⚠️Automatic translation pending review by an economist.

BSI Economics Consensus consults a panel of economists working in France and internationally within public, private, institutional, and academic structures. Consensus surveys these specialists on economic and financial risks to identify the challenges for the coming months.

BSI Economics Consensus July 2018:

1- Slowdown in activity in the eurozone

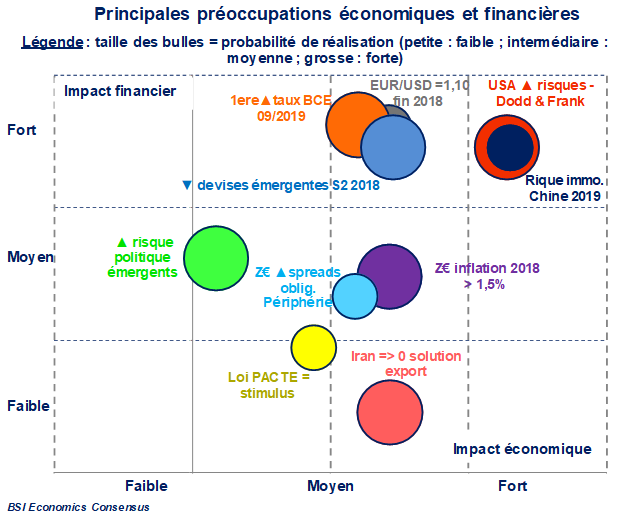

According to 55% of the economists surveyed, there is a strong likelihood of inflation in the eurozone exceeding 1.5% by the end of 2018. This inflation would be mainly driven by rising energy prices. While these prices weigh on household purchasing power and corporate margins, financial conditions would remain favorable and could therefore mitigate the negative impact of the energy bill. After a dynamic 2017, economic growth is expected to slow in the eurozone. In the specific case of France, the potential impact of the PACTE law on private investment and corporate financing could become apparent in the medium term, but this is not a strong conviction among the sample in this Consensus.

The European Central Bank (ECB) is expected to proceed with a gradual and very progressive normalization of its monetary policy, i.e., a policy that will remain fairly accommodative, at least in the short and medium term. Nearly 70% of Consensus economists anticipate a rise in the key interest rate as early as September 2019. Even though interest rate differentials no longer capture or explain currency fluctuations, only 13% of economists believe there is a high probability of the euro depreciating against the US dollar by the end of 2018 (EUR/USD at 1.10). This situation would prevent spreads from widening further in peripheral countries, despite the political risk remaining palpable (see section « What are the risks in 2018? »).

2- Risksto US growth in the medium term

Tax reform in the United States is helping to accelerate economic activity, with GDP growth forecast to be close to 3% in 2018. This acceleration does not call into question the normalization of monetary policy initiated by the Federal Reserve (Fed). Increased uncertainty, particularly regarding protectionism, makes a sharp depreciation of the USD between now and the end of 2018 unlikely at this stage.

While the rise of protectionism has already been discussed in previous issues of Consensus, the current issue focuses on medium-term financial risks.

While the rise of protectionism has already been discussed in previous issues of Consensus, the current issue focuses on medium-term financial risks.

Fifty-six percent of economists believe that the repeal of the Dodd-Frank Act is highly likely to pose a significant risk to financial stability. None of the economists surveyed consider this event to be unlikely. It would even have a significant impact on global growth and asset allocation for a majority of the economists surveyed, the only question presenting this characteristic, along with the one concerning financial risks in China.

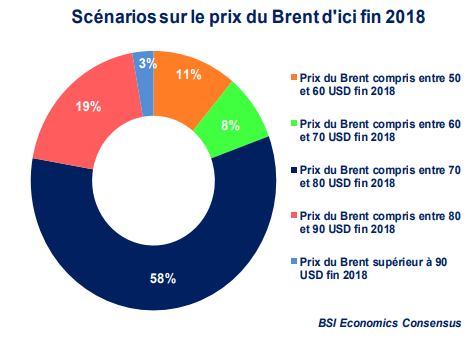

Despite a sharp rise in oil prices over the past year (78% of respondents believe that the price of Brent crude will exceed USD 70 per barrel by the end of 2018, compared with only 23% in the previous quarter) and a recovery in commodity prices, significant uncertainties remain in emerging countries (see section entitled « What are the risks in 2018? »).

Trade tensions are likely to contribute to a slowdown in global economic growth in the medium term and have a direct and indirect impact on emerging countries. The firm stance taken by the US leaves little room for hope, as evidenced by the situation in Iran on another issue (63% of respondents do not foresee a favorable outcome for exports to Iran). While the growth outlook remains positive at this stage, uncertainties are emerging, particularly in the form of emerging market currency depreciation. This scenario is likely to continue until the end of 2018, with a high probability of occurrence for 56% of respondents; China is not immune to this situation. The stability of its currency is a key objective, as is the strengthening of financial stability. Financial and/or real estate risks could resurface as early as 2019, but no clear trend emerges from the Consensus to determine the likelihood of such an event occurring.

