trillion to €3.2 trillion), while at the same time the money supply (M3) has increased by only 20%. This leads to the conclusion that a significant portion of the €2 trillion in base money created by the Eurosystem is not being fully transmitted to the real economy. Consequently, it is unlikely that a further sharp increase in the balance sheet will significantly change this situation.

1.b) The economic slowdown in the eurozone: decline in the industrial sector but services are proving resilient

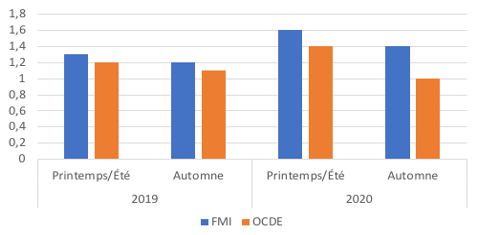

As shown by recent figures published by the OECD and the IMF, the eurozone economy is facing a slowdown. Both institutions revised their forecasts downwards this fall (-0.1 percentage points in 2019 and -0.4 percentage points in 2020 for the OECD and -0.1 percentage points in 2019 and -0.2 percentage points in 2020 for the IMF) for the eurozone (see Chart 2). The latest economic surveys continue to show a sharp slowdown in the manufacturing sector, particularly in Germany[6], but the services sector is proving more resilient. Thanks to its dynamic domestic demand, the French economy has become the engine of growth in the EMU.

Chart 2: Changes in GDP growth forecasts for the euro area (in %)

Sources: IMF, OECD, BSI Economics

An expansionary fiscal policy would therefore have two objectives: to cushion the economic slowdown and to strengthen potential growth by mobilizing existing savings and encouraging economic agents to invest. The question that arises is how much room for maneuver euro area governments have to fulfill their responsibilities in terms of stabilization and structural policies (public investment), given that public debt levels are already high.

2. Fiscal stimulus becomes relevant and is approved by the institutions despite the constraints imposed by EU fiscal rules

2.a) The call for fiscal stimulus: countercyclical policy and public investment stimulus to boost potential growth

More and more economists, such as Olivier Blanchard, but also supranational institutions, are emphasizing that fiscal leverage is becoming a necessity in the face of the risk of secular stagnation and /or economic slowdown.

For Olivier Blanchard, it is primarily the nominal interest rate being lower than the nominal growth rate (r<g) that is highlighted and is becoming the norm[9]. A positive gap between the growth rate and the interest rate would ensure the long-term sustainability of debt[10]. Consequently, at the level of the government’s financing costs, the cost/benefit balance of debt becomes positive and the economic situation facilitates an increase in the multiplier effect[11] of public spending[12].

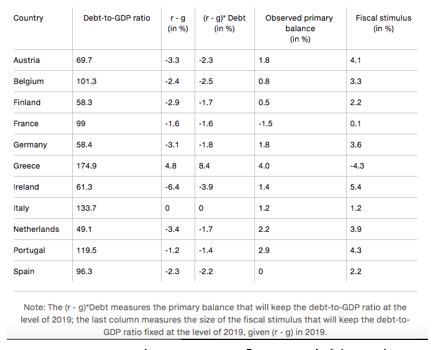

Applied to the eurozone, countries with an interest rate regime in which r > g (where r is the interest rate and g is the GDP growth rate) are therefore very limited in their use of fiscal policy (e.g., Italy and Greece). For the others (Germany, the Netherlands, Ireland, Finland, Austria and, to a lesser extent, France, Spain, Portugal, and Belgium), the debt-to-GDP ratio will tend to remain stable, meaning that even if the government finances all interest-related expenditure by issuing debt, the debt-to-GDP ratio will tend to decline.

This means that these countries have room for maneuver to use countercyclical fiscal policies to (1) counter the economic slowdown and (2) strengthen potential growth through public investment without threatening the sustainability of their public debt.

Table 1: Fiscal stimulus room for maneuver in selected euro area countries in 2019

Source: Paul De Grauwe & Yuemei Ji (2019)

The call for fiscal stimulus is also reinforced by international organizations such as the OECD, the IMF, and the ECB, which justify this stimulus as a means of cushioning the economic slowdown. In its latest publication on the interim economic outlook for September 2019, the OECD points out that several eurozone countries (Germany, the Netherlands, Austria, and the Baltic states) have fiscal capacity and that using this capacity would strengthen the medium- and long-term economic growth of the EMU. A few days earlier, at the Governing Council press conference, Mario Draghi, then President of the ECB, called on countries with budget surpluses to « act effectively and quickly » in view of the deteriorating economic outlook in the euro area. Furthermore, at his last press conference on October 24, he mentioned that the effectiveness of monetary policy (in order to bring inflation down to a level below but close to 2%) now depended on the use of fiscal policy. Finally, the IMF encouraged Germany in particular to take action through the publication of Article IV in July 2019.

