Usefulness of the article : This note sheds light on negative interest rates and the extent to which they are justified, highlighting their limitations and, more specifically, their impact on the stability of the European banking system. The article also outlines a solution that the ECB could consider in order to support banks facing negative rates.

Summary :

- The fall in the deposit rate into negative territory has made it possible to continue monetary accommodation while key interest rates were close to 0%;

- Negative rates are limited by: 1) a physical lower bound, below which agents prefer to hold cash rather than an asset with a negative return, and 2) an economic lower bound, below which rate cuts would have counterproductive effects on the economy, in particular because they would threaten the stability of the banking system.

- In addition to the direct cost to banks’ profitability of applying negative deposit rates to excess reserves, negative rates reduce the interest margin of banks, which struggle to pass them on to their customers’ deposits. They also push banks to take more risks.

- While the European Central Bank is considering further rate cuts in 2019, it could at the same time decide to introduce a tiered system for remunerating excess reserves in order to exempt part of them from the negative deposit rate and thus support banks’ profitability.

On August 20, 2019, Germany and France borrowed at the lowest 10-year rates in their history, at -0.7% and -0.4% respectively. That same month, a Danish bank announced that it would offer its customers 10-year mortgages at a negative interest rate. After a decade of ultra-accommodative monetary policy, and more specifically five years after the European Central Bank (ECB) lowered its deposit rate into negative territory, negative interest rates have become the norm in Europe. Although justified in some respects, this new environment has side effects that could hinder the transmission of monetary policy to the economy, particularly through the banking channel.

Reminder of the principles of monetary policy transmission to short- and long-term rates

The ECB stimulates or restricts economic activity by manipulating key interest rates, which enable it to set short-term interest rates. The ECB has three key interest rates at its disposal to implement monetary policy:

- The refinancing rate is the rate at which the central bank lends funds for a period of one week against collateral provided as security. The refinancing rate has been 0% since March 2016.

- The overnightdeposit rate, which remunerates cash deposited in commercial banks’ accounts with the central bank. The deposit rate for excess reserves is currently -0.4%.

- The marginal refinancing rate, which allows banks to borrow central liquidity on an emergency basis for one day. Currently stable at 0.25%, it is still higher than the refinancing rate.

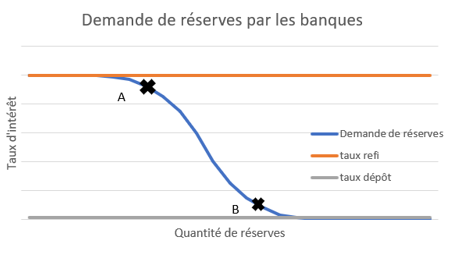

The interbank market rate, which is determined by the supply and demand for short-term bank liquidity, is automatically between the deposit rate (lower limit) and the refinancing rate (upper limit). Below this rate, the lending bank will prefer to deposit its liquidity in its account with the ECB rather than lend it on the short-term market, while above this rate, the borrowing bank will choose to borrow directly from the ECB rather than on the market. It is through this mechanism that the ECB manipulates short-term market rates via its key interest rates. For several reasons, the ECB has injected a very large amount of liquidity into the system since 2008. The abundance of liquidity has caused demand for this liquidity to fall, leading to a decline in interbank rates, which have converged towards the deposit rate. The deposit rate has since become the ECB’s benchmark policy rate.

Figure 1 – Demand for liquidity by banks, BSI Economics

Interest rates on longer-term securities are set by the market according to the law of supply and demand and are, in theory, equal to the average of the short-term rates anticipated by investors, to which a term premium must be added (see the article « Expectation hypothesis: what is it? » by BSI Economics). By changing key interest rates, the ECB therefore indirectly affects longer-term rates as it changes investors’ expectations. Lower long-term rates reduce borrowing costs for households and businesses, making it easier for them to take on debt for consumption and investment, thereby stimulating the economy and inflation.

Since the crises of 2008 and 2010, the ECB has also expanded its toolkit by using unconventional policies to influence long-term rates: 1) it guides investor expectations (« forward guidance ») by providing indications on the future level of key interest rates, and 2) between March 2015 and December 2018, it purchased large quantities of long-term debt securities, contributing in particular to increasing their price and thus reducing their yield.

Why did the European Central Bank lower its deposit rate into negative territory?

