Usefulness: This article identifies the determinants of economic cycle synchronization in ECOWAS. It is relevant in light of the region’s heads of state’s desire to create a single currency in 2020. Indeed, taking steps to synchronize cycles is important because the asymmetries of shocks observed within a monetary union determine its sustainability.

Summary:

- A monetary union requires member countries to relinquish their monetary sovereignty, at least partially. Monetary policy ceases to be national and becomes common to all countries in the union in question.

- The synchronization of economic cycles has the advantage of increasing the effectiveness of monetary policy because when countries are not in the same phase of the cycle (some in expansion and others in recession), the common monetary policy may prove more favorable to some countries than others.

- Thus, identifying the factors that synchronize cycles allows policymakers to better target their economic policies. For example, the effects of trade liberalization make it possible to verify the relevance of free trade agreements in terms of economic convergence.

- Trade integration and financial integration are determinants of economic cycle synchronization in ECOWAS (Economic Community of West African States). In addition, sharing a common currency in ECOWAS will increase economic cycle synchronization through trade.

- The weakness of intra-community trade in the region is not an obstacle to monetary union, as trade outside ECOWAS also increases the synchronization of economic cycles.

The single currency of ECOWAS, to be called the » Eco, » has been a recurring topic of discussion for 45 years. Since its creation in 1975, ECOWAS (Economic Community of West African States) has sought to promote greater integration in all areas of economic activity, including trade, industry, energy, telecommunications, and monetary and financial issues (Ouédraogo, 2003).

However, plans to establish the « Eco » have been postponed numerous times (see Appendix at the end of the article). These constant postponements raise concerns about the ability of West African economies to comply with the same rules and about the consequences, both positive and negative, that this monetary change could entail. While monetary union limits the uncertainties associated with exchange rate fluctuations, increases foreign direct investment, reduces transaction costs, and boosts intra-community trade, it also imposes constraints.

The national cost of participating in a monetary union stems mainly from the renunciation of a specific monetary policy and the loss of the exchange rate as an instrument for adjusting to external shocks. This disadvantage reflects the impossibility of using the exchange rate as an economic policy instrument in the face of a shock that triggers asymmetric responses from one region to another. The viability of the union depends on its ability to mitigate these so-called asymmetric shocks, because in the face of such shocks, the common monetary policy may prove more favorable to some countries than others.

The asymmetry of economic cycles forms the basis of the traditional theory of optimal currency areas (OCAs) developed by Mundell (1961), McKinnon (1963), and Kenen (1969). For a monetary union to be economically viable and advantageous, the countries forming the monetary union must be in the same phase of the economic cycle at the same time (cycle synchronization). This condition of symmetry, considered a necessary condition for the success of monetary unions, ensures that the common monetary policy can be stabilizing in all countries and that in no country does the abandonment of monetary sovereignty mean increased cyclical instability.

Thus, the degree of asymmetry in economic cycles observed within a monetary union determines its sustainability. In this article, we identify potential determinants of economic cycle synchronization in ECOWAS to enable economic policymakers to better orient their economic policies in order to contribute to increasing cycle synchronization in the region.

1. Heterogeneity of ECOWAS economies

Many factors contribute to increasing the asymmetry of economic cycles in ECOWAS.

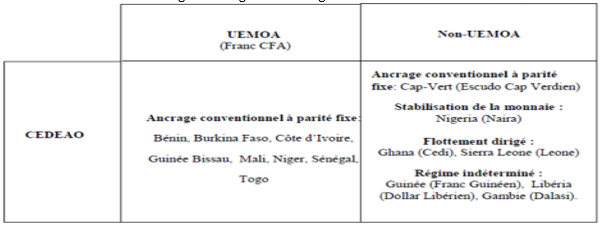

On the monetary front, ECOWAS includes, on the one hand, the countries of the West African Economic and Monetary Union (UEMOA) and Cape Verde, whose currencies have been pegged to the euro since 1999 (and previously to the French franc), and, on the other hand, the English-speaking countries of West Africa and Guinea, which have independent currencies. Furthermore, Nigeria, as a full member of ECOWAS, has a much larger economy than any other member. It alone accounts for 65% of the region’s gross domestic product (GDP) (World Bank, 2018). Also, unlike most other countries in the region, Nigeria’s economy is heavily dependent on crude oil exports (Economic Complexity Observatory, 2018).

Thus, when oil prices are high, Nigeria can experience strong economic expansion, which may justify a restrictive monetary policy (e.g., higher interest rates), while its crude oil-importing neighbors such as Côte d’Ivoire, Senegal, and Togo may suffer from weaker growth or recession, requiring a more accommodative monetary policy (e.g., lower interest rates). In addition, the region’s countries’ specialization in raw material exports creates structural vulnerability linked to significant volatility in the terms of trade( Bénassy-Quéré and Coupet, 2005).