2.b) But the countries concerned remain reluctant to provide any fiscal support despite the pressure that is beginning to weigh on them

Recent macroeconomic developments have not changed the minds of Member States, which remain reluctant to provide any form of demand support despite interest rates and the economic slowdown in the euro area. De facto, while (1) the cost of debt is falling sharply (demand for sovereign bonds is strong, leading to lower yields), (2) there is a lack of domestic demand and public investment has been insufficient since the 2008 crisis, thereby penalizing potential growth, some eurozone members are refusing to use fiscal leverage.

Pressure on economies with room for maneuver is mounting, not only from institutions but also from financial markets, especially as the risk of economic recession in Germany, with its manufacturing sector in sharp decline, should encourage a coordinated European recovery.

In this context, German Economy Minister O. Scholtz is attempting to change German economic policy, now advocating a « solid budget » rather than a « zero deficit »(schwarze Null), while the Netherlands is considering creating a €50 billion public investment fund financed by debt to develop certain sectors that are sorely lacking in capital. Finland recently joined the ECB’s call and is preparing to invest in its infrastructure to boost short- and long-term growth. This long-awaited fiscal stimulus is therefore both a necessity, given the state of the economy, and an opportunity, given the level of interest rates.

2.c) And fiscal rules may compel eurozone countries to use fiscal policy

The shortcomings of fiscal rules and the incompleteness of the eurozone are well known: the rules require countries to reduce their structural public deficits to 0.5% of GDP and gradually reduce their public debt to around 60% of GDP, with a public deficit of 3% of GDP to be respected.

The pro-cyclical nature of these rules is often criticized: when GDP contracts, countries tighten fiscal policy, which exacerbates the recession and effectively increases the public debt ratio.

However, many economists are calling for these rules to be simplified and relaxed to enable countries to better support economic activity in the face of asymmetric shocks. A group of 14 French and German economists[19] has put forward its proposals for achieving this. In particular, they propose replacing the current budgetary rules, which focus on the so-called « structural » deficit, with a simple spending rule with a long-term debt reduction target.

The idea of the cost/benefit advantage of increasing public debt is ultimately gaining more and more consensus, but we now need to consider how this new debt will be used (some ideas on this will be posted shortly on the BSI website in a new article).

Conclusion

This new macroeconomic environment, combined with an economic slowdown in the eurozone, reinforces the need to use fiscal leverage to increase potential growth and better prepare for future shocks. It now depends on the political will of countries with fiscal capacity to activate this leverage.

(article completed on December 3, 2019)

[1]Blanchard, O., & Summers, L. H. (2019). Evolution Or Revolution: Rethinking Macroeconomics After the Great Recession. Mit Press.

[2] Inflation excluding volatile components (oil, fresh produce, meat, etc.).

[3] The debt snowball effect refers to the autonomous process of worsening public deficits resulting from a gap between economic growth and the cost of public debt (associated with a given level of interest rates).

[4] The monetary base refers to both banknotes and coins in circulation and monetary assets held by banks at the central bank.

[5] De Grauwe, P., & Ji, Y. (2019). Time to change budgetary priorities in the eurozone. Intereconomics, 54(5), 285-290.

[7] Secular stagnation generally refers to a situation where an economy is faced with a combination of low growth and low inflation in a context of low interest rates.

[8] Le Floc’h, P (2016). What are the risks of secular stagnation for the eurozone? BSI Economics Studies. November

[9]Blanchard, O. (2019). Public debt and low interest rates. American Economic Review, 109(4), 1197-1229.

[10]Aurissergues E. (2019). The rise in public debt: should we be happy about it? , BSI Economics, March

[11]Auerbach, A. J., & Gorodnichenko, Y. (2012). Measuring the output responses to fiscal policy. American Economic Journal: Economic Policy, 4(2), 1-27.

[12]Ramey, V. A. (2019). Ten years after the financial crisis: What have we learned from the renaissance in fiscal research?. Journal of Economic Perspectives, 33(2), 89-114.

[13]Heyer, E., & Timbeau, X. (2019). What room for maneuver is there for French public finances in a world of persistently low interest rates?, OFCE, Le Blog, October 16

[14]OECD (2019), Interim Economic Outlook, September

[15]Draghi M. (2019). Introductory statement to the press conference (with Q&A), October 24.

[17]Bénassy-Quéré, A., Ragot, X., & Wolff, G. (2016). What kind of fiscal union for the eurozone? Notes from the Economic Analysis Council, (2), 1-12.

[18] That is, the public deficit adjusted for the economic cycle.

[19]Telos-eu (2018). Reconciling solidarity and market discipline in the eurozone.

[20]Furman, J. (2016). The new view of fiscal policy and its application. VoxEU.org.