On Sunday, July 5, the Greek people will vote in a referendum for or against accepting the terms of the creditors’ offer. The announcement of the end of negotiations between Athens and its creditors and the holding of a referendum to ask the Greek people whether they « accept the terms of the creditors’ offer » took Europeans and the markets by surprise. However, the underlying issue is Greece’s membership in the eurozone, since without an agreement, the country would be forced to leave the monetary union. In fact, the probability of a « Grexit » has increased significantly, with S&P now estimating it at 50%.

Faced with this sudden political tension, the financial markets, both equities and bonds, have been particularly erratic this week, without however triggering a « domino effect » as was the case in 2012. Indeed, multiple factors (improvement in the economic climate, impact of the ECB’s action, strengthening of European institutions) limit the risk of a systemic economic and financial crisis erupting in the event of Greece’s exit.

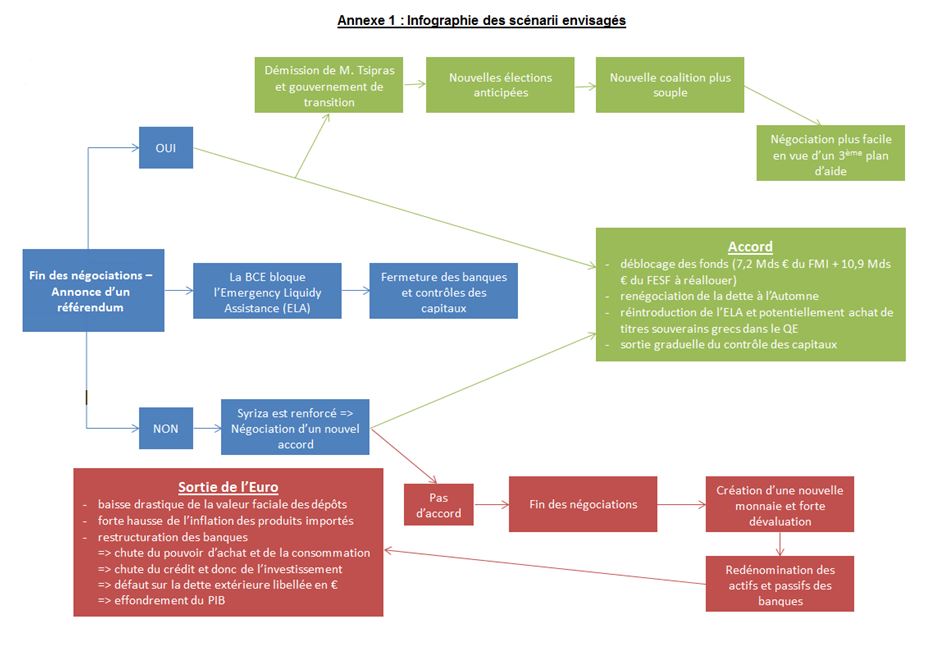

If the « No » vote wins on Sunday, the most likely scenario would be a « Grexit. » On the other hand, a « Yes » victory would virtually guarantee an agreement and a change of government. To date, all observers expect a « Yes » victory.

1 – Foreword

For the time being, and despite the non-repayment of €1.6 billion to the IMF (June 30), Greece has not been declared in default, as this event is considered to be a payment arrears with the institution.

However, it should be noted that Greece’s debt has once again been downgraded by all rating agencies to the level just below default (CCC- by S&P, Caa3 by Moody’s, CC by FitchRatings).