Figure 1: Exchange rate regime in ECOWAS

Sources: Bationo (2018), BSI Economics.

Note: (.), national currency. The ZMAO represents the non-UEMOA zone with the exception of Cape Verde.

From the above, it is clear that the economies of the ECOWAS are heterogeneous and that the homogeneous impact of a single monetary policy would be hypothetical.

2. Ex-ante to ex-post conditions for an optimal currency area (OCA)

Early studies on the optimality of currency areas identified criteria that must be met in order to abandon the use of exchange rates as an adjustment instrument at low cost. These are traditional criteria such as the mobility of production factors (Mundell, 1961), the degree of openness of economies (McKinnon, 1963), and the degree of diversification (Kenen, 1969). According to these criteria, countries that each have factor mobility, a high degree of economic openness (measured by trade) and a diversified productive structure can form a monetary zone. However, the direct application of these criteria does not clearly identify the optimal profile of an EMZ (Beine, 2002).

This difficulty arose in the context of the European EMU and prompted many authors to resort to an implicit but central criterion in EMU theory. This is the degree of asymmetry of cycles. The idea is to analyze the extent to which countries applying for monetary union have similar economic cycles, since the exchange rate is primarily seen as an instrument for cushioning the effect of significant macroeconomic fluctuations. In this sense, most academic studies on the subject show that the divergence of economic cycles is so marked between West African countries that the ECOWAS countries could not form an EMU (Bénassy-Quéré and Coupet, 2005; Houssa, 2008; Tsangarides and Qureshi, 2008).

However, these analyses are static because they cannot be assessed over several periods. This poses a problem because a monetary union that is considered costly from the outset may become beneficial over time. As proof, since the 1990s, the literature has seen the emergence of the endogenous theory of EMAs, which states that the creation of a monetary union between a group of countries establishes conditions for increased trade and, at the same time, brings the cycles of these countries closer together.

Frankel and Rose (1998) assume that in a monetary union, intra-industry specialization tends to develop with the expansion of bilateral trade, and as a result, the productive structures of countries become more similar. Thus, countries would be affected in the same way by sectoral shocks. This thesis is supported by the experience of the euro. A country such as Spain, which had very different fluctuations from other member countries before joining the euro area, has seen its economic cycle become significantly and positively correlated with other economic cycles in the euro area (Gravet, 2014).

Thus, the absence of the ideal ex-ante conditions described in early studies does not preclude the ex-post success of a monetary union, provided that there is a gradual synchronization of economic cycles based in particular on deeper intra-industry trade[2]. Even if intra-industry trade may be relatively weak initially, the trade dynamics driven by monetary union are capable of initiating a significant increase in this type of trade and thus increasing the synchronization of economic cycles.

Identifying the determinants of cycle synchronization in ECOWAS is essential for the ex-post success of the future monetary zone.

3. Determinants of economic cycle synchronization in ECOWAS

Trade integration and financial integration are two key aspects of economic cycle synchronization in ECOWAS. These two factors deserve special attention. The first allows us to verify the endogeneity hypothesis[3] for the region (Frankel and Rose, 1998). In other words, a monetary union creates ex post the conditions for its optimality. The second is relevant in view of its role in the risk-sharing mechanism (a mechanism for smoothing asymmetric shocks).

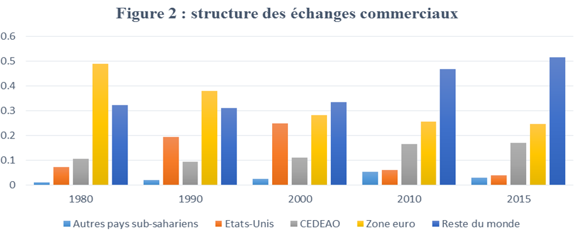

A) Trade

According to Figure 2, intra-regional trade is relatively limited in the ECOWAS region. This weakness certainly limits the potential gains of a monetary union. However, monetary unification in itself tends to increase the volume of trade, as observed in the WAEMU (Diop, 2007). Indeed, the sharing of the CFA franc in the WAEMU has increased intra-community trade by reducing transaction costs.

Sources: Direction of Trade Statistics (DOTS) from the International Monetary Fund (IMF), BSI Economics.

Note: trade = (Xij,t + Mij,t) / (Xi,t+Xj,t).Mij,t represents imports from country j to country i, andXij,t represents exports from country i to country j.Xit andMjt indicate, respectively, total exports from country i to the rest of the world and total imports from the rest of the world to country j.

Intra-ECOWAS trade over the period 1980-2015 accounted for 9% (lowest level) of total ECOWAS trade in 1990, compared with 17% (highest level) in 2015. Our econometric estimates (Zouri, 2020) for the period 1980-2015 show that bilateral trade within ECOWAS helps to increase the synchronization of economic cycles in the region.

