Summary:

– The decentralization process is not yet complete in Morocco;

– Local authorities are merely administrative intermediaries and are subordinate to the central authority;

– Transfers from the central government account for one-third of Moroccan municipalities’ resources;

– The mobilization of local tax resources depends on socioeconomic and demographic factors and not only on the decentralization system.

Decentralized management of local affairs has undoubtedly proven to be an essential mode of governance for addressing local development challenges. Decentralization also makes it possible to take into account local disparities in preferences regarding local public services. In Morocco, decentralization reforms have multiplied since independence. Following the 2015 local elections, Morocco is in the process of completing the implementation of the advanced regionalization project launched in 2011. This project aims to modernize local authorities by promoting proximity and accountability in the regions. The number of regions has been reduced from 16 to 12. The administrative division still comprises three levels: regions, provinces/prefectures,and municipalities.

The choice of decentralization in Morocco was accompanied by the establishment of a mechanism for mobilizing financial resources. In addition, particular importance is given to local taxation, which is a key instrument for financing local public facilities. The effectiveness of decentralization can be measured in terms of local expenditure management and local resource mobilization.

Using budget data from more than 920 Moroccan municipalities for the period 2005–2009, this article aims, first, to provide a general overview of the budgetary situation of municipalities. Next, we present the various problems and difficulties of local taxation. Finally, we offer some recommendations for improving local tax mobilization.

Evaluation of the municipal budgetary system in Morocco

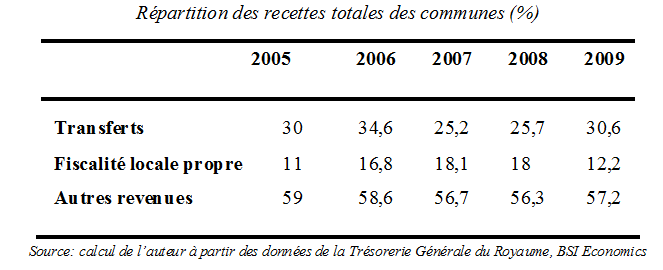

In order to evaluate budgetary decentralization in Morocco, it is necessary to examine the distribution of the main sources of municipal revenue and the autonomy of revenue management. Moroccan municipalities enjoy greater autonomy in the management of local taxes and user fees than in the management of VAT transfers or debt, which represent a significant share of municipal revenues (see table below).

Municipal revenues are divided into two categories:

· Operating revenue related to local taxation, taxes, and transfers, on the one hand;

· And capital revenue consisting of proceeds from the sale of private property, previous surpluses, matching funds, and loans, on the other hand.

We have grouped these different types of revenue into three categories:

1. The first category of resources, « local taxation, » consists of local taxes[4] and taxes managed and collected by the tax authorities on behalf of municipalities[5] (business tax, housing tax, and municipal services tax);

2. The second category includes resources linked to transfers from the central government.

3. The third group, « other income, » includes revenue from assets, previous surpluses, and loans.

Between 2005 and 2009, the share of local taxation in total municipal revenue was minimal (between 10% and 19%) compared to other categories of resources and did not increase despite the various reforms implemented during this period (Law 47-06, VAT reform in 2006, etc.). This share remains relatively low compared to other resources and, all other things being equal, can be explained by a set of problems that will be presented in the following section.

The various problems with local taxation in Morocco

Local taxation in Morocco presents various anomalies in its functioning and administration across several levels. Firstly, with regard to the housing tax (formerly the urban tax), it should be noted that local authorities are required to update certain tax bases by adjusting rates in line with economic data. This is the case with rental values, which often date back several decades and contribute to low property tax revenues.

Next, with regard to the collection of municipal taxes and duties, it should be noted that this is carried out by three different government entities. On the one hand, by the municipality through the municipal tax collector, who has neither the human nor material resources to identify, register, and collect specifically local taxes and duties. On the other hand, it is carried out by decentralized services under the Ministry of Finance, which retain the management and collection of taxes that have been fully transferred to the municipalities, namely the urban tax and the business tax. Finally, services under other administrations are responsible for the management of certain local taxes.

The shared management of local taxation by these different entities can lead to difficulties in communication and information exchange, as well as a lack of interest on the part of those who manage or collect on behalf of third parties. Furthermore, the sharing of a tax base between several levels of government and the lack of specialization of taxes by level of local authority can weaken the link between the taxpayer and the elected representative, since the person responsible for a tax increase or decrease is not immediately identifiable by the taxpayer. In addition, municipalities are sometimes unable to collect tax revenues in cases of under-reporting, as they must call on the General Tax Directorate or the Kingdom’s General Treasury.

Finally, the creation of taxes falls under the authority of the legislative body, i.e., the central government. Municipalities essentially act as tax collectors and can only set, within the framework of laws and regulations, the basis of assessment, rates, and rules for collecting the various taxes, fees, and duties they levy. Furthermore, local taxation is caught between two stools, which only adds to the complexity of the system. It is subject to both local policies, such as the choice of tax rates, and national policies, such as exemptions for economic purposes. This deprives municipal budgets of significant uncompensated revenue. Decentralized taxation is therefore in reality only a local extension of state taxation (Sbihi, 2007).

Given this observation, Morocco still has a long way to go before achieving a significant degree of budgetary decentralization. However, excessive autonomy for municipalities may lead them to develop their own taxation strategies (Madiès et al., 2005). For example, the location of the tax base may be sensitive to taxation, which can lead to competition between local governments (« tax competition ») (Salmon, 1987).