To understand the ECB’s decision to use negative key interest rates, it is necessary to address the concept of the neutral rate. The neutral rate is the theoretical key interest rate (its estimation is often subject to debate) that stabilizes unemployment and inflation in an economy. A central bank’s monetary policy is considered accommodative when it sets its key rates below the estimated neutral rate, which will stimulate growth, and restrictive when they are set above it, which will slow growth.

This neutral rate is not fixed over time; it evolves in the long term according to factors that affect structural growth, such as demographics and technological progress. It can also vary temporarily in response to temporary events that affect the economy, such as a crisis or fiscal stimulus, without affecting long-term growth. The economic collapse that followed the 2008 financial crisis and then the sovereign debt crisis in the eurozone caused the neutral rate to fall below 0% after 2013, according to estimates by Laubach & Williams (2016). Given the ECB’s desire to continue monetary accommodation in a context of low inflation and below-potential growth, the introduction of a negative deposit rate from June 11, 2014, appears more consistent.

Another factor also influenced the ECB’s decision. Once key rates reached the psychological floor of 0% (which investors did not consider breakable), the transmission of short-term key rates to longer-term rates became imperfect. Investors could only anticipate that rates would remain at their current level or rise in the future, which artificially kept long-term rates higher. According to ECB President Mario Draghi, breaking the 0% threshold helped to lower investor expectations.

Negative rates are causing concerns about the stability of the banking system

In a speech in July 2016, Benoît Coeuré, member of the ECB’s Executive Board, explained that rates can fall below 0% as long as they do not exceed two limits: the « physical lower bound » and the « economic lower bound. »

The physical lower bound is the threshold below which agents prefer to convert their liquid assets into cash rather than hold an asset with a negative return. Of course, holding cash has a cost for the owner, who must store their money, insure it, and use it for day-to-day transactions. This cost is not linear for all agents. For example, compared to an individual, a large company carries out more transactions but would benefit from economies of scale related to cash storage. The physical limit below which it is preferable to convert bank deposits into cash is different for everyone. Thus, this risk could materialize gradually as rates fall. The transition to negative rates has so far been smooth, with banks not facing an increase in withdrawal requests.

The economic threshold is of particular interest to us in this article. This is the level at which further cuts in key interest rates would have counterproductive effects on the economy. Under normal circumstances, a cut in key interest rates supports the economy and therefore banks’ lending activity (more loan applications, fewer defaults among borrowers with the same repayment capacity as interest charges are lower, etc.), which improves their earnings prospects. However, the banking sector’s profitability falls when key interest rates drop below a certain level. Bank profitability is essential for banks to accumulate capital (also known as « equity »), which serves as a safety cushion when they incur losses (e.g., when a borrower defaults on a loan). When a bank has exhausted this safety cushion and no longer complies with regulatory requirements, it risks insolvency and must rebuild its capital. Financial stability is therefore directly threatened when the banking system as a whole lacks capital. In order to avoid the risk of insolvency, studies show that banks that do not have sufficient capital tend to restrict their lending activity, which is the opposite of what the central bank is seeking to achieve when it lowers its key interest rates. The strengthening of regulatory capital requirements imposed on banks by Basel III regulations accentuates this phenomenon.

As we will see in the next section, the impact of negative rates on bank profitability affects several areas of the balance sheet, making this threshold specific to each bank. Although this threshold has not yet been reached in aggregate terms, central bankers should be particularly vigilant in the event of further rate cuts.

What do banks object to about negative interest rates?

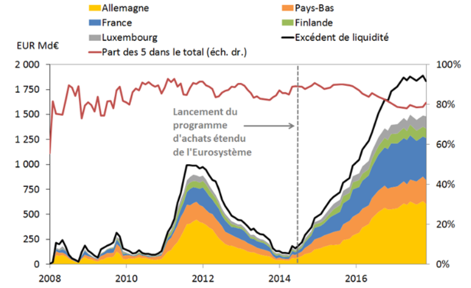

To meet their liquidity needs (flight of deposits to other banks, cash withdrawals by customers, granting of new loans to gain market share, repayment of maturing debt, etc.), banks use the reserves they deposit directly in their accounts with the ECB. To ensure that banks always have sufficient liquidity, the ECB requires them to hold a minimum amount of reserves equivalent to approximately 1% of the deposits they have collected (liquidity constraints have also been tightened by Basel III with the introduction of a liquidity coverage ratio). Above the mandatory threshold, banks are subject to a deposit rate on their reserves (currently -0.4% since March 2016, a rate that could be lowered in 2019 by 0.1 to 0.2 percentage points). For reasons that we will not explain in this article, the amount of excess reserves in the banking system has « exploded » with the start of the asset purchase program (« Quantitative Easing ») initiated by the ECB in 2015, without commercial banks being the source.