ECOWAS trade with the eurozone accounted for 25% of total ECOWAS trade in 2015, compared to 49% in 1980. Although the eurozone’s share of total ECOWAS trade has declined over the years, it remains its main trading partner.

The weakness of intra-regional trade compared to trade between ECOWAS countries and the euro area can be explained in part by the export and import products of the region’s member countries. By analyzing the impact of bilateral trade between the countries of the region and the euro area on the synchronization of economic cycles in ECOWAS, econometric estimates (Zouri, 2020) show that the trade structure of ECOWAS countries is not an obstacle to monetary union, as trade between ECOWAS countries and the euro area also accentuates the synchronization of economic cycles within the countries of the region.

The positive effect of trade between ECOWAS and the eurozone on the synchronization of economic cycles can be explained by the interdependence of the economies. Take, for example, an economic shock (a sudden event that causes an economic indicator to rise or fall) affecting the eurozone, such as the 2008 financial crisis. This shock will lead to a decline in eurozone demand for raw materials exported by ECOWAS countries. This decline in demand will lead to a decline in exports in each ECOWAS country. The end result will be a decline in GDP in all countries in the region. Thus, due to their trade interdependence, a demand shock in the eurozone will have the same effect on the economic activity of ECOWAS countries. This is why the literature identifies common factors (changes in commodity prices, changes in reference interest rates in developed economies) as determinants of the synchronization of economic cycles (Chebbi and Knani, 2013; Duarte and Holden, 2003).

Finally, when comparing the trade integration of WAEMU countries with non-WAEMU countries, our econometric estimates (Zouri, 2019) show that the monetary union has increased trade within the WAEMU by reducing transaction costs.

B) Financial integration

Compared to developed countries, international financial integration in ECOWAS is weak (Dufréno and Sugimoto, 2019). There are two reasons for this weakness. First, the level of development of financial markets is still low. This delays financial integration due to the inferior performance of commercial banks and financial companies (Lensik and Meesters, 2014). Second, financial markets are still fragmented because banks and financial institutions operate in oligopolistic markets. This does not facilitate access to credit (Beck and Honohan, 2008).

International (and especially regional) financial integration deserves special attention in ECOWAS because it can help supplement domestic savings that are sometimes insufficient or poorly mobilized, improve the allocation of financing for productive, high-yield investments, contribute to increasing access to financial services, particularly credit, enable the absorption of asymmetric exogenous shocks, and encourage more effective macroeconomic stabilization policies (Agénor, 2014).

In addition, strengthening financial links could increase the synchronization of economic cycles. Kose et al. (2003) indicate that financial integration leads to a higher degree of synchronization of economic cycles by generating significant demand-side effects. Indeed, if consumers in ECOWAS countries hold a significant portion of their investments in a particular stock market in the region, then a crisis in that stock market could lead to a simultaneous decline[5] in demand for consumer and investment goods (ultimately leading to a decline in GDP) in the various countries of the region.

Our econometric estimates (Zouri, 2020) for the period from 1980 to 2015 show that both de facto (Lane and Milesi-Ferretti, 2003) and de jure (Chinn-Ito index, 2006) international financial integration increase the synchronization of economic cycles in the region. Furthermore, by constructing a proxy for regional financial integration based on risk-sharing theory (Alcalin et al., 2015), we show that regional financial integration has a greater impact on the synchronization of economic cycles in the region than international financial integration.

Conclusion

Trade integration and international financial integration (de facto or de jure) appear to be key determinants of economic cycle synchronization in ECOWAS. However, we indicate that regional financial integration dominates international financial integration. The weakness of intra-community trade would not be an obstacle to monetary union, as trade between ECOWAS countries and the euro zone also increases the synchronization of economic cycles. However, a single currency in ECOWAS would increase the synchronization of economic cycles through trade. Several implications for the region arise from these results.

The coexistence of several currencies and exchange rate regimes in a small area such as ECOWAS does not promote trade between countries given the high transaction costs. Therefore, a common currency means savings for each member country on all commercial and financial transactions with other members of the Union. However, these savings on transaction costs are not without consequences, as there will be a single common monetary policy for all countries in the region. The difficulty in finding the optimal formula for conducting a common monetary policy in a monetary union stems from the asymmetric nature of economic cycles. However, the asymmetry of economic cycles between ECOWAS countries should not block the political decision to expand the monetary union, as this promotes the synchronization of economic cycles through trade. In addition, economic policymakers must promote financial integration in ECOWAS, particularly at the regional level, in order to further contribute to the convergence of economic cycles and better risk sharing in the region.