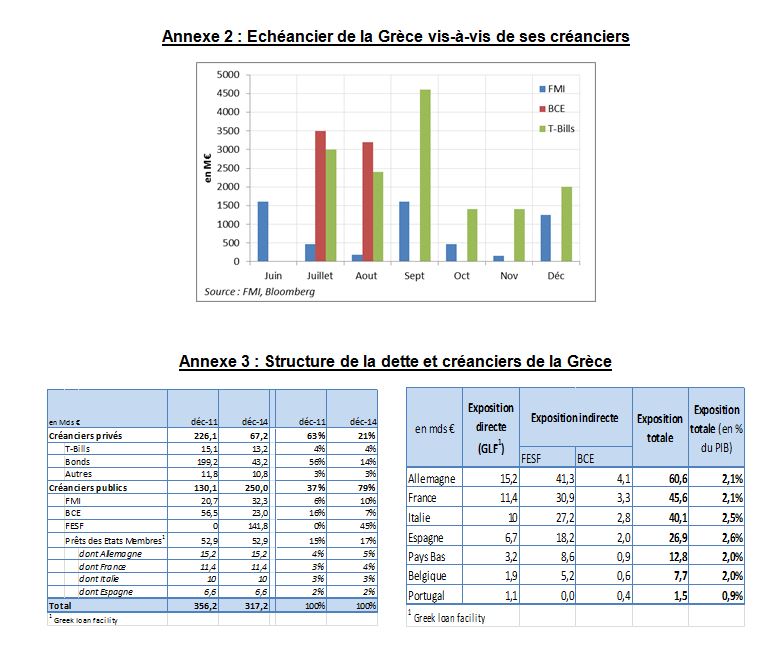

On the other hand, failure to pay the amounts due to the ECB in July and August (see Appendix 2) would result in the Greek sovereign defaulting. This payment will depend on reaching an agreement with its creditors and therefore on the outcome of this Sunday’s referendum.

2 – Overview of the Greek banking system

Since early February, and the ECB’s decision to close the Eurosystem to Greek banks, Greek banks have been facing significant financing difficulties. Faced with massive deposit withdrawals (€30 billion since the beginning of the year as of May), the only source of financing is Emergency Liquidity Assistance[1],as the banking system is unable to issue securities on the financial markets.

On several occasions, the ECB has had to raise the ceiling on Greek banks’ eligibility for ELA in order to finance themselves. It should be noted that Greek banks, which were recently recapitalized under previous aid plans, are considered solvent ( Core Equity Tier 1 ratios above the minimum required by the regulator) and that this is indeed a liquidity crisis.

Following the Greek government’s decision to withdraw from negotiations and hold a referendum, and faced with the substantial risk of default, the ECB decided to refuse to raise the ELA ceiling again (currently €89 billion), but without canceling it (such a decision would have caused the entire system to collapse). Unable to continue financing himself, Mr. Tsipras announced the closure of Greek banks (until Monday, July 6, the day after the vote).

Thus, while polls showed the « No » vote winning by a wide margin when the referendum was announced, the ECB’s decision, followed by the Greek government’s decision to close the banks, has largely reshuffled the deck.

Faced with daily operational constraints for Greeks(unable to withdraw more than €60 per day from bank counters), the « Yes » vote now seems to be winning.

3 – A « Yes » victory would ensure an agreement and political change in Greece…

If the « Yes » vote wins on Sunday, Greece would commit to accepting the latest offer presented by its creditors. This offer can be summarized as follows:

Furthermore, as announced on national television by Mr. Tsipras and confirmed by Minister Varoufakis, a victory for the « Yes » vote would mean the resignation of the current government and the establishment of a transitional government with a view to holding new early elections.

Another scenario could see Mr. Tsipras remain in government and reshape his governing majority in favor of more flexible parties. In both cases (an expanded coalition with or without Syriza), the climate for negotiations should calm down considerably and facilitate an agreement, not only on the €7.2 billion still to be disbursed (in addition to the €10.9 billion owed by the EFSF, which could be reallocated to meet the country’s budgetary needs), but also on a third bailout package (worth €29.7 billion).

However, this new round of austerity measures will have a substantial impact on economic activity, given the increase in taxation (corporate and VAT) and contributions on assets, which will constrain domestic demand. According to S&P, the recessionary effect of these measures could cause GDP to decline by 3% in 2015 (compared with the European Commission’s forecast of +0.5%). This would jeopardize the trajectory of public debt (180% in 2015 according to the Commission and its « optimistic » scenario) and push back the reversal of the debt curve to 2016. According to the European Commission, public debt would amount to 118% of GDP in 2030 (scenario excluding debt restructuring).

4 – …whereas if the « No » vote wins, Greece’s default accompanied by an exit from the Eurozone would be very likely.

a. Worst-case scenario: a « No » vote would mean an exit from the eurozone

A scenario involving the country’s exit from the eurozone would have disastrous consequences for Greece, far more so than for its European partners, which would only be marginally affected

In recent history, the case of Argentina’s default serves as a reference and could shed some light on the impact of currency redenomination on a country’s economy. In three years, Argentina’s GDP fell by 20%. This was because the government defaulted on its entire foreign debt and the banking system was paralyzed and declared bankrupt. Capital controls were introduced following a massive flight of deposits, and the government was forced to redenominate assets and liabilities at different and heavily devalued rates. The restructuring of the banking sector (heavily indebted in dollars) caused debt to skyrocket, rising from 63% of GDP at the end of 2001 to 135% a year later. This sharp devaluation also caused consumption to fall as a result of a decline in household wealth (fall in the value of deposits) and rising inflation on imported goods. Finally, the explosion in poverty rates led to an unprecedented social crisis. While devaluation enabled the country to return to a path of high growth in 2003 (although it took until 2007 to return to pre-2001 wealth levels) through exports, this was mainly due to the heavy weight of the export sector in the economy and the boom in global trade. These are two factors that Greece may find difficult to capitalize on today.