What are the risks to growth in 2018?

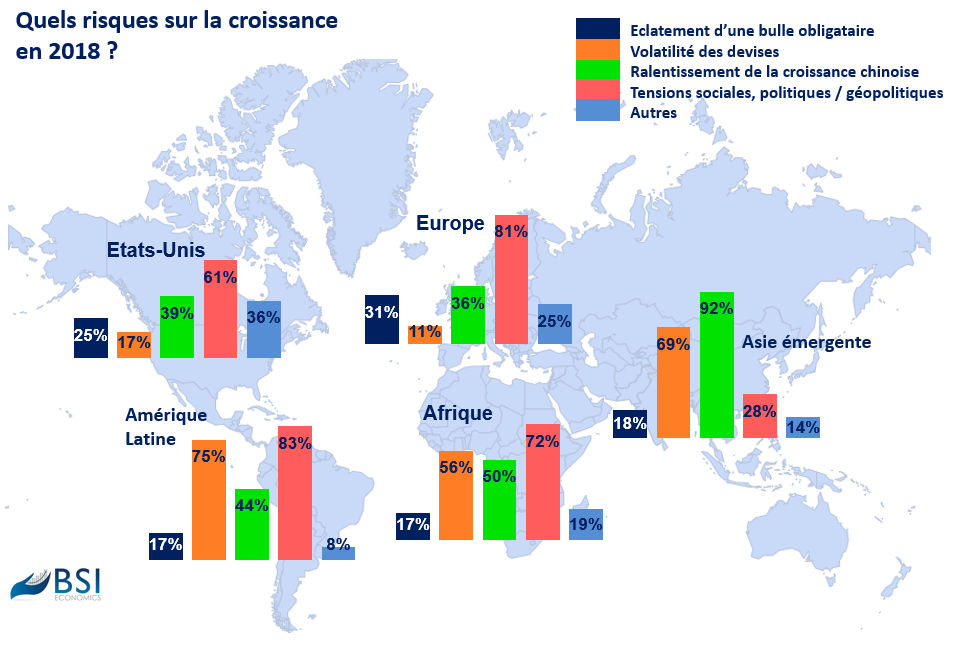

This mapping of risks to growth shows that no region will be spared in 2018 and that all will be affected to a greater or lesser extent by different types of risk.

Compared with the results of the previous Consensus, the bursting of a bond bubble is causing less concern in the United States and Europe: currently 31% of respondents in Europe are concerned (compared with 48% a quarter ago) and more than 25% in the United States (compared with 53% in the previous quarter). This decline can be explained in particular by the effective forward guidance provided by central bankers as part of the gradual normalization of their monetary policy. Social and political/geopolitical risk remains significant in the United States (61% of respondents) but especially in Europe, where this risk is cited by 81% of economists surveyed. Several events are fueling this risk: the advent of a Eurosceptic coalition in Italy, the handling of Brexit (especially with the increasing number of resignations in the British government), the many sources of tension with the United States (tariffs, NATO, rising protectionism, exports to Iran), the standoff between the European Union and Poland over the rule of law, and the continuing high level of social risk with growing inequalities, etc.

The risk of a slowdown in Chinese growth is seen as more significant in emerging markets than in developed countries (39% of respondents in the US, 36% in Europe) and particularly in emerging Asia (92%), countries directly affected by the decline in value chains. Countries that export raw materials (particularly minerals and metals, in Africa and Latin America) would also be affected by a decline in Chinese demand. The prospects of a « trade war » between China and the United States could also have repercussions on the rest of the emerging world through second-round effects.

After benefiting from favorable carry trade, investments in emerging currencies are now less attractive with the rise in interest rates in developed countries, particularly in the United States. As a result, new arbitrage has maintained downward pressure on emerging currencies, and the trend toward capital outflows is expected to continue in H2 2018. Currency volatility is therefore a significant risk in 2018 for three out of four economists in Latin America, with the Argentine peso being a perfect example. This risk also affects emerging Asian countries, according to 69% of the panel, even as China is currently trying to remedy the fall of the renminbi. In Africa, this risk is less pronounced but still concerns 56% of the panel.

Outside emerging Asia, socio-political and geopolitical tensions will remain high in Africa (72%) but especially in Latin America (83%: election of a populist candidate in Mexico, uncertainty over NAFTA and the outcome of the Brazilian elections).