Appendix: Major historical milestones in the development of the « eco »

This desire was marked in 1996 with the creation of the West African Monetary Agency (WAMA), whose mission is to oversee the design and operational implementation of this project. This outline was reinforced in 1999 with the adoption of a so-called integrated strategy. This strategy provided that countries not members of the West African Economic and Monetary Union (WAEMU) should create a single monetary zone called the West African Monetary Zone (WAMZ), which would subsequently merge with the WAEMU zone to form the single currency of ECOWAS.

Since then, despite the support provided by subregional institutions, the WMAZ project has not made any significant progress. An initial deadline was set for 2003, then postponed to 2005 and 2009. Faced with this lack of progress, and given that the advent of the ECOWAS single currency zone is contingent upon the establishment of the WAMZ, ECOWAS urged WAEMU countries in 2013 to take the necessary steps to roll out their project before the end of 2015, by which time the WAEMU should have a single currency in the same way as the WAEMU zone.However, given the WAMZ’s inability to adopt a single currency, ECOWAS decided in 2015 to abandon the two-speed approach and merge the region’s currencies in 2020.

Notes and Bibliography

- Acalin, J., Cabrillac, B., Dufrénot G., et al. 2015. Financial integration and growth correlation in Sub-Saharan Africa. Banque de France.

- Agénor, P.R. 2014. Successful financial integration in Africa. At a conference organized by the Banque de France and FERDI

- Bationo, B.F. 2018. Monetary and exchange rate policies—The CFA franc, an optimal choice for the West African Monetary Union, L’Harmathan, African Studies collection.

- Beck, T. & Honohan, P. 2008. Finance for all? Policies and pitfalls in expanding access. World Bank Publications, Washington D.C.

- Beine, M. 2002. The European Monetary Union: Lessons from the Optimal Currency Area Approach. De Boeck Supérieur, European Economic Integration, 139-158.

- Bénassy-Quéré, A. & Coupet, M. 2005. On the adequacy of monetary arrangements in Sub-Saharan Africa. The World Economy, 28(3), 349-373.

- Chebbi, A. & Knani, R. 2013. Determinants of cycle synchronization in Tunisia: an ADL model approach. Revue d’Economie Théorique et Appliquée, 3(1), 23–48.

- Duarte, A. & Holden, K. 2003. The business cycle in the G-7 economies. International Journal of Forecasting, 19(4), 685–700.

- Dufrénot, G. & Sugimoto, K., 2019. Does international financial integration increase the standard of living in Africa? A frontier approach. Working Papers halshs, HAL.

- Frankel, J. A. & Rose, A. K. 1998. The Endogeneity of the Optimum Currency Area Criteria. Economic Journal, 108 (449), 1009-1025.

- Gravet, I. 2014. Eurozone and productive specialization. Resources in economics and social sciences, Ecole Normale Supérieure de Lyon.

- Houssa, R. 2008. Monetary union in West Africa and asymmetric shocks: a dynamic structural factor model approach. Journal of Development Economics, 85(1-2), 319–347.

- Kose, M. A., Otrok, C., & Whiteman, C. H. 2003. International Business Cycles: World, Region, and Country-Specific Factors. American Economic Review 93 (4), 1216–1239.

- Kenen, P. 1969. The Theory of Optimum Currency Areas: an Eclectic view. Monetary Problems of the International Economy, R. Mundell and K. Swoboda, University of Chicago Press.

- Lensik, R. & Meesters, A. 2014. Institutions and bank performance: a stochastic frontier analysis. Oxford Bulletin of Economics and Statistics, 76(1), 67–92.

- McKinnon, R. 1963. Money and Capital in Economic Development. Washington, DC: Brookings Institution.

- Mundell, R. A. 1961. A Theory of Optimal Currency Areas. American Economic Review, 51 (4), 667-665.

- Ouédraogo, O. 2003. A single currency for all of West Africa? Karthala, economics and development collection.

- Tapsoba, S. J-A. 2009. Heterogeneity of shocks and the viability of monetary unions in West Africa. Revue Economique et Monétaire, (5), 38-63.

- ZOURI, S. 2020. Business cycles, bilateral trade and financial integration: Evidence from Economic Community of West African States (ECOWAS). https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3541770

[1]Terms of trade refer to the purchasing power of imported goods and services that a country has thanks to its exports.

[2]Trade in goods or services involving the same types of products or services (e.g., France buys German cars and Germany buys French cars).

[3]The creation of a monetary union between a group of countries establishes conditions for increased trade and, at the same time, brings the economic cycles of these countries closer together.

[4]The countries in the region are rich in natural resources but lack the technology needed to process raw materials. As a result, most of their exports consist of raw materials destined for industrialized countries. Their imports consist of consumer goods and equipment from industrialized countries.

[5]As a reminder, synchronization occurs when countries react in the same way (decline or increase) to a shock, whether positive or negative.