Despite the likelihood of a « Grexit, » the systemic risk seems to have been averted. The situation in early 2015 is significantly different from that of 2012, and this change is due to several factors:

– Greek debt is now held by public creditors (see Appendix 3).

– Greece’s weight in Europe remains very low, as evidenced by its share of Eurozone GDP (i.e., 2%).

– The » firewalls » put in place at the European level have strengthened Europe’s ability to deal with crises, namely: the ECB’s quantitative easing program and the European Court of Justice’s validation of the OMT program.[2], the ring-fencing of banking risk as part of the implementation of the Banking Union (Single Resolution Mechanism and, above all, improvement in the quality of bank balance sheets as part of Single Supervision).

– The economic situation is significantly better than in 2012, due in particular to the robust recovery in Portugal and Spain, in the wake of an improvement in employment and purchasing power, which is boosting domestic demand, while exports will benefit from the rebound in Europe. In fact, although Portugal was in a situation similar to that of Greece in 2012, the substantial improvement in its economy is limiting contagion.

All these factors explain why investors are less alarmed than in 2012, as evidenced by the levels of interest rate spreads and CDSs, which remain much less tense than in 2012. The markets therefore do not believe there is a risk of contagion if Greece leaves the eurozone.

However, without causing a systemic crisis, various transmission channels remain and could impact the markets:

– Tensions could arise on the sovereign rates of countries considered fragile (i.e., Portugal, Italy, Spain). Barclays estimates this at a 200bp increase (compared with an increase of around 400-500bp in 2012). In this regard, it should be noted that the ECB’s QE could be adjusted and increased in order to cope with any significant changes in rates.

– Certain countries would be directly affected given their direct (Greek Loan Facility) and indirect (via the EFSF and the ECB) exposure to Greek sovereign debt. These include Germany (€61 billion, or 2.1% of its GDP), France (€46 billion, or 2.1% of its GDP) and Italy (€40 billion, or 2.5% of its GDP). A study by Natixis estimates that the Greek default will increase European debt by 2.5 percentage points of GDP.

– While banks have significantly reduced their exposure to Greek assets, both sovereign and private, they have « gorged » themselves on domestic sovereign assets in recent years. In Italy, Portugal, and Spain, domestic public debt now accounts for between 6% and 10% of banks’ total assets. However, Greece accounts for only a very small share of banks’ sovereign asset portfolios, and in most cases none at all. In fact, Greece’s bankruptcy would have a very marginal direct impact on the quality of banks’ assets. On the other hand, contagion to the spreads of other eurozone countries could put further pressure on the financial sector.

– There is a real political risk in the eurozone linked to the timing of upcoming legislative elections in Europe (Spain and Portugal). Tensions between Europe and Greece could play into the hands of « anti-European » and « anti-austerity » parties. In this regard, Podemos’ victory in the May municipal elections suggests a victory in the September legislative elections, which could increase the risk of contagion in that country.

– Finally, Axa IM anticipates a decline in the euro and equity markets of around 5% to 10%.

b. « Fluctuat Nec Mergitur »: an agreement in favor of Syriza, although unlikely, could be reached in the event of a « No » vote

Emerging stronger from a « No » victory, Mr. Tsipras will be able to return to the negotiating table with greater political leverage. His main demands focus on three points:

– Reshaping the public debt through longer maturities or a haircut.

– No changes to pension levels (particularly EKAS)

– Reviewing the minimum wage

Greece could therefore attempt to obtain concessions from its creditors on these three points, although Germany, Finland, and the Baltic countries appear to be inflexible in their position. Reaching an agreement in the event of a « No » vote therefore seems unlikely.

Notes:

[1] In order to ensure continuity of funding, since February banks have been turning to the Bank of Greece via the Emergency Liquidity Assistance (ELA) system. However, while the rules on collateral are set by the Central Bank itself (which therefore accepts Greek sovereign bonds), there is a clear difference between the rates offered by the ECB (0.05%) and those offered by the ELA (1.95%). Excluding interbank loans and deposits and Eurosystem financing, the aggregate loan-to-deposit ratio rose significantly from 129% to 155% between December 2014 and April 2015, reflecting growing financing needs.

[2]Outright Monetary Transaction: program for the purchase of eurozone sovereign bonds conditional on the implementation of structural reforms.