Transfers account for a significant share of municipalities’ total revenues. This share has been steadily increasing, from 36.9% in 2005 to 39.2% in 2009. In Morocco, transfers consist of VAT amounts that are distributed among the various local authorities, accounting for 30% of the total amount. For municipalities, there are three criteria used to determine the amounts of these transfers, with the aim of reducing inequalities between municipalities:

-The « flat-rate grant »: a grant that is essential for the functioning of the municipality, it is the same for all local authorities.

-The « tax potential grant »: this reduces disparities in tax revenue resulting from the uneven distribution of taxable income.

– The « own resources promotion grant »: this aims to encourage municipalities that have made an effort to manage and collect tax resources by awarding a bonus proportional to the effort when it is greater than or equal to 0.65 times the national average.

Some elements for better local taxation

All these dysfunctions, from the creation of taxes to their collection, including the undervaluation of the tax base, only serve to make local taxation less competitive and reduce its importance in the total revenue of municipalities.

In light of this, the central government must undertake a major effort to create a simplified tax system (reducing the number of taxes and consolidating levies) specific to municipalities (creation and collection of taxes at the local level) in order to give fiscal decentralization its local meaning. Full involvement of municipalities in the collection of local taxes, through improved guidelines for taxpayers and the application of appropriate penalties for tax fraud, will enable them to take on more responsibilities and mobilize more tax resources.

In the same vein, municipalities should inventory their assets and update concession fees by adjusting prices to market value. This would encourage municipalities to adopt modern computerized valuation and geographic information techniques. In addition, double taxation should be avoided and harmonization between local and central taxation ensured, given that taxpayers are sometimes subject to multiple taxes. The latter is often a hindrance rather than a source of tax revenue, as it generates unnecessary collection costs and encourages tax evasion. A reduction in their number should be considered in order to reduce counterproductive overtaxation (« too much tax kills tax ») and to merge duplicate taxes, such as the tourist tax and the tourism promotion tax, or the tax on beverage sales and VAT.

The objectives of the transfers mentioned above are not always achieved due to the application of these criteria. Indeed, the « flat-rate grant » criterion is heavily criticized because it grants additional resources to wealthy municipalities by treating them in the same way as poor municipalities. The « tax potential grant » criterion is based on estimated revenues and its application differs from one municipality to another. Similarly, the latter criterion risks increasing disparities between municipalities by rewarding wealthy municipalities more. These criteria remain essentially fiscal and are not linked to the socioeconomic data of the municipalities. A system of equalization that is also based on socioeconomic criteria, such as investment, promotes local development.

Furthermore, an econometric study conducted on the same database with the aim of explaining local tax mobilization in Morocco showed that municipal tax revenues depend on several factors. Poverty, inequality, fiscal decentralization, and the municipality’s environment (rural or urban) have a positive impact on municipal tax revenues. Based on this observation, in order to promote the mobilization of local tax resources, it is necessary to address all the factors involved in this mobilization: not only is it necessary to implement a relevant local tax system (not dependent on subsidies or transfers) to ensure financial autonomy, but it is also necessary to identify the overall factors (poverty, inequality, number of inhabitants in the municipality, etc.) that constitute obstacles to the mobilization of local resources and take action to promote an environment more conducive to this mobilization.

Conclusion

In order to address the various issues related to local taxation on the one hand, and to give decentralization its most advanced form on the other, Morocco is currently implementing the advanced regionalization project. Advanced regionalization allows local authorities to take on more responsibility and become more autonomous from the central government. This enables them to leverage their own resources to contribute to the economic and social development of their citizens. This autonomy will also encourage them to compete, which should motivate them to improve their efficiency and performance in providing public goods.

Effective mobilization of local tax resources is a necessary condition for this provision at the local level, as local resources make it possible to establish a direct accountability relationship between local elected officials and citizens. This allows citizens to easily assess the performance of the territories where they live without shifting responsibility to the central government, as is the case in most situations.

Bibliography

Chambas G. (2010): « Mobilizing local resources in sub-Saharan Africa, » Economica.

Madiès, Paty and Rocaboy, (2005): « Horizontal and vertical fiscal externalities. Where does the theory of financial federalism stand? », Revue d’économie politique, Dalloz, vol. 115(1), pages 17-63.

Salmon P., (1987): “Decentralization as an incentive scheme,” Oxford Review of Economic Policy, Vol. 3, pp. 24-43.

Sbihi M., (2007) “Fiscal decentralization: The Moroccan experience,” CeSPI.

[1] Before the 2015 local elections, there were 16 regions, each composed of prefectures and provinces, which are made up of municipalities. There are 13 prefectures covering the main urban areas. The 62 provinces cover small urban areas and nearby rural areas. Finally, there are 1,503 municipalities (221 urban and 1,282 rural).

[2] These are sources of funding for local authorities such as taxes, transfers of tax revenues collected by the state, loans, and subsidies.

[3] Chambas (2010) shows that decentralization in African countries has often been accompanied by an imbalance between the capacity of local jurisdictions to mobilize resources and manage the expenditures and responsibilities transferred to them.

[4]These include a range of taxes, fees, and contributions affecting various sectors (real estate, administrative, tourism, commercial, etc.).

[5]Ninety percent of these taxes are allocated to municipalities, with the remaining 10% going to the central government budget to cover collection costs.

[6] For example, the transport administration for the tax on driving licenses, the fisheries office for fees on sales in wholesale markets and fish markets, and the water and forestry department for the tax on the sale of forest products.

[7]The legislature has provided for a very high number of taxes and duties, which is not necessarily synonymous with fiscal efficiency. On the contrary, it can be the source of a complex and cumbersome system that undermines any chance of productivity (Sbihi, 2007).

[8]In some rural municipalities, taxes and duties are included in the « fiscal potential » allocation along with other resources such as forest products and market fees.