Figure 2 – Excess reserves in the eurozone, Banque de France, BSI Economics

The first criticism of negative rates is the direct cost to banks of applying the negative deposit rate to excess reserves. In 2018, eurozone banks paid €7.5 billion to the ECB, representing nearly 10% of their profits. It should be noted that reserves are distributed very unevenly among eurozone banks. German and French banks have paid 33% and 24% of the total bill to the ECB since the introduction of the negative deposit rate in June 2014.

Furthermore, negative rates indirectly weigh on the profitability of the banking sector by affecting banks’ various sources of income. The main activity of a commercial bank is to collect short-term funds (deposits and short-term loans on the money markets) and lend them on longer terms to businesses, governments and households (in the form of loans or by purchasing bonds), while assuming the risk of non-repayment of the loans it grants. To understand the impact of negative interest rates on banking activity, it is important to remember the factors that contribute to the sector’s profitability:

- The « maturity transformation margin, » which depends on the difference in profitability between the assets from which the bank derives its income (loans and long-term bonds) and the cost of its financing (deposits and short-term market borrowings), at equivalent risk;

- The « intermediation margin, » which arises from the transfer of risk from the depositor/lender to the bank;

- Changes in the price of its assets (i.e., loans granted and bonds acquired), which are inversely correlated with changes in interest rates;

- The economic climate. When the economy slows down, banks face an increase in customer defaults and lower demand for new loans.

Another major criticism of negative rates is that banks find it difficult to apply them to their customers’ deposits, particularly those of retail customers. In theory, if a fall in rates leads to a decline in short-term rates (on which the rate of return on customer deposits depends) and long-term rates (on which bank lending rates depend) in the same proportions, then banks see their « maturity transformation margin » unchanged. In practice, however, banks find it very difficult to pass on negative rates to customer deposits for several reasons: national law prohibits it, there is a high reputational risk for the bank, some customers could convert their deposits into banknotes, creating a risk of illiquidity, etc. The decline in income from bank lending is therefore only partially offset by a decline in their financing costs, which would reduce their profitability. In addition, banks show different sensitivities to negative rates depending on their financing structure. In particular, banks that are more dependent on customer deposits are more penalized than those that prefer to finance themselves on the money markets.

Athird criticism that is often raised is the counterpart to an effect that the ECB was actually seeking when it decided to implement its negative interest rate policy. In a context of abundant reserves, the negative rate that remunerates banks’ deposits with the ECB stimulates credit through an additional channel. Banks want to keep only the necessary reserves, as excess reserves penalize their profitability. Commercial banks can individually attempt to reduce their reserves by replacing them with other assets. To do so, they have three options:

- Granting a loan to a business, household, or the government

- Acquiring debt securities (public or private) or other assets

- Not renewing a debt that is coming to maturity

Negative interest rates therefore increase competition between banks and allow for an increase in the supply of credit. The downside of this effect is that it encourages banks to take more risks. In their « search for yield, » banks accept higher risk without being compensated proportionally, contributing to financial instability. This phenomenon has been confirmed empirically, with the decline in risk aversion leading to a decline in sovereign spreads (the yield differences for a given maturity between a country’s debt and that of Germany, which is the least risky). The question now is whether the risk taken by banks is too great and whether it is time to restrict it.

However, it should be noted that the ECB’s negative interest rate policy has also had positive effects on bank profitability:

- The downward movement in interest rates has had a positive impact on the value of the assets held in banks’ portfolios (loans and bonds), whose valuation is inversely correlated with interest rate movements.

- The continuation of an ultra-accommodative policy in recent years has supported the economy and, by extension, the banks. A favorable macroeconomic environment stimulates demand for credit and limits borrower defaults. This phenomenon is further reinforced by the fact that low rates make demand more solvent (the total amount to be repaid by the borrower is lower) and make it more attractive for businesses and households wishing to finance an investment to take out credit.

What options are available to the ECB as it considers further cuts to its deposit rate?

In 2017, Mario Draghi concluded that « overall, negative interest rates have been a success […] We have not seen the distortions that people predicted. We have not seen bank profitability decline; in fact, it has even increased… » Although he had long stated that negative rates were not an obstacle to financial stability and that, as a result, the ECB was not considering any solution to support bank profitability, Mario Draghi announced at the end of July 2019 that the ECB was examining the possibility of introducing a « tiering » system in the near future.

