Decline in emerging countries’ foreign exchange reserves: Should we fear a tightening of financial conditions? (1/2)

Summary:

· After peaking at USD 8.2 trillion in June 2014, emerging market foreign exchange reserves have fallen by more than 18%.

· This trend is likely to continue due to slowing growth in emerging countries, the new regime in commodity markets, and the structural transition underway in several major economies in the region, including China.

· The accumulation of foreign exchange reserves by emerging countries had a significant impact on sovereign interest rates in advanced economies during the 2000s. The reversal of this trend is expected to have a major impact on these rates through two channels: global liquidity and portfolio rebalancing.

· Despite the decline in emerging countries’ foreign exchange reserves, global liquidity is not falling at the moment. This is due to the sterilization policy of emerging countries and the continuation of quantitative easing in advanced economies.

The downward trend in sovereign interest rates observed over several decades in advanced economies is attributed in academic literature to a growing excess of ex ante savings over ex ante investment .

A myriad of factors are generally put forward to explain this persistent imbalance between desired savings and investment, including the significant expansion of savings in emerging economies since the Asian crisis (Bernanke 2005). This increase in savings has led to an accumulation of reserves by emerging countries, which is one of the striking features of the transformation of the global financial architecture in the 2000s.

However, these reserves are now declining. This new trend is likely to have major consequences for asset valuations in advanced economies and the financing of the global economy. In the following, we review the determinants of the evolution of emerging countries’ foreign exchange reserves and then examine the impact of their erosion on the level of global liquidity.

1- Emerging market foreign exchange reserves: from accumulation to erosion

With their growing integration into the global economy, their increased participation in world trade, and the establishment of a regime of persistently high prices on commodity markets during the first decade of this century, emerging countries have seen a significant acceleration in their national income. At the same time, the national savings rate has continued to grow, rising from 22% of GDP in emerging economies[1] to 33% in 2008. This proven trend is attributed to a number of factors, including the modest level of development of the financial sector in emerging countries, financial repression, weak social protection systems, and institutional structures or corporate governance that do not encourage maximizing shareholder returns. Added to these factors are demographic dynamics, cultural factors, persistent habits, and significant inequalities (Ferrucci and Miralles 2007, Prasad 2009, Ma and Yi 2010).

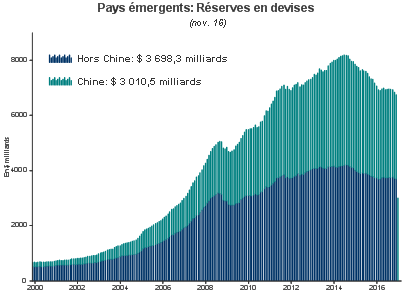

In fact, with accelerating growth and rising savings, emerging economies recorded an average current account surplus of 2% of GDP per year between 2000 and 2014 (Figure 1). Coupled with a financial account deficit [2] in the very specific case of China, this positive current account balance should have led to a significant appreciation of emerging market currencies, which was avoided thanks to the accumulation of colossal foreign exchange reserves. These reserves peaked in June 2014 at nearly USD 8.2 trillion, almost half of which was held by China. Still scarred by the trauma of the balance of payments crises of the 1980s and 1990s, emerging countries, in search of liquid assets with low credit risk, have often recycled these reserves into the sovereign debt markets of advanced economies, contributing to the decline in long-term interest rates and the development of the famous « conundrum » that baffled Alan Greenspan( Greenspan 2005).

Figure 1

However, emerging market savings are currently declining. The trend in commodity markets has reversed, and prices are expected to remain much lower than in the past, particularly for oil (Arezki and Matsumoto 2016). Demand from advanced economies has weakened significantly and global trade is sluggish. Finally, some emerging economies, including China, are undergoing a structural transition to a growth model that relies more on private consumption and requires lower savings. In fact, according to the IMF, the emerging market area’s current account surplus turned into a deficit in 2015, which is expected to persist until at least 2021.

At the same time, in China, capital inflows slowed and eventually turned into capital outflows. This trend could be sustainable insofar as it constitutes an « endogenous response to deteriorating growth prospects and weakening commodity prices, » as noted by Clark et al. (2016), although capital controls could slow it down in the short to medium term. According to their study’s estimates, a sustained increase in the growth differential between an emerging country and advanced economies of one percentage point tends to be associated with an increase in net capital inflows of a quarter of a percentage point of GDP. In China’s case, the opposite effect is likely to be observed: the growth differential with advanced economies is expected to be 4.4 points between 2016 and 2020, compared with 7.7 points between 2000 and 2015, according to IMF estimates. With this narrowing of the growth differential, the Chinese economy has therefore been posting net capital outflows[4] continuously since Q2 2014, i.e., for eleven consecutive quarters, a development unprecedented since at least the mid-1990s.

The disappearance of the current account surplus (and the reduction of the financial account deficit) should lead to a depreciation of domestic currencies. Some major emerging countries, including China, are attempting to smooth or halt this trend by drawing on their reserves in order to limit the adverse effects of a sharp fall in exchange rates on financial stability. As a result of exchange rate management policies, emerging market foreign exchange reserves have fallen by more than $1.4 trillion since June 2014, with China accounting for two-thirds of this decline. It should be noted, however, that part of this decline is simply due to a valuation effect, as emerging market reserves are largely invested in dollars (60% according to a consensus estimate), while the US currency has appreciated by 23.5% in effective terms since mid-2014, automatically reducing the value of assets invested in euros, yen or pounds sterling[5].

