The latest forecasts from the International Monetary Fund (IMF) in April 2018 predict global growth of 3.9% in 2018, compared with 3.7% in 2017. This growth is expected to be driven largely by emerging countries (average growth of 4.4% in 2018, making it the most dynamic region). Advanced economies are also expected to benefit from the upturn in 2018 (2.7%), although this will be less pronounced than in emerging economies (+0.178 ppt compared to 2017 for emerging economies versus +0.017 ppt for advanced economies).

Eight countries are expected to be in recession in 2018, fewer than in 2017: Dominica, Equatorial Guinea, Nauru, Puerto Rico, South Sudan, Swaziland, Venezuela, and Yemen. 92 countries (out of 193) are expected to record growth above the global average, the vast majority of which are Asian countries (emerging Asia recorded average annual growth of 6.5%) and certain African countries (with average growth of 3.4% in sub-Saharan Africa). In 2018, Ethiopia is expected to be the fastest-growing country in the world (8.5%) outside of Libya, which is catching up after several years of conflict. Growth in the United States is expected to be 2.9%, in the eurozone 2.4%, and in China 6.6%.

The strongest progress compared to 2017 is expected to be recorded in the Middle East and North Africa region (+0.961 ppt for average growth of 3.2%), which suffered a serious decline in 2017, and by Central and South America (+0.734 ppt for an average growth rate of 2.0%), where growth had already recovered in 2017 after a recession in 2016.

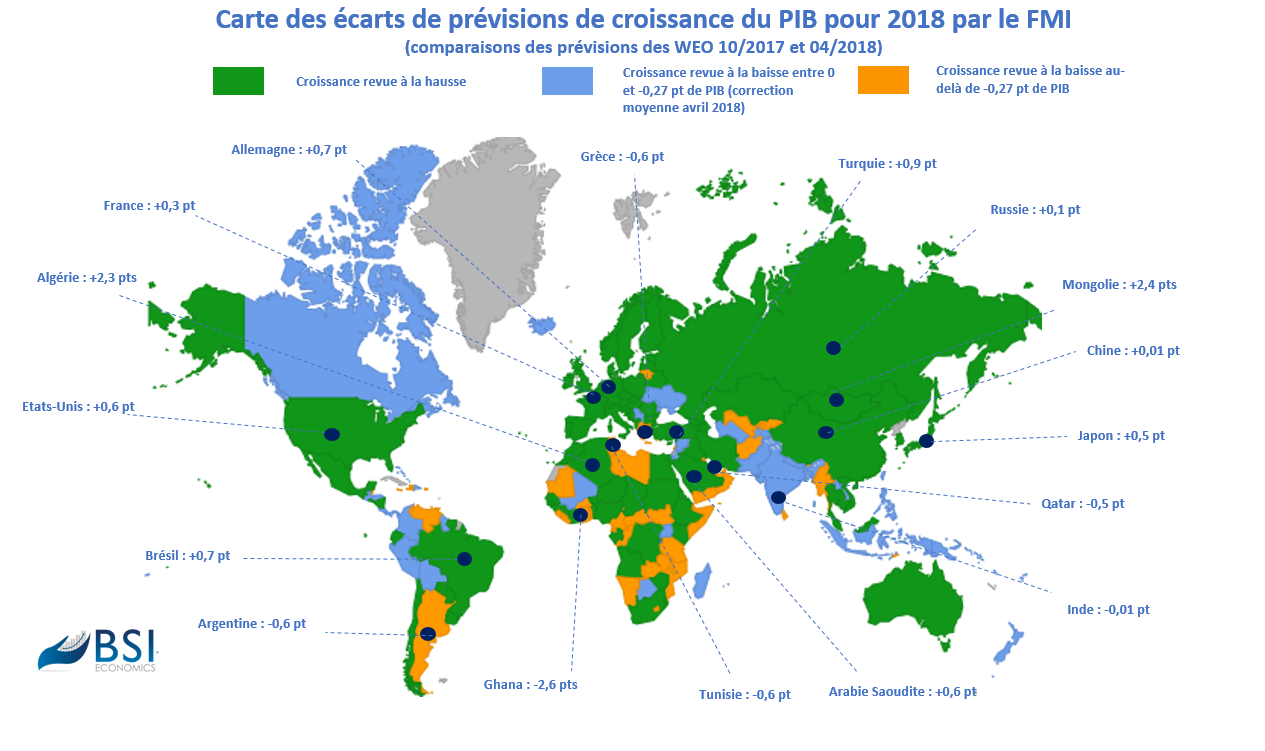

Between the April 2018 forecasts and the previous ones dating from October 2017, the IMF made numerous adjustments to growth for 2018. Indeed, despite an overall improvement, the average adjustment per country is -0.274 ppt between October 2017 and April 2018. At the same time in 2017, this adjustment was also negative (-0.03 ppt); over the past two years, adjustments have generally been more lenient when growth forecasts are revised in October.

Growth forecasts were therefore revised downwards for 96 countries (compared with 97 countries for which they were revised upwards, but the scale of the downward revision is on average greater than the average upward adjustment), including Argentina (-0.6 pts), Ghana (-2.6 pts), Greece (-0.6), and Tunisia (-0.6). Several Asian countries are expected to post high growth figures but will nevertheless see slight declines (India, Indonesia, Malaysia, Philippines).

In developed countries, the gradual normalization of monetary policy seems to be a done deal, but financing conditions for these economies will remain fairly accommodative and should therefore continue to support growth in the eurozone and the United States. Positive externalities linked to the expansionary US fiscal policy following the December 2017 tax reform are expected for the United States, but also for the rest of the world. According to the IMF, the strengthening of economic fundamentals and the improvement in the outlook would be particularly significant in Ireland (+1.1 pts), Switzerland (+1.0 pts), Germany (+0.7 pts), and the United States (+0.6 pts). Countries such as France, Italy, and Spain have also seen their growth prospects revised upwards by the IMF, but to a lesser extent, while Canadian growth has undergone a slight downward correction (-0.04). The renewed dynamism in the eurozone will also benefit emerging Europe, which remains highly dependent on the economic situation in Western Europe, explaining the upward revision of growth figures in Eastern Europe for 2018.

In 2017, emerging economies benefited from strong Chinese demand. Although an economic slowdown is expected in China, growth will remain high (the IMF has left its forecast of 6.6% growth in 2018 virtually unchanged) and a scenario of hard lending therefore seems unlikely at this stage. Consequently, continued high growth in China will support global growth, particularly in emerging countries. In addition, the recovery in commodity prices could partly explain the improved outlook for emerging market exporters, particularly in Africa. For example, the IMF expects oil prices to reach USD 62.3 in 2018, compared with USD 52.8 in 2017. Growth forecasts for oil-exporting countries have therefore been revised upwards. These countries could effectively accumulate revenues again, giving them more room for maneuver to break with austerity and better support economic activity. This is particularly the case for Algeria (+2.3 pts), Saudi Arabia (+0.6 pts) and, to a lesser extent, Russia (+0.1 pts), which is still weakened by financial sanctions.

Despite a reduction in risks in 2018 and an overall upward growth outlook, not all risks have been eliminated. Tighter financial conditions in advanced countries could increase the external vulnerability of some emerging countries (especially those with a lack of savings and high external financing needs). Chinese growth is not necessarily based on solid economic fundamentals (high private debt, financial risks) and any slowdown greater than anticipated would have significant repercussions. While 2017 was marked by very strong global demand and Q1 2018 seems to be following the same trend, the introduction of tariffs in the United States (on steel and aluminum) could spark renewed interest in protectionist theories. The risk of a « trade war » would then pose significant risks to global growth.