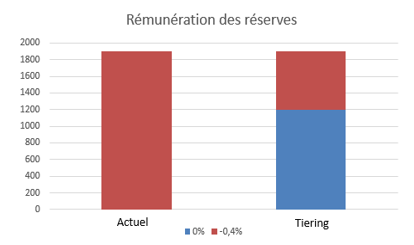

In order to alleviate the burden of negative rates, some central banks, such as the Bank of Japan, have introduced a system of tiered remuneration for banks’ reserves deposited with the central bank. Under such a system, the ECB could decide to exempt excess reserves up to a certain amount from negative rates, applying the deposit rate only marginally to reserves exceeding this threshold. It is even possible to imagine a multi-tiered remuneration system, as is the case in Japan (three tiers). French and German banks, which together hold €1.1 trillion of the €1.9 trillion in reserves deposited with the ECB, would be the primary beneficiaries of this system.

Figure 3 – Remuneration of excess reserves with and without tiering (€bn), ECB, BSI Economics

Tiering has been under discussion since the introduction of negative rates, as it allows the economic limit of negative rates to be pushed back. Its implementation opens the door to further cuts in key interest rates by the ECB, following the example of the Swiss central bank, whose main key interest rate is -0.75%. However, its detractors argue that tiering could partially offset the economic effects of a cut in key interest rates and even contribute to a rise in short-term rates, depending on the amount of reserves that the ECB decides to exempt.

Conclusion

Although justified by weak growth and inflation, the unconventional negative interest rate policy initiated by the ECB in 2014 could weigh on financial stability. A prolonged period of negative rates will erode banks’ profits, preventing them from accumulating capital, which acts as a safety cushion when they incur losses. While negative rates put pressure on bank lending rates, banks are reluctant to pass on this decline in returns to their customers’ deposits for legal and reputational reasons. Banks are therefore encouraged to seek higher returns, which they obtain in particular by granting more loans and accepting higher risk. While bank profitability has tended to improve in recent years thanks to a favorable economic environment, persistently low inflation and the risks weighing on the eurozone could lead the ECB to lower its deposit rate again as early as September 2019. In this case, it is very likely that the ECB will also create a system of tiered remuneration for excess reserves in order to support banks’ profitability in the face of negative rates.

Sources:

1/ BSI Economics – What is the « expectation hypothesis »? (2014)

http://www.bsi-economics.org/270-??-l-expectation-hypothesis-de-quoi-sagit-il

2/ Federal Reserve Bank of Dallas – The neutral rate of interest – Robert Kaplan (2018)

https://www.dallasfed.org/news/speeches/kaplan/2018/rsk181024.aspx

3/ Federal Reserve Bank of San Francisco – Working paper – Measuring the natural rate of interest: international trends and determinants – Holston, Laubach & Williams (2016)

https://www.frbsf.org/economic-research/files/wp2016-11.pdf

4/ IMF – Working Paper – Negative Monetary Policy Rates and Portfolio Rebalancing:

Evidence from Credit Register Data (2019)

5/ Benoît Coeuré – speech at Yale University – Assessing the implication of negative interest rates (2016)

https://www.investing.com/central-banks/european-central-bank/speeches/assessing-the-implications-of-negative-interest-rates-200146901

6/ ECB – How to calculate the minimum reserve requirements?

https://www.ecb.europa.eu/mopo/implement/mr/html/calc.en.html

7/ECB – Key ECB interest rates

https://www.ecb.europa.eu/stats/policy_and_exchange_rates/key_ecb_interest_rates/html/index.en.html

8/ Deutsche Bank – European bank profits rise to post-crisis peak despite lower revenues in 2018 – capital ratios down for the first time – Jan Schildbach (2019)

9/ IMF – Policy paper – Negative interest rate policies – initial experiences and assessments (2017)

10/ ECB – Working paper – Do negative interest rates make banks less safe? (2017)https://www.ecb.europa.eu/pub/pdf/scpwps/ecb.wp2098.en.pdf

11/ European Parliament – Monetary dialogue – Post-crisis Excess Liquidity and Bank Lending (2018) http://www.europarl.europa.eu/cmsdata/153221/LSE_FINAL.pdf

12/ Draghi, Interview at the Peterson Institute for International Economics (2017)

13/ ECB – Press conference – Mario Draghi (July 25, 2019)

https://www.ecb.europa.eu/press/pressconf/2019/html/ecb.is190725~547f29c369.en.html

14/ IMF – Working paper – Negative interest rate policy: implications for monetary transmission and bank profitability in the euro area (2016)