Chart 2

2- Emerging market foreign exchange reserves and global liquidity:

The fact remains that the decline in reserves is very real and long-term. This trend raises two distinct questions. The first concerns the evolution of global liquidity as a whole. The second concerns the holding of sovereign debt from advanced economies. Thus:

1- Global liquidity:Emerging economies account for two-thirds of the growth in global money supply (M2). All other things being equal, the decline in their foreign exchange reserves should lead to a contraction in their central banks’ balance sheets. Is it therefore legitimate to fear « quantitative tightening, » which would be the opposite of the quantitative easing implemented in advanced economies (Bloomberg, September 2, 2015, September 19, 2016)?

2- With regard to holdings of risk-free assets issued by advanced economies:If the accumulation of foreign exchange reserves by emerging economies had led to a decline in sovereign interest rates in advanced economies, shouldn’t their decline push these rates up? In other words, if causality works in one direction, shouldn’t it work in the opposite direction?

In the following, we will attempt to shed light on the first question and leave the answer to the second for the second part of this note.

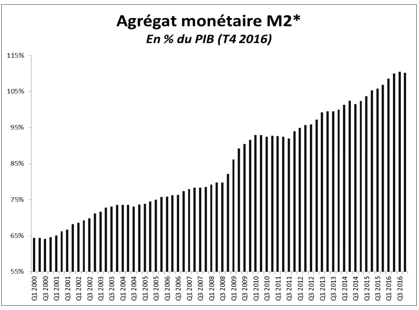

Globally, the decline in emerging countries’ reserves could lead to a contraction in the balance sheets of the central banks concerned only if they do not sterilize their interventions in the foreign exchange market. Sterilization can take different forms ( repo facilities, open market operations, etc .) and be accompanied by complementary measures (reductions in reserve requirements) in order to limit or even offset the impact of the decline in reserves on the money supply. In China, the PBOC’s total assets contracted year-on-year between September 2015 and June 2016, falling from more than 53% of GDP at the end of 2013 to 46% in Q4 2016. Nevertheless, the 300 basis point reduction in reserve requirements since January 2015 has increased the money multiplier. Together with the intensification of liquidity injections in Q1 2015 and throughout 2016, this has fueled continued growth in the money supply. The M2 aggregate thus peaked at a historic high of 208% of GDP at the end of 2016, compared with 186% three years earlier, despite capital outflows and a decline in foreign exchange reserves.

Overall, sterilization policies in emerging markets and continued quantitative easing in several advanced economies have allowed global money supply to continue to grow. According to our estimates, the money supply reached a historic high of 110% of global GDP in Q4 2016 (Chart 3). It therefore does not appear to have been significantly affected by the decline in emerging market reserves.

Chart 3

* Estimates based on a sample of countries representing 84% of the global economy. M2 is estimated as the sum of the ratios of aggregates to GDP in domestic currency, weighted by each country’s share of global GDP estimated in PPP, in order to mimic the significant valuation effects that could be generated by an estimate based on current exchange rates.

Sources: National authorities, IMF, BSI Economics estimates

Conclusion:

A lasting trend, the decline in emerging market reserves has yet to have any negative impact on global liquidity levels. In the future, it could lead to quantitative tightening ( QT) if the sterilization currently pursued by the central banks concerned comes to an end. At the same time, a partial halt to the rollover of assets held by the Fed could also encourage the advent of QT. This measure, which has been increasingly discussed in public debate recently, could have significant consequences for the global economy that are difficult to estimate in the absence of a consensus on the impact of QE on asset prices and its transmission to the real economy.

[1]As defined by the IMF.

[2]In other words, an accumulation of external liabilities, excluding changes in reserves.

[3]In his speech to the US Senate on February 17, 2005, Alan Greenspan, then Chairman of the Fed, described the downward trend in long-term interest rates in the United States as a « conundrum » despite a 150 basis point increase in the Federal Reserve’s benchmark rate.

[4]Calculated as the sum of the financial balance and « errors and omissions » in the balance of payments.

[5]As the exact breakdown of foreign exchange reserves by currency is unknown at the aggregate level, as is the case for China, it is impossible to calculate the valuation effects resulting from the appreciation of the dollar. By way of illustration, it should be noted that a country whose foreign exchange reserve investment strategy replicated the weightings of the SDR basket before the inclusion of the yuan in that basket would have seen its reserves melt away by 10% between Q2 2014 and Q4 2016 due to the appreciation of the dollar.

[6]When a central bank sells part of its foreign exchange reserves, it receives a certain amount of domestic currency in exchange, which is then withdrawn from circulation. This reduces the money supply at the domestic level. Conversely, when it accumulates foreign exchange reserves, the central bank increases the domestic money supply. Sterilization consists of the central bank offsetting the effect of foreign exchange interventions on the domestic money supply through injections or withdrawals